June 5, 2024

- BoC expected to cut rates 25 bps today.

- US 10-year Treasury Yield decline weighing on greenback.

- US dollar opens lower compared to Tuesday, but little changed overnight.

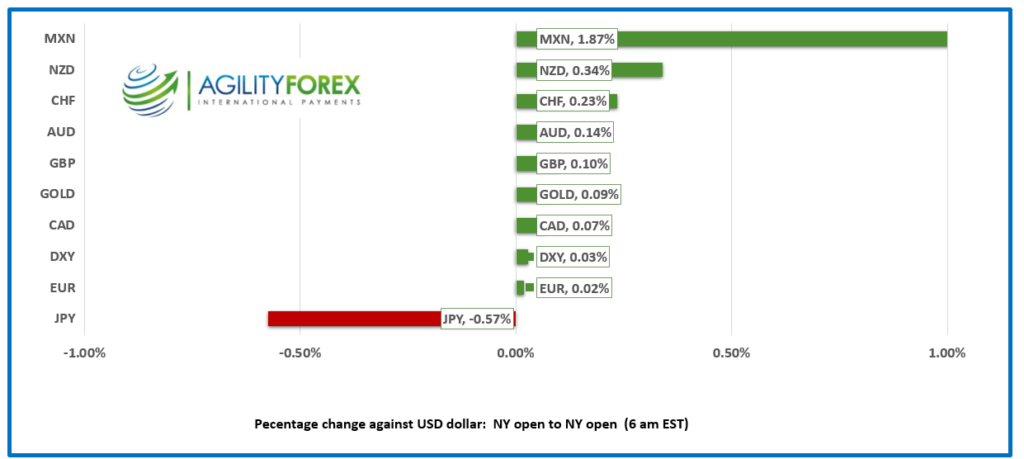

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3685, overnight range 1.3666-1.3691, close 1.3679

USDCAD is bid ahead of todays Bank of Canada interest rate decision. The odds for a rate cut have shifted from about 50/50 in the middle of May to over 80% today due weak economic growth and slowing inflation. The BoC’s preferred inflation measures, CPI-trim and CPI-median are inside the mandated 1-3% inflation band at 2.9% and 2.6%, respectively.

More importantly, Governor Tiff Macklem strongly hinted that a June rate card was in the cards, and he needs to follow through on the prediction or take another hit to is already wonky credibility. The only reason to wait until July is because that is when the quarterly Monetary Policy Report and updated forecasts are available.

The risk to USDCAD will be the tone of the statement and Mr Macklem’s comments in his press conference. If traders think his comments are dovish , USDCAD will rally to the 1.3850 area. However, balanced remarks will leave USDCAD in its 1.3500-1.3800 range.

Soft oil prices are providing a bit of support for USDCAD. WTI traded in a 72.82-73.53 range overnight due to oversupply concerns. The weekly API data showed at 4.05 M b/d increase in US crude inventories which is occurring against a backdrop of global growth concerns due to the Fed staying on hold for longer than expected.

USDCAD Technicals

The intraday technicals are bullish above 1.3650, looking for a break above 1.3710 to extend gains to 1.3750. A move below 1.3650 targets 1.3610 then 1.3550.

The daily chart uptrend line is at 1.3600 with a decisive move above 1.3720 targeting the 1.3775-85 area. A topside break will extend gains to 1.3875.

For today, USDCAD support is in the 1.3650 and 1.3610. Resistance is at 1.3720 and 1.3760. Today’s range is 1.3660-1.3760

Chart: USDCAD daily

Source: DailyFX

Tepid Optimism

Global markets are treading warily ahead of Thursday’s ECB monetary policy meeting and Friday’s US employment report. Soft Australian data, a better than expected Chinese Service PMI report, and mixed Euro area PMI results were merely distractions ahead of the main events. Today’s, US ADP Employment change data came in at 152,000 well below the 173,000 predicted and 36,000 less than April’s downwardly revised 188,000 result. Still it was enough to knock the US 10-year Treasury yield down to 4.328% from 4.345% at the NY open. The ISM Services PMI index is expected to be unchanged at 54.8.

Equities Rising

Equity traders are feeling rather frisky. The recent drop in the US 10-year Treasury yield to 4.328%, post-ADP has encouraged investors in Europe. The German DAX has risen 1.10%, trailed by the 1.04% gain in the French CAC 40 index. S&P 500 futures are up 0.25% and gold (XAUUSD) has risen to 2335.81

EURUSD

EURUSD is steady in a 1.0865-1.0886 range with traders biding their time until Thursday’s ECB decision. Traders did not show any interest in slightly better than expected German Services PMI (actual 54.2 vs forecast 53.9) or modestly weaker than expected Eurozone Services PMI (actual 53.2 vs forecast 53.3). Eurozone PPI did not raise any eyebrows despite falling 1% in April (forecast -0.5%). EURUSD remains underpinned by softer US interest rates.

GBPUSD

GBPUSD traded narrowly in a 1.2764-1.2790 range, but prices were supported by May Services PMI data which ticked up to 53 from 52.8 in April. The PMI statement said that May showed another reasonable rate of expansion in the UK service sector. Taken in tandem with the earlier-released manufacturing survey, the PMIs imply GDP growth of around 0.3% so far in the second quarter. GBPUSD is also bid on the US interest rate outlook.

USDJPY

USDJPY caught a bid yesterday afternoon and rallied from 154.55 to 156.31 overnight. Some analysts suggest that the rally is due to carry trades being unwound after sentiment for earlier than expected Fed rate cut bets improved. Still, gains are limited due to the risk of further BoJ FX intervention, and the prospect of another BoJ rate hike. Service PMI rose to 53.8 from 53.6.

AUDUSD and NZDUSD

AUDUSD traded defensively after soft GDP data falling from 0.6665 to 0.6639. Q1 GDP rose just 0.1% q/q dragging the annual rate down to 1.1% from 1.5%. The AUDUSD downside was limited due to improved China Services data and by comments from RBA Governor Michele Bullock. She warned that rates would rise if there inflation starts rising. NZDUSD traded uneventfully in a 0.6168-0.6199 range

USDMXN

USDMXN dropped from 18.0268 yesterday to 17.0624 in NY today, after the knee-jerk reaction to the Mexican election results faded. Nevertheless, USDMXN downside moves on a lower US rate outlook will be hampered by investor concerns over the socialist government’s agenda.

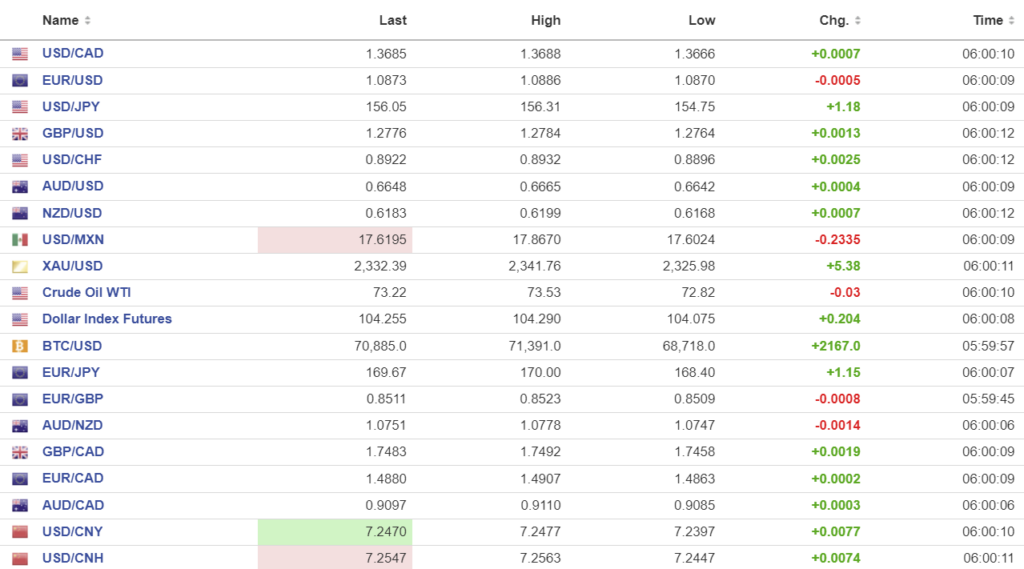

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1097 vs exp. 7.2418 (prev. 7.1083).

Shanghai Shenzhen CSI 300 fell 0.58% to 3594.79

Chinese Caixin Services May PMI 54.0 (Prev. 52.5). The data suggests that China’s economy is on the road to recovery.

China sent 26 fighter planes into and around Taiwan airspace in the past 24 hours.

Chart: USDCNY and USDCNH

Source: Investing.com