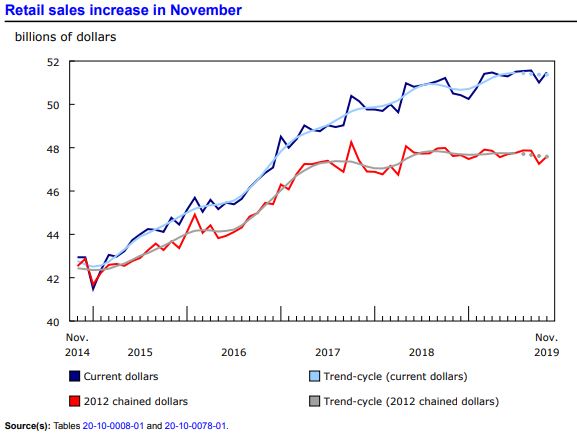

Source: Statistics Canada

January 24, 2020

USDCAD open (6:00 am EST) 1.3138-42 Overnight Range 1.3120-1.3140

Canadian retail sales jumped more than expected in November, rising 0.9% m/m, a vast improvement over Octobers 1.1% decline. Statistics Canada credited the increase to “higher sales at motor vehicle and parts dealers and at food and beverage stores, both of which were down in October.”

The better than expected Canadian data follows on the heels of European and UK Purchasing Managers Index reports, which also surprised to the upside.

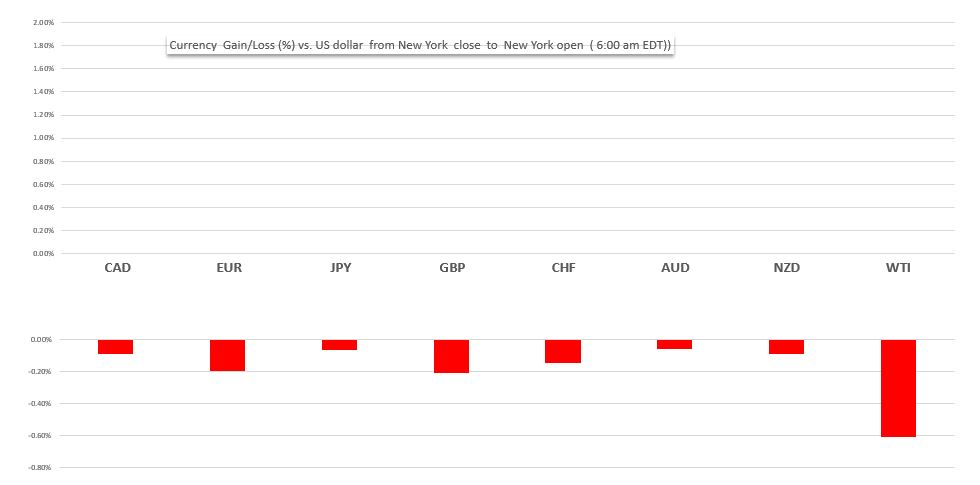

The US dollar is virtually unchanged after opening with small gains against the G-10 major today, and poised to finish the week on a mixed note. Gains against CAD, EUR, CHF, and AUD were offset by losses against GBP, JPY and NZD.

Chart: Currency gain/loss (%) against the US dollar from NY open Jan.20 to NY open Jan 24.

Source: Saxo Bank/ IFXA Ltd

EURUSD traded sideways in Asia but perked up in Europe. Prices jumped to 1.1060 from 1.1042 when German Manufacturing PMI printed 45.2 rather than the 44.5 forecast. The gain suggested that Germany’s economy was picking up, albeit slowly. Eurozone Manufacturing PMI rose 47.8 (forecast 46.8) which supported the rally, but the move was short-lived. Traders quickly sold EURUSD, reverting to yesterday’s post-ECB meeting concerns that the existing easy monetary policy will stay in place for a long time. EURUSD continues to trade with an offered bias in early New York markets.

GBPUSD rallied following its Markit Manufacturing PMI report rising to 47.8 in January compared to the forecast for a 46.8 gain. UK coronavirus fears, the upcoming official Brexit date and bearish technicals weighed on the currency pair. GBPUSD dropped from a post-data peak of 1.3170 to 1.3081 in New York trading.

Asia traders noticed a shortage of liquidity which was due to the start of the Chinese New Years celebrations. USDJPY direction was torn between demand due to broad US dollar strength and selling from risk aversion sentiment, although the sellers had the edge. Price churned between 109.45 and 109.64 undermined by soft US Treasury yields and bearish intraday USDJPY technicals below 109.80.

NZDUSD outperformed AUDUSD and USDCAD. Prices jumped to 0.6627 from yesterday’s low of 0.6580 after New Zealand inflation rose higher than expected Q4 CPI rose 1.9% y/y compared to the forecast of a 1.8% gain. AUDUSD was weighed down by disappointing by modestly weak PMI data.

Oil prices continue to suffer from fears that the Wuhan coronavirus will lower China’s demand for crude and yesterday’s uninspiring EIA Crude stocks report. Traders ignored an article from TASS, suggesting Opec would extend production cuts until the end of 2020. The intraday WTI technicals are bearish below $57.00/barrel, looking for a break of $54.80/b to extend losses to $53.60/b.

USDCAD continued to consolidate its gains following the Bank of Canada’s dovish monetary policy flip-flop on Wednesday. The domestic Retail Sales data has prices poised to test support in the 1.3090-1.3105 area. However further losses may be curtailed due to weak oil prices.

There are not any notable US economic reports, suggesting the greenback could be vulnerable to profit-taking selling into the weekend.

USDCAD Technical Outlook

USDCAD is consolidating gains with a bullish bias. The intraday uptrend is intact above 1.3070 and looking for a break of resistance at 1.3170 to extend gains to 1.3320. A break of minor support at 1.3120 targets 1.3070. For today, USDCAD support is at 1.3105 and 1.3070. Resistance is at 1.3160 and 1.3190. today’s Range 1.3070-1.3140

Chart: USDCAD 30 minute

Source: Saxo Bank