Photo: Bing Image Creator

October 31, 2023

- BoC Governor blames Feds for stubborn inflation.

- Canada GDP flatlines in August

- US dollar opens soft-JPY falls sharply.

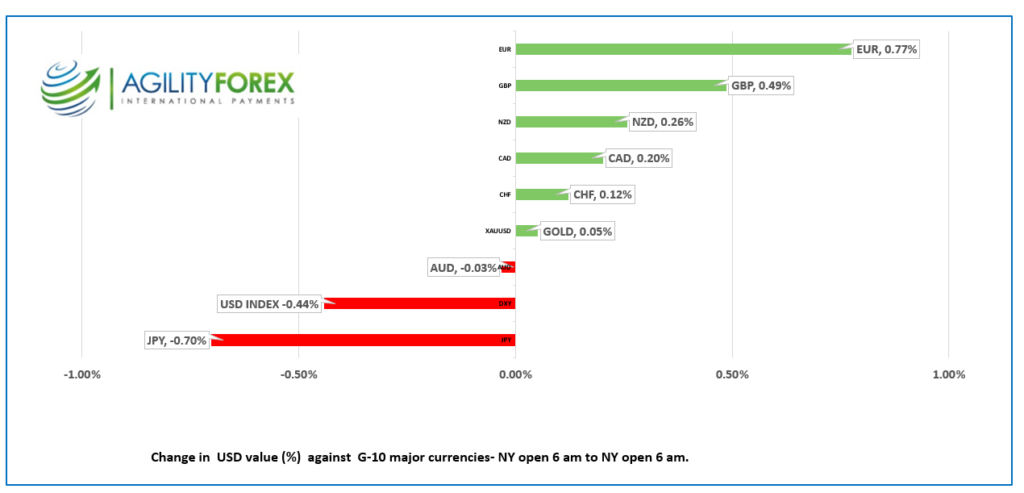

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open: 1.3815-19, overnight range 1.3814-1.3852, close 1.3826

USDCAD dipped modestly overnight due to US dollar selling pressures in Europe following better-than-expected Eurozone inflation data. In addition, month-end rebalancing flows and pre-Fed positioning also played a role.

Bank of Canada Governor blamed the federal and provincial governments’ voracious spending for propping up inflation. CTV News reported that Trudeau’s generous spending and open-door immigration policies have driven up interest rates. Cynics would suggest Macklem should have called out the Fed long before inflation became so problematic.

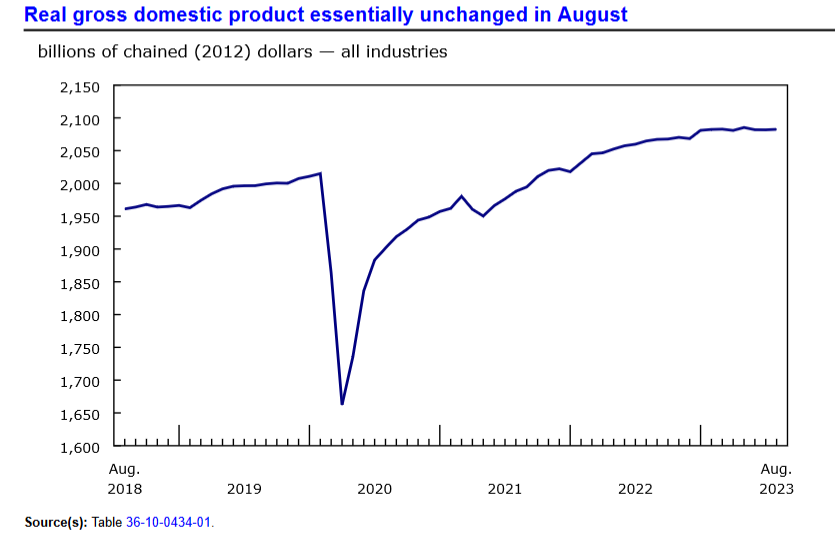

Canada’s economy flat-lined in August (actual GDP 0.0%, forecast 0.1%). Statistics Canada said Real gross domestic product (GDP) was essentially unchanged for a second consecutive month in August as factors such as “higher interest rates, inflation, forest fires and drought conditions continued to weigh on the economy. Services-producing industries edged up 0.1% in the month, while goods-producing industries contracted 0.2%. Overall, 8 of 20 industrial sectors increased.

Source: Statistics Canada

World Bank economists offered up a scary Halloween forecast, warning oil prices could soar to $140.00-$150.00/b if Israel’s war against terrorists widens. It is their “worst-case” scenario and is based on the energy disruptions caused by the Russian invasion of Ukraine. Oil traders didn’t seem to care and drove WTI to $82.31/b from $83.25/b overnight.

USDCAD Technicals:

The intraday USDCAD technicals are bullish above 1.3780 which is being guarded by minor support at 1.3810. That level was tested overnight, and it held, leaving prices to bounce in a 1.3810-1.3870 level until after Wednesday’s FOMC meeting. A break below 1.3790 will risks 1.3710 although there is support in the 1.3740 area. A topside break targets 1.4000.

Longer, term, the USDCAD uptrend from July is intact above 1.3590.

For today, USDCAD support at 1.3810 and 1.3780. Resistance at 1.3860 and 1.3890. Today’s expected trading range is 1.3810-1.3890.

Chart: USDCAD 4 hour

Source: Daily FX

G-10 FX recap

October is headed to the graveyard, and not many people are sorry to see it go, particularly equity bulls and US dollar bears. It’s also month-end, which brings the usual market distortions against a backdrop of soft Chinese Manufacturing PMI, a dovish Bank of Japan monetary policy announcement, and the FOMC decision tomorrow.

Asian equity indexes closed slightly higher. Japan’s Nikkei 225 index gained 0.53%, while Australia’s ASX rose 0.11%. European bourses are in positive territory, and S&P 500 futures are up 0.21%. The US 10-year Treasury yield slipped to 4.818% from 4.83%, and gold (XAUUSD) rose 0.15% to 1999.09 as of 7:00 AM ET.

The US Employment Cost Index (ECI) rose 1.0% in Q3, compared to the forecast of 1.0% which served to give the US dollar a bit of a boost.

EURUSD traded higher, rising from 1.0591 to 1.0675, following lower-than-expected inflation data, with added support from EURJPY demand. The Q3 Harmonized Index of Consumer Prices (HICP) rose 2.9% y/y, below the forecast of 3.1% and well below 4.3% in Q2. Eurozone GDP fell by 0.1% in Q3, but the news was largely ignored. Analysts have downgraded their outlook for ECB rates, while the Fed will likely repeat its “higher for longer” mantra tomorrow. That contrast suggests limited EURUSD upside.

GBPUSD is at the top of its 1.2137-1.2200 range, bolstered by GBPJPY demand and broad US dollar demand. The Bank of England meeting is on Thursday.

USDJPY soared from 149.03 to 150.76 after the Bank of Japan disappointed markets. The BoJ had leaked a story suggesting that the YCC would be adjusted to a top of 1.25% from 1.0%. They lied. All they did was change 1.0% from a cap to a reference rate. However, ING analysts argue that the tweak is not minor because the BoJ also said they would be ending the daily bond purchase program, which means that the BoJ will not explicitly fix the rate and let the market decide.

AUDUSD climbed to 0.6377 from 0.6341 due to AUDJPY demand and general US dollar selling.

Today’s US data: Chicago PMI, Consumer Confidence, and Housing Price Index

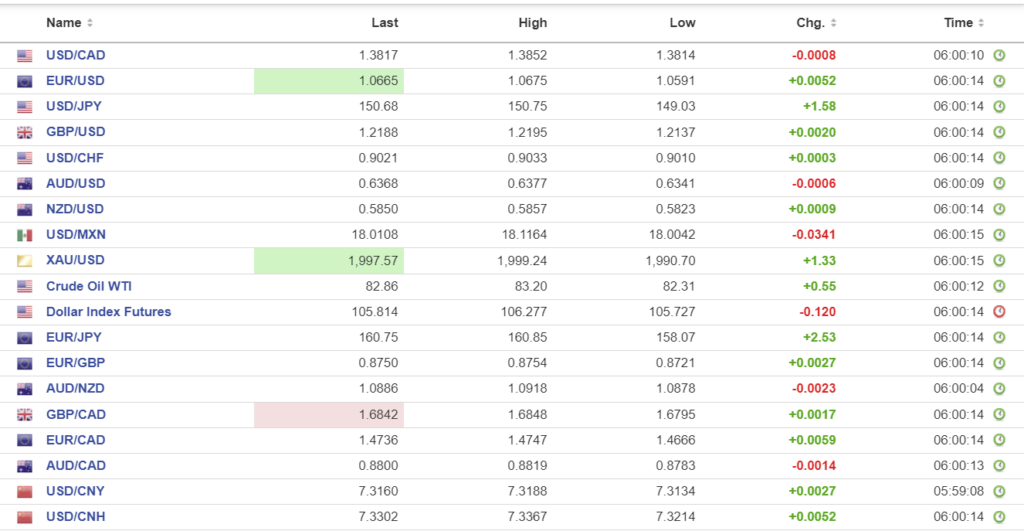

FX high, low, open

Source: Investing.com

China Snapshot

PBoC fix: today 7.1779, expected 7.3024, previous 7.1781.

Shanghai Shenzhen CSI 300 fell 0.31% to 3572.51

October Manufacturing PMI (actual 49.5 (expected 50.2, September 50.2)

Non-Manufacturing PMI (actual 50.6, expected 51.8, September 51.7)

Chart: USDCNY (onshore) vs USDCNH (offshore) hourly

Source: Investing.com