Image by DALL-E

December 7, 2023

- BoJ Governor’s comments roil markets.

- BoC rate issues ambiguous guidance.

- US dollar gains except against JPY

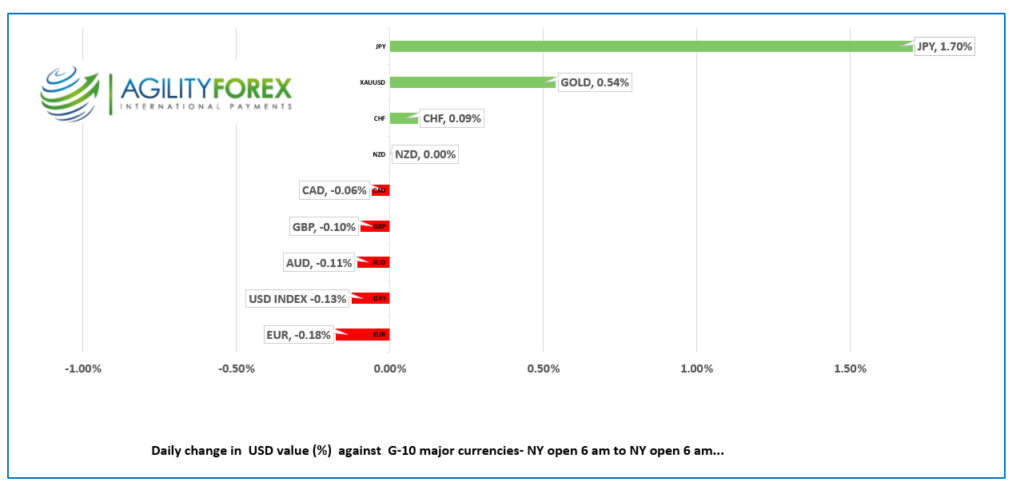

FX at a glance

Source: IFXA/RP

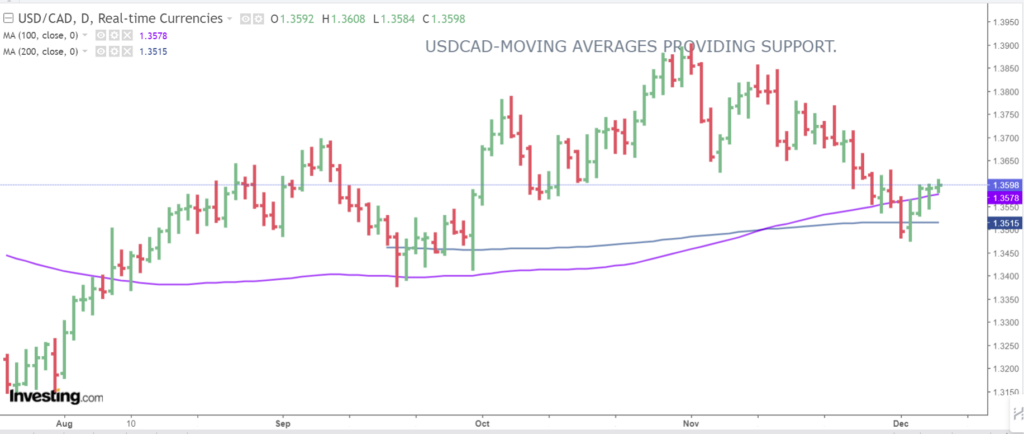

USDCAD Snapshot: open 1.3586-90, overnight range 1.3584-1.3613, close 1.3593

USDCAD traded erratically but in a narrow range following the Bank of Canada’s monetary policy decision and close yesterday, exactly where it closed the day before. Boring!

The BoC statement was ambiguous, but many bank economists claim it was hawkish due to warnings that inflation remains elevated, and wages are still increasing. Deputy Governor Toni Granville will expand on the decision with a speech in Windsor, Ontario, at 12:50 ET.

WTI oil prices are not helping the Canadian dollar at all. Rising U.S. production and a weak Chinese economy more than offset OPEC’s attempt to boost prices. WTI traded in a $69.28-$70.41 range, and prices are down nearly 12% since OPEC announced increased production cuts on November 30.

Canada’s building permits data is on tap.

USDCAD Technicals:

The intraday USDCAD technicals are bullish while trading above 1.3550 and looking for a break above 1.3620 to extend gains to 1.3660. However, unless 1.3660 is broken decisively, the rally is merely a correction.

Longer term, the USDCAD uptrend from August is intact while prices are above 1.3510 and its is guarded by the 100 day moving average in the 1.3570 area with the 200 day moving average sitting at 1.3510.

For today, USDCAD support at 1.3570 and 1.3530. Resistance is at 1.3620 and 1.3660. Today’s range 1.3570-1.3650

Chart: USDCAD daily

Source: Investing.com

G-10 FX recap

“Life is full of coincidences, though some are more deliberate than others.”

How else can you explain the timing of comments by the Bank of Japan Governor that caught markets off guard, exactly eighty-two years to the day after the Empire of Japan launched a sneak attack on the US Naval base at Pearl Harbor? If not for that raid, the movie ‘Oppenheimer’ would never have been made.

BoJ Governor Ueda told the Japanese parliament that the central bank will face an “even more challenging” situation heading into year-end and the beginning of 2024. He also reportedly discussed various options available to the BoJ to end its nearly seven-year negative interest rate policy. Earlier, Deputy Governor Ryozo Himino spoke about the possible impact that ending negative rates would have on the economy.

Traders put two and two together and boosted the odds that the BoJ scraps its negative rate policy on December 19, from 3.5% on December 5 to 45% today. Five and ten-year Japanese government bond (JGB) yields jumped 10.5 bps, and USD/JPY tanked.

China’s trade data did not inspire confidence that the economy was recovering, and those results weighed on risk sentiment in Asia.

The BoJ story, the Chinese trade data, and Wall Street’s negative close set the tone for Asian equity indexes. Japan’s Nikkei 225 index lost 1.70%, while Australia’s ASX ticked down 0.7%. European bourses opened in the red and remain in negative territory, albeit modestly. The German DAX index is down 0.20%. S&P 500 futures are flat.

US 10-year Treasury yields tumbled from 4.205% to 4.106% yesterday in the wake of the weaker-than-expected JOLTs job openings survey. The news raised the odds for a Fed rate cut on March 20 to nearly 60%. Today’s US data will not have the same impact. That suggests markets will consolidate recent moves ahead of Friday’s US nonfarm payroll data.

Challenger Job cuts rose 24% in November compared to October which they said means “The job market is loosening, and employers are not as quick to hire. Weekly jobless claims were close enough to forecasts not to matter.

EUR/USD consolidated yesterday’s losses in a narrow 1.0755-1.0785 range. Traders mostly ignored the BoJ story as they are more concerned about the ECB’s interest rate intentions. The market has priced in 125 bps of cuts for 2024. However, ECB President Christine Lagarde is likely to suggest the expected cuts are too aggressive in her post-ECB meeting press conference on December 14. Eurozone Q3 employment rose 0.2% q/q (forecast 0.3%), while Q3 GDP was 0, compared to the forecast of 0.1% y/y.

GBP/USD was uninspired in a 1.2544-1.2593 range, with price action mirroring that of EUR/USD. GBP/USD is seeing a little support because the BoE is not expected to cut rates as aggressively as the ECB.

USD/JPY plummeted to 144.55 from 147.32 on hopes that the seven-year-old negative interest rate policy ends on December 19. Those hopes, combined with the drop in US Treasury yields, fueled the losses.

AUD/USD traded in a 0.6525-0.6573 range. Disappointing Chinese data weighed on prices in Asia, but that disappointment faded in Europe, and the currency inched higher. Australia’s trade surplus widened but was not a factor for traders.

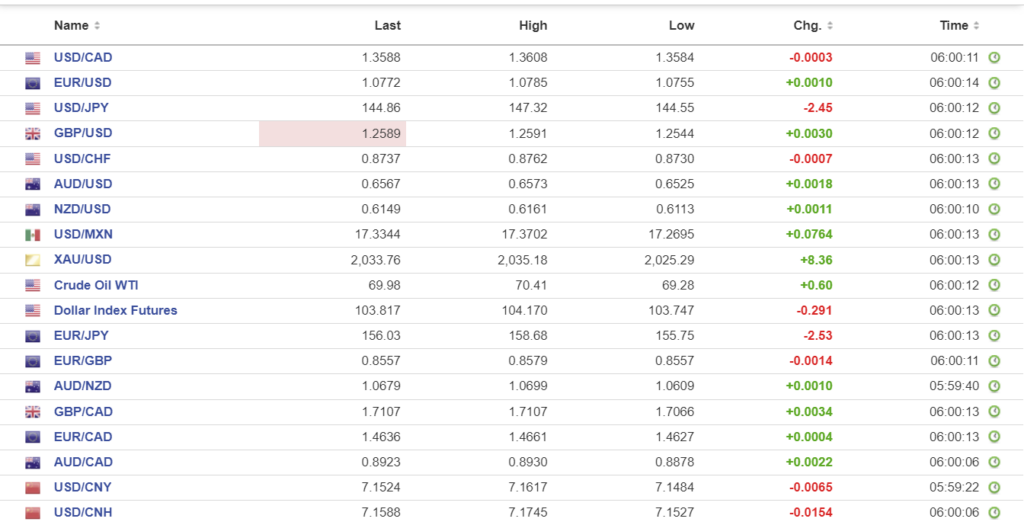

FX high, low, open (as of 6:28 am ET)

Source: Investing.com

China Snapshot

PBoC fix: today 7.1176, expected 7.1623, previous 7.1140.

Shanghai Shenzhen CSI 300 fell 0.24 % to 3391.28.

China’s Trade surplus widened to $68.39 b in November (Oct. $56.53). Imports fell 0.6% m/m while Exports rose 0.5% m/m. The results were welcome news in Beijing as exports grew for the first time in 6 months.

China/Russia trade was $218.2 billion between January and November, which occurred a year ahead of schedule.

Xi Jinping met EU officials at a summit meeting in Beijing. Mr Jinping warned them not to view each others as rivals and avoiding claiming historical rights to the Mediterranean Sea based on the Silk Road trade route.

Chart: USDCNY and USDCNH

Source: Investing.com