Photo: PXfuel

December 1, 2020

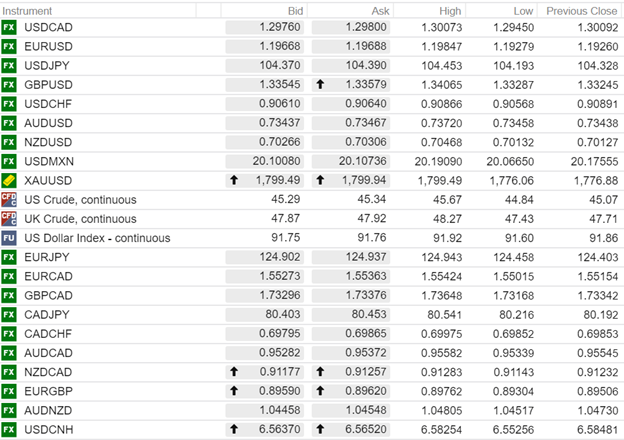

USDCAD open (6:00 am ET) 1.2976-80, Overnight Range 1.2945-1.3007

- Canada GDP in October rises 0.8% m/m (forecast 0.9%)

- Positive COVID-19 vaccine news boosts risk sentiment.

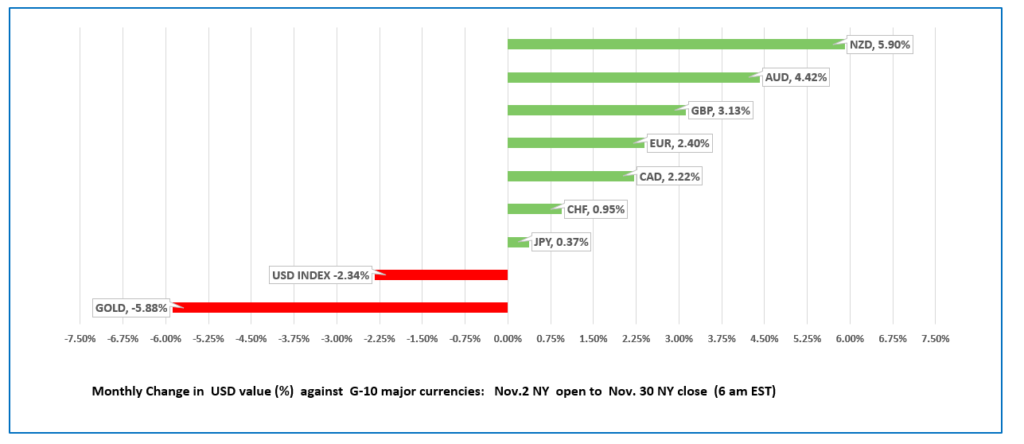

- US dollar finished November with losses across the board

FX Ranges at a Glance for November

Source: IFXA Ltd/RP

FX Recap and Outlook: Forecasters were swinging for the fences with their estimates for Canadian growth- They missed. Canada October GDP failed to live up to expectations, rising 0.8% m/m compared to the downward revised 0.9% in September. GDP rose 40.5% in Q3, q/q. (forecast 47.6). The data and the reasons for the results are stale.

The US dollar started December in retreat, giving back yesterday afternoon’s gains. Better than expected China Caixin Manufacturing PMI in November (actual 54.9 vs 53.6 in Oct.) underpinned risk sentiment in Asia. Global equity indexes rose, as did oil and gold prices. US equity futures are poised for a strong open.

Pfizer added Europe to the list of regions where it sought approval for its vaccine, which added to the positive risk sentiment.

Fed Chair Jerome Powell and Treasury Secretary Steven Mnuchin testify before Congress today. Powell’s remarks have been released. He is still concerned about uncertainty. He said “Recent news on the vaccine front is very positive for the medium term. For now, significant challenges and uncertainties remain, including timing, production and distribution, and efficacy across different groups. It remains difficult to assess the timing and scope of the economic implications of these developments with any degree of confidence.”

EURUSD rallied to 1.1985 from 1.1927, underpinned by vaccine news but hampered by the lack of progress on Brexit, and weak inflation readings. Eurozone November CPI declined 0.3% y/y, as expected.

Euro area Manufacturing PMI was a tick better than forecast but it was offset by weaker than expected German Manufacturing PMI data. EURUSD short term technicals are bullish above 1.1900.

GBPUSD rallied to 1.3409 from 1.3307, then retraced the move, dropping to 1.3318 in NY. UK Housing Price and Manufacturing PMI reports were better than expected, but FX traders didn’t care. Their focus is Brexit, and a lack of progress with a deal.

USDJPY traded sideways in a narrow 104.19-104.45 range. Prices are supported by broad US dollar weakness and the unwinding of safe-haven trades, but longer-term technicals are bearish below 105.20

AUDUSD rallied in Asia, following a benign RBA monetary policy meeting and statement., underpinned by robust China data, and upbeat risk sentiment. The move was reversed in Europe, and AUDUSD opened nearly unchanged in NY. NZDUSD traded similarly but opened with small gains in NY.

Oil prices are modestly higher, underpinned by Opec’s decision to schedule further discussions on production cuts to December 3.

USDCAD mirrored antipodean currency moves. Yesterday’s Federal fiscal update is a 237-page fantasy novel, projecting a $381.6 billion deficit in this year. Traders didn’t care. USDCAD drifted lower in Europe and extended its losses in NY trading.

US ISM PMI and Construction Spending are due.

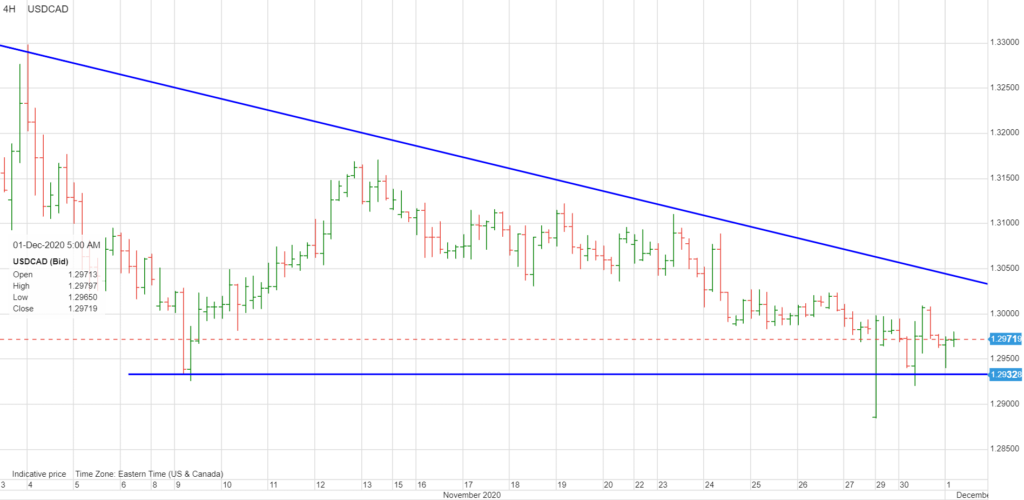

USDCAD Technicals: The technical picture is unchanged from yesterday. They are bearish below 1.3040, looking for a decisive break below the 1.2930-1.2950 support zone to extend losses to 1.2850. For today, USDCAD support is at 1.2980 and 1.2930. Resistance is at 1.3020 and 1.3040 . Today’s Range 1.2940-1.3020

Chart: USDCAD 4 hour

Source: Saxo Bank

FX open (6:00 am EDT) High, Low, and previous close

Source: Saxo Bank