Source: chrome.google.com

- Canada Core inflation hotter than expected -again

- US 10-year Treasury yield comfortable above 4.0%

- US dollar opens soft compared to Tuesday against backdrop of hawkish Fed commentary

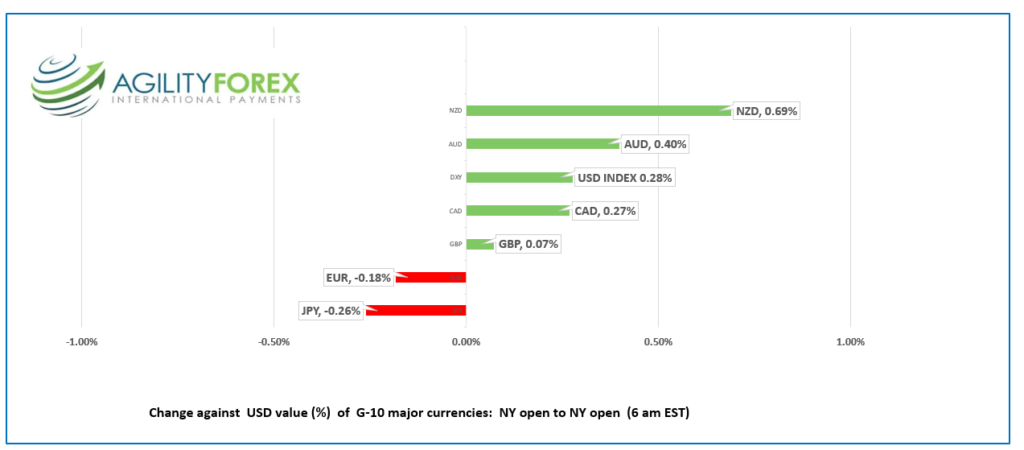

FX at a glance:

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3726-30, overnight range 1.3721-1.3799, close 1.3733

USDCAD traded with a modest bid for most of the overnight session then retreated toward the closing level at the start of NY trading.

USDCAD gains are hampered by expectations that the Bank of Canada will hike rates 75 bps next Wednesday. That view won’t change after today’s September CPI report. The BoC is more concerned about inflation expectations becoming entrenched.

Canada inflation is not moving in the direction the Bank of Canada wants to see. In September headline inflation rose 6.9% which was a tick better than in August, but a tick higher then forecast. The modest dip was mostly due to lower gasoline prices.

Source: Statistics Canada

WTI oil consolidated yesterday’s losses in a $82.63-$84.46/b range overnight. Oil traders seem to believe that slowing growth in China will more than offset the latest Opec production cut that starts November 1. President Biden’s pending announcement about the release of 15 million barrels of crude from the Strategic Petroleum Reserve also weighed prices. WTI didn’t get much support from the API report that crude inventories fell by 1.27 million barrels in the week ending October 14.

USDCAD mostly ignored the inflation data with traders focused on broad US dollar sentiment.

USDCAD Technical outlook

The intraday technicals are bullish inside a minor uptrend channel bound by 1.3670 on the bottom and 1.3950 at the top. Inside that band, USDCAD has a bit of support at 1.3710 with resistance at 1.3780. The long term (weekly) chart shows support at 1.3460.

For today, USDCAD support is at 1.3710 and 1.3670. Resistance is at 1.3780 and 1.3830. Today’s range: 1.3710-1.3810

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

Russian kamikaze drones piloted by Iranians are attacking Ukrainian civilian targets. North Korea is firing artillery to protest South Korea military drills and China is lusting after Taiwan. It’s bad news if you live in or around those regions but for everyone else, its just another day in paradise.

Cleveland Fed President Neal Kashkari said he wasn’t ready to declare a pause in rates hikes, much to the dismay of “Fed-Pivot” disciples. He said he could see US rates getting to the mid-4% area next year. Expect even more hawkish rhetoric from St Louis Fed President James Bullard today.

His comments helped underpin Treasury yields in a 3.998%-4.081% range overnight.

Asian equity indexes posted small gains (except China) with the Australian ASX 200 rising 0.31% and the Nikkei 225 index gaining 0.37%. European bourses followed suit led by a 0.56% gain in the French CAC index. S&P500 futures are down 0.75% while gold lost 1.17%.

US building permits rose 1.4% in September (-8.5% in August) while Housing starts plunged 8.1% compared to 13.7% gain in August. Markets are more concerned about US quarterly earnings reports. Tesla, IBM and P&G report today.

EURUSD traded sideways in Asia then fell from 0.9872 to 0.9761 in early NY. Eurostat reported “The euro area annual inflation rate was 9.9% in September 2022, up from 9.1% in August. European Union annual inflation was 10.9% in September 2022, up from 10.1% in August. The results helped ensure the ECB hikes rates by 75 bps next October 27.

GBPUSD traded negatively in a 1.1237-1.1357 range after the euphoria from the budget U-turn fades. Yesterday’s FT story that the Bank of England would delay the start of its QT program proved false, with the BoE confirming gilt sales start November 1. UK inflation rose 10.1% y/y in September (forecast 10.0%, August 9.9% y/y) with PPI and Retail Price index data also above forecasts.

The Office for National Statistics (ONS) said “After last month’s small fall, headline inflation returned to its high seen earlier in the summer. The rise was driven by further increases across food, which saw its largest annual rise in over 40 years, while hotel prices also increased after falling this time last year.”

USDJPY rose from 149.11 to 149.77 despite warnings from Finance Minister Shunichi Suzuki saying the government would properly respond in the exchange market. BoJ board member Seiji Adachi said it was premature to shift away from the bank’s ultra-easy monetary policy.

AUDUSD and NZDUSD price action tracked broad US dollar moves with both currency pairs trading at overnight session lows in NY.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

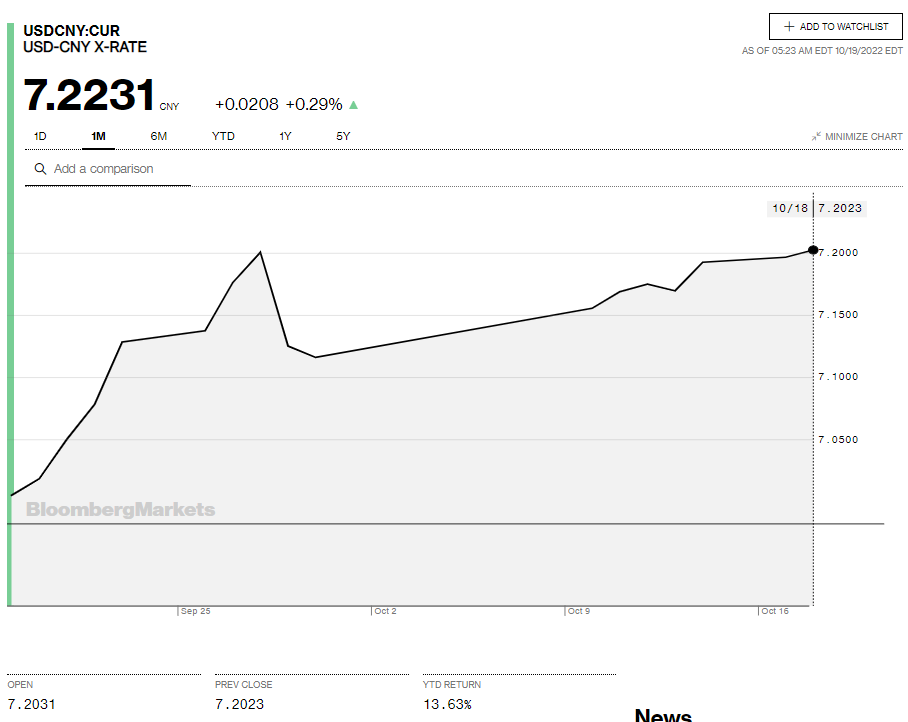

China Snapshot

Today’s Bank of China Fix: 7.1105, previous 7.1086

Shanghai Shenzhen CSI 300 fell 1.61% to 3776.53

Chart: USDCNY 1 month

Source: Saxo Bank