Photo:Bing Image Creator

August 15, 2023

- Canada CPI accelerates but BoC core measures ease.

- US data mixed, muddying rate hike waters.

- USD dollar firms on renewed risk aversion.

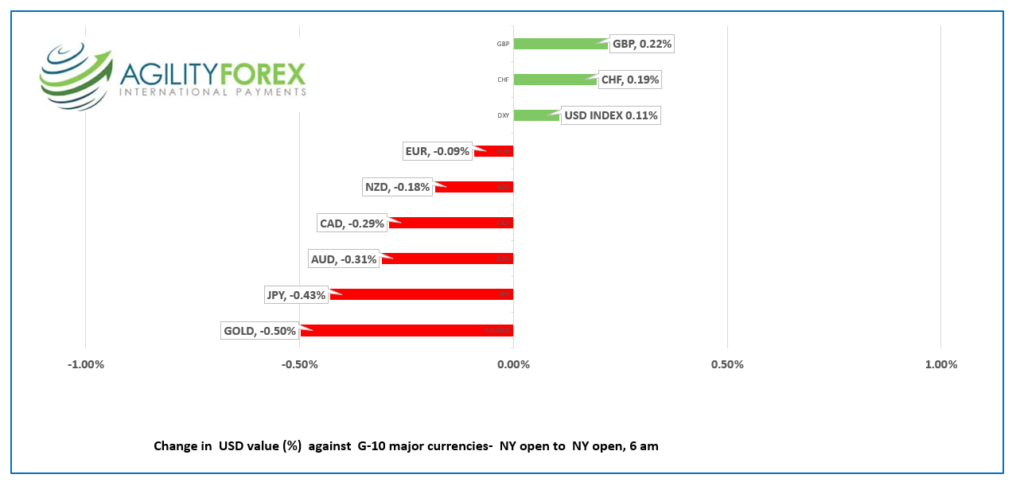

FX at a Glance

Source: IFXA/R

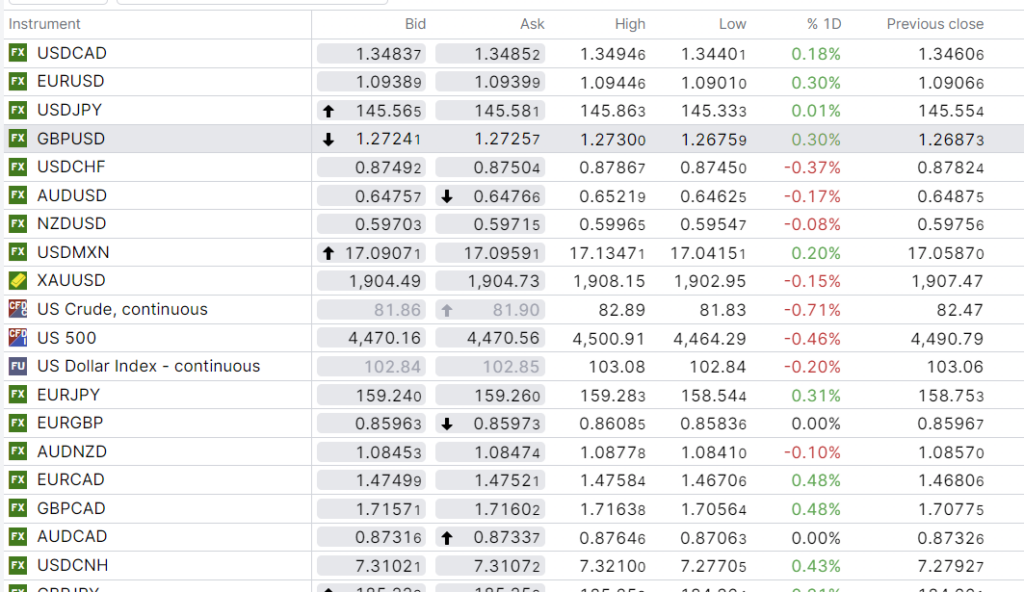

USDCAD Snapshot: open: 1.3484-88, overnight range: 1.3440-1.3500, close 1.3460

USDCAD rallied on the back of negative risk sentiment fueled by fears of a global economic slowdown and rising US Treasury yields which sparked broad based US dollar demand.

The rally stalled in the wake of domestic inflation and US retail sales and NY Empire State Manufacturing data.

Headline CPI rose 3.3% y/y in July well above the 2.8% increase in June, but the gain was dismissed due to base-year effects from gasoline prices. However, the BoC prefers their own inflation measures, CPI-Trim and CPI-Median. The average of those two dipped to 3.65%.

The results offered no clarity regarding the trajectory of future BoC rate hikes.

Oil prices traded defensively on fears of an economic slowdown in China, but the losses were slowed by the recent Opec production cuts. WTI is trading just above the bottom of its overnight $81.13/b-$82.89 range.

USDCAD Technicals

The USDCAD technicals are bullish above 1.3420, looking for a break above 1.3500 to target 1.3580. Prolonged price action above 1.3500 risks a new 1.3500-1.3670 range while a break below 1.3420 negates the upside pressure and argues for more 1.3260-1.3500 consolidation.

For today, USDCAD support is at 1.3420 and 1.3380. Resistance is at 1.3500 and 1.3560. Today’s range 1.3420-1.3510

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap

Emperor and Tsar-wannabes are learning the hard way that they are not bigger than the financial markets. China’s Xi Jinping’s bungled pandemic response and his misguided micromanagement of the economy have scared away foreign investors, sunk the yuan, and exacerbated an economic slow-down.

His newest “bestie” Vlad Putin is presiding over the worst-performing currency in 2023 as the rouble has lost over 26%, and sanctions have crushed exports. In response the Russian central Bank boosted its benchmark interest rate to 12.0% from 8.5%.

Risk sentiment is also negative due to soaring US treasury yields. The 10-year yield is 4.235% compared to 3.97% a week ago. Traders are also concerned that US interest rates could rise further. The Fed claims it is “data dependent” suggesting a stronger than expected retail sales print today, may provide the incentive for another rate hike.

This mornings US data was inconclusive. American consumers are still spending despite 550 bps of rate hikes since March 2022, and that news does not give the Fed any incentive to not raise rates higher. However, the NY Empire Manufacturing Survey offsets the retail sales data to a degree. It fell -19 reflects a significant fall in new orders and shipments.

Asian equity indexes closed in positive territory, except for those in China while European bourses gave up opening gains and are trading with steep losses across the board. The UK FTSE 100 leads the pack with a loss of 1.32%. S&P 500 futures are down 0.59% while gold prices are hovering around $1903.00.

EURUSD eked out a small gain overnight, rising from 1.0898 to 1.0944 despite market angst over China’s weakening economy. The German and Eurozone ZEW economic sentiment survey recorded a slight improvement compared to the previous month. The survey noted that “respondents, by and large, do not anticipate further interest rate hikes in the Eurozone or US.”

GBPUSD rallied from 1.2676 to 1.2730 after the employment report showed a surge in average hourly earnings, excluding bonuses (actual 7.8% from 7.5% previously). The results increase the odds for another BoE rate hike in September, which is underpinning GBPUSD.

USDJPY jumped to 145.86 from 145.33 despite better-than-expected Japanese Q2 GDP, which showed the economy grew 6.0% compared to 3.7%, thanks to sharply higher exports. The news was offset by weakening domestic consumption and the unemployment rate rising to 5.3%. Japanese authorities claimed they would take “steps against excessive currency moves.”

AUDUSD churned in a range of 0.6463-0.6522, peaking after the Chinese rate cut news and then falling as traders feared slowing global growth and higher US interest rates.

NZDUSD traded in a range of 0.5955-0.5997, tracking AUDUSD moves but more restrained ahead of the RBNZ meeting tomorrow.

FX high, low, close

Source: Saxo Bank

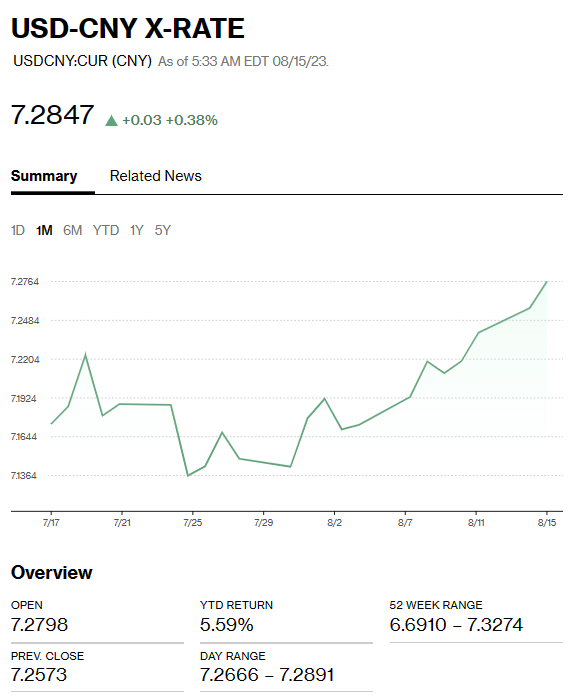

China Snapshot

Bank of China Fix: Today 7.1768 , expected 7.2648, previous 7.1686.

Shanghai Shenzhen CSI 300 fell 0.24% to 3846.54.

PboC surprises market with 15 bp cut to 1-year Medium Term Loan Facility (MLF) to 2.50% from 2.65%.

Authorities announced the government will no longer report youth unemployment (June 23%) . A spokesman from the Statistics Bureau said it was necessary because “statistical work needs continuous improvement.” Sceptics suggest the move is designed to mask the government’s failed economic growth strategy.

Barclay’s Bank cut its China GDP forecast to 4.5% from 5.3%.

Chinese State Banks intervened and sold USDCNY in the 7.2800 area.

Chart: USDCNY 1 month

Source: Bloomberg