Photo: publicdomainvectors.org

- Canada Headline CPI 7.6% y/y as expected

- German ZEW Index falls again-near all time low

- US dollar adds to gains, CAD outperforms

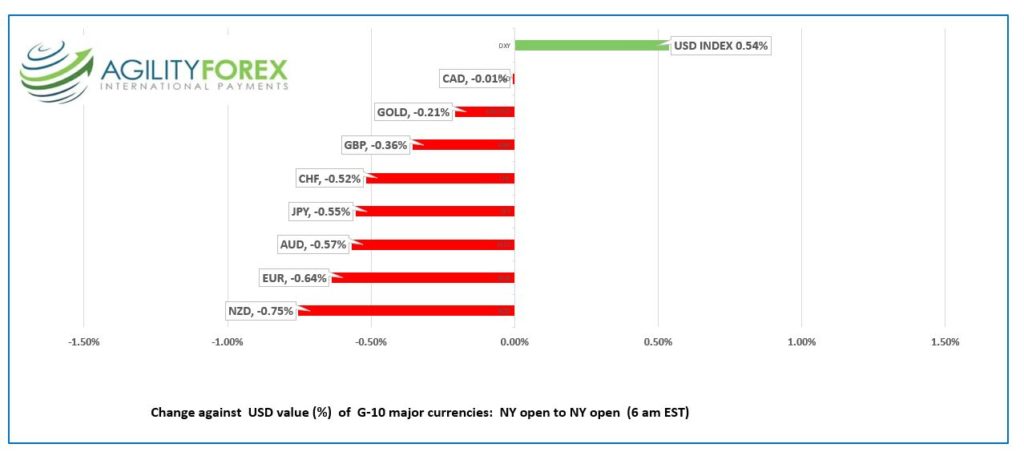

FX at a glance:

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.2904-08, overnight range 1.2883-1.2927, close 1.2902

Canada’s headline CPI rose 7.6% y/y in July, as expected and down from the 8.1% y/y increase in June Core inflation rose 6.1% y/y ,a tad below the 6.2% increase in July. The drop was all due to lower gasoline prices. Prices for natural gas, and groceries rose.

Monthly Core-CPI rose 0.5% m/m (forecast 0.6, June 0.3% m/m).

More importantly, the BoC inflation metrics worsened.

CPI Trim 5.4% in July (5.5% in June), CPI-median 5.0% in July (4.9% in June) and the BoC’s favorite measure, CPI-common 5.5% in July vs 4.6% in June.

The CPI common result will ensure the Bank of Canada hikes rate by 75 bps in September, which helps explain the USDCAD dip to 1.2883 from 1.2902, following the data.

Overnight, USDCAD consolidated yesterday’s gains and opened unchanged compared to Monday. The USDCAD gains are due to external factors and exacerbated by summer-holiday thinned markets.

The Canadian dollar is the best-performing major G-10 currency year-to-date, losing just 1.42% against the US dollar. The other commodity currencies suffered more. The Australian dollar dropped 3.69% while the New Zealand dollar lost 7.55%. Those losses pale in the face of the 16.54% drop in the Japanese yen.

The surge in commodity prices, particularly oil, and the “born-again” inflation fighting Bank of Canada combined to temper USDCAD gains.

USDCAD direction remains at the whim of the US Fed and its outlook for inflation and interest rates. Currently financial markets have decided that the Fed slow the pace of rate hikes for the rest of the year, then cut them as early as January 2023. Fed policymakers have said no such thing, so someone is going to be disappointed.

Russia, China, Iran, and to a lesser extent, North Korea are wild cards, and their actions could spark another round of safe-haven UIS dollar buying.

USDCAD Technical outlook

The intraday USDCAD technicals are bullish above 1.2880, looking for a break of 1.2940 to extend gains to 1.2980, with a topside break targeting 1.3070. Failure to break above 1.2940 and a drop below 1.2880 suggests a retest of support at 1.2730.

For today, USDCAD support is at 1.2880, and 1.2830. Resistance is at 1.2940 and 1.2980. Today’s range: 1.2860-1.2940

Chart: USDCAD 1 hour

Source: Saxo Bank

G-10 FX recap and outlook

Markets are skittish. Yesterday, a drop in the 10-year Treasury yield to 2.768% gave S&P 500 bulls the green light to buy stocks, and they did. However, their conviction wavered overnight, even as the 10-year Treasury yield stayed in a 2.777%-2.80% range overnight.

Traders are awaiting Wednesday’s US data which includes Retail Sales and the FOMC minutes from July 27, for further direction, although next week’s Jackson Hole Symposium may be more relevant to markets.

EURUSD drifted lower, trading in a 1.0126-1.0169 range, weighed down by a poor German ZEW survey result. The statement noted, “The ZEW Economic Expectations decrease again slightly in August after a sharp drop in the previous month. The financial market experts therefore expect a further decline in the already weak economic growth in Germany. The still high inflation rates and the expected additional costs for heating and energy lead to a decrease in profit expectations for the private consumption sector.” A break below 1.0100 targets parity.

GBPUSD followed EURUSD lower, trading in a 1.2009-1.2059 range. The UK employment data was mixed.

Unemployment remains low, but job vacancies fell. Even worse, Liverpool dockworkers, one of the UK’s largest container ports, voted to strike.

USDJPY rallied from 132.96 to 133.29 due to modestly firmer 10-year Treasury yields and ongoing US dollar demand.

AUDUSD traded in a 0.06997-0.7039 range, weighed down by broad US dollar strength. The RBA minutes from the August 2 meeting did not offer any fresh insight. They suggest further rate hikes are in the cards, put qualify the statement with the usual “we are not on a pre-set path” blather. The minutes note that the RBA expects inflation to peak in 2022 and then fall to the 2-3% range in 2023.

NZUSD eased in a 0.6325-0.6369 with Kiwi traders awaiting the RBNZ monetary policy meeting and a universally expected 0.50% rate hike tomorrow. The currency will see some volatility as updated forecasts are released. The risk is that policymakers hint that rates are soon topping out for this cycle.

Today’s US data includes Building Permits, Capacity Utilization, and Industrial Production.

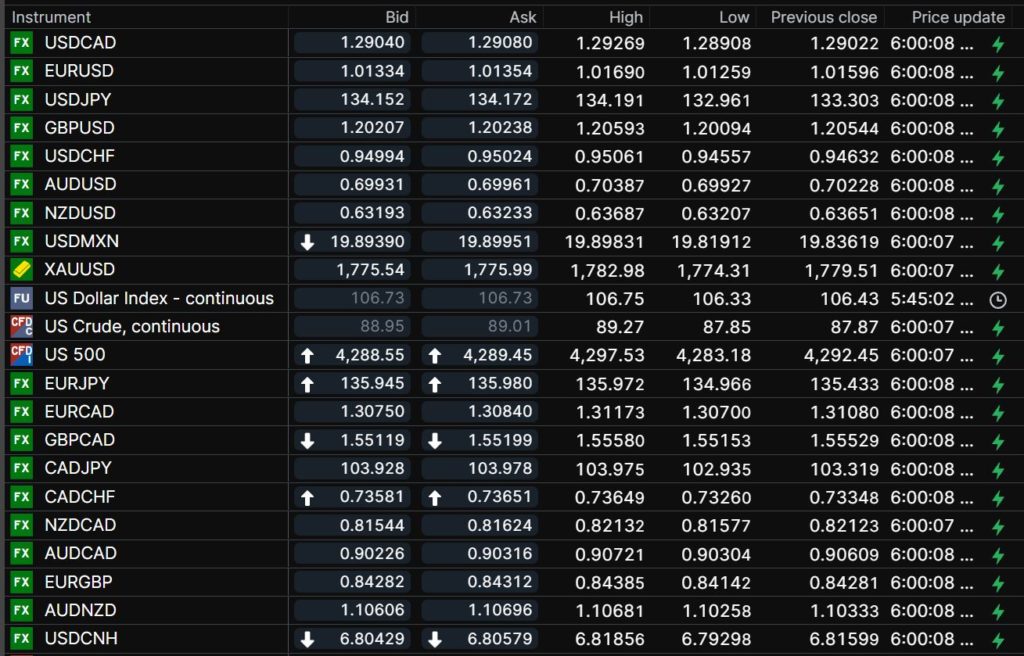

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

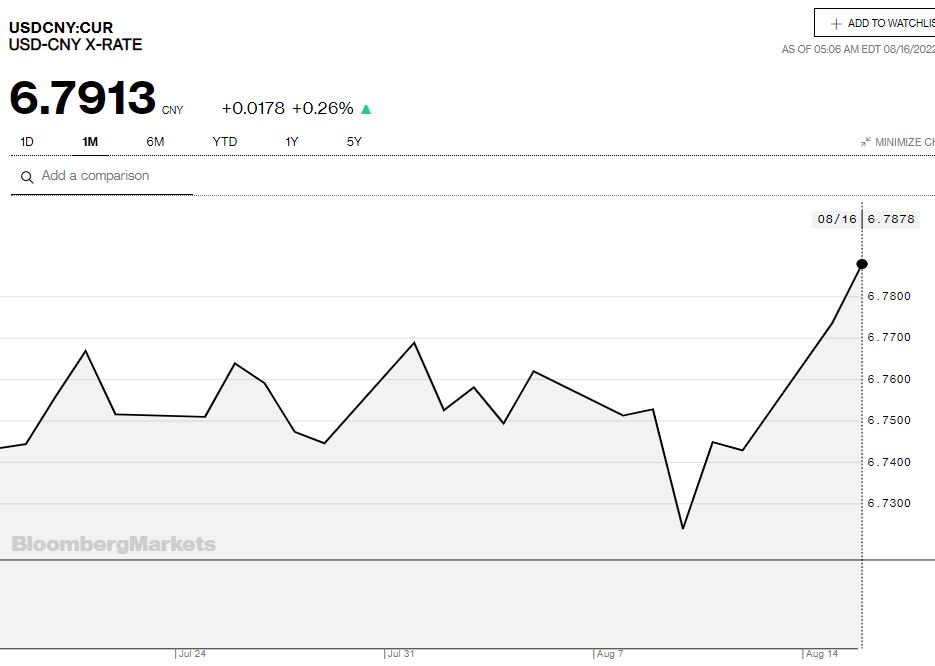

China Snapshot

Today’s Bank of China Fix: 6.7763, previous 6.7410

Shanghai Shenzhen CSI 300 fell 0.19% to 4,177.84

Chinese media suggest China needs more policy stimulus to increase economic growth.

Securities Times suggests the surprise PboC may be the first in a series of measures.

Chart: USDCNY 1 month

Source: Bloomberg