Photo: Bing Image Creator

September 8, 2023

- Canada adds 39,900 jobs, more than expected.

- Canadian dollar shrugs off Governor Macklem speech

- US dollar rally takes a breather and CAD playing catch-up.

FX at a Glance

Source: IFXA/RP

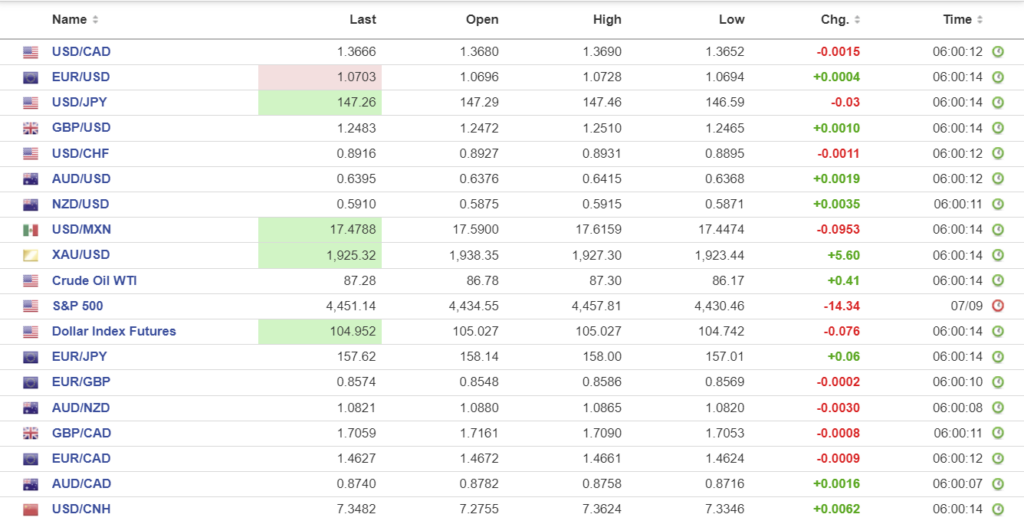

USDCAD Snapshot: open: 1.3664-68, overnight range: 1.3610-1.3690, close 1.3687

Canada added far more jobs in August than what was anticipated. The 39,900 job gains surpassed the consensus estimate for a 15,000 gain and the unemployment rate remained unchanged at 5.5%.

Yesterday, Bank of Canada Governor Tiff Macklem said “With past interest rate increases still working their way through the economy, monetary policy may be sufficiently restrictive to restore price stability.”

Fortunately for him, he presented a detailed argument for why an end to rate hikes won’t happen just yet. He said that the BoC remains “concerned that overall inflationary pressures are persisting, and larger-than-normal price increases remain broad-based across the goods and services Canadians buy regularly.” He also said that there is a risk that monetary policy is not yet restrictive enough.

Today’s employment data suggests he was prudent to highlight the upside risk to interest rates.

However, despite the headline suggesting the economy is booming and churning out new jobs, the details are rather disappointing. The data shows that fewer private sector workers are paying for more public sector employees. Who wouldn’t want a government job with pretty much a life-time guarantee of employment, complete with a gold-plated, inflation indexed pension?

This week’s WTI oil price rally stalled resistance in the $88.00/barrel area as traders juggle concerns about lower supply from Opec production cuts with fears of slowing demand due to China’s economic malaise.

USDCAD dropped to its session low of 1.3610 after the employment report, but it may not have a lot more downside.

USDCAD Technicals

The intraday USDCAD technicals are bullish above 1.3610, looking for a break of resistance in the 1.3680-1.3700 area to extend gains to 1.3750, then 1.4000.

Longer term, the August uptrend line comes into play at 1.3590, with a break above 1.3750 setting up further gains to the 1.4000 area.

For today, USDCAD support is at 1.3610 and 1.3580. Resistance is at 1.3680 and 1.3740. Today’s range 1.3580-1.3670.

Chart: USDCAD 4 hour

Source: Investing.com

G-10 FX recap

The G-20 Summit and photo-op meeting kicks off in New Delhi, India this weekend. The flunkies have been beavering away at crafting a communique which will condemn the Russian invasion of Ukraine, while simultaneously supporting the Chinese and Russian view on the matter. Russia’s Foreign Minister Sergei Lavrov said Moscow will block the final declaration if it does not reflect its stand. That is easily solved. Call it the G-18 and be done with it.

Vladimir Putin is not attending the festivities because the International Criminal court has issued a warrant for his arrest. Xi Jinping may be taking a pass in case rivals use his absence to take control of the country due to his poor leadership.

Fed watchers expecting that the FOMC will leave rates unchanged at the September 20 meeting were a a tad worried after Thursday’s weekly jobless claims data showed the labour market was still on solid ground. Fortunately, a bevy of Fed officials suggested that rates may be left unchanged at the next meeting.

Traders are a tad risk negative and concerned that China’s ban of iPhones for government use, may be expanded to all state-owned firms and escalate the US/China tech war.

Asia equity indexes closed negatively. The Hong Kong Hang Seng index lost 1.34%, Japan’s Nikkei 225 index fell 1.16% and Australia’s ASX 200 dipped 0.20%. The German Dax is down 0.79% leading the other major bourses lower. S&P futures are down 0.20% and the US 10-year Treasury yield is unchanged at 4.246%.

EURUSD rose from 1.0696 to 1.0728 the dropped to 1.0700 in early NY trading. Germany’s inflation rate was 6.1% y/y in August a tick below the 6.2% seen in July. It was expected. Traders are looking ahead to next week’s ECB meeting with policymakers expected to leave rates unchanged.

GBPUSD is trading negatively in a 1.2465-1.2510. Sentiment is bearish due to the recent downgrading of Bank of England rate increases. The expected peak rate has dropped from 6.50% in June to 5.60%, which has curtailed some GBPUSD demand.

USDJPY dipsy-doodled in a 146.246-147.29 band as traders following weaker than expected Q2 GDP (actual 4.8% vs forecast 5.5% and 6.0% in Q1). Traders are also wrestling with BoJ intervention fears and steady to higher US Treasury yields. Intervention threats intensify with USDJPY gains.

AUDUSD traded in a 0.6368-0.6415 band with gains capped by deteriorating risk sentiment around the China/US tech dispute and by broad US dollar demand.

Top of Form

FX high, low, open

Source: Investing.com

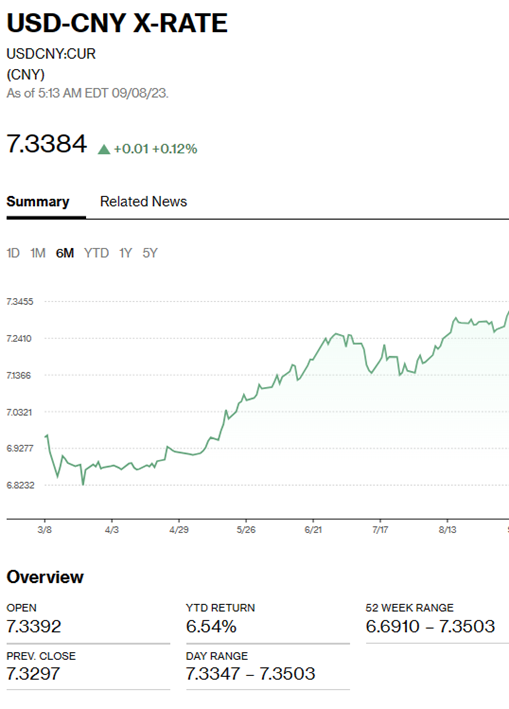

China Snapshot

Bank of China Fix: today 7.2150, expected 7.3284, previous 7.1986.

Shanghai Shenzhen CSI 300 fell 0.49% to 3739.99.

Chart: USDCNY 1 month

Source: Bloomberg