Image by DALL-E

December 19, 2023

- Canada Core-CPI rises more than expected.

- BoJ disappoints and leaves monetary policy unchanged.

- US dollar drifts lower, except against yen.

USDCAD Snapshot: open 1.3385-89, overnight range 1.3336-1.3403, close 1.3400

If Santa Claus made his rounds today, he would have delivered a huge lump of coal to Canadians. Statistics Canada reported that CPI rose 3.1% y/y in November, unchanged from October and disappointing those expecting just a 2.9% increase. Even worse, Core CPI (excludes food and energy) rose 3.5% compared to 3.4% in October.

Once again, the BoC looks confused. The post-BoC monetary policy statement warned that sticky or higher inflations posed upside risks to Canadian rates. Then Friday, Governor Tiff Macklem told Bloomberg that the bank is likely to cut rates some time in 2024. Today’s data suggests rates may go higher.

The BoC is unlikely to raise rates due to the impact on the economy and due to political pressure. In addition, the majority of central banks in developed markets are discussing when rates will be cut and the BoC is no different, despite what Macklem says.

USDCAD slipped on the results but support in the 1.3340-50 area held.

Oil prices are not getting much of a boost from supply disruption risks due to Yemeni Houthis attacking Red Sea shipping. The US created task force to combat the threat is one reason expectations of weak Chinese oil demand is limiting gains.

USDCAD Technicals:

The intraday USDCAD technicals are directionless. USDCAD is trapped in a tight 1.3350-1.3410 range. A move below 1.3350 targets 1.3310 while a break above 1.3410 targets 1.3460.

Longer term, USDCAD the November downtrend line is intact while prices are below 1.3680.

For today, USDCAD support at 1.3340 and 1.3310. Resistance is at 1.3410 and 1.3460. Today’s range 1.3340-1.3420.

Chart: USDCAD 4 hour

Source: Daily FX

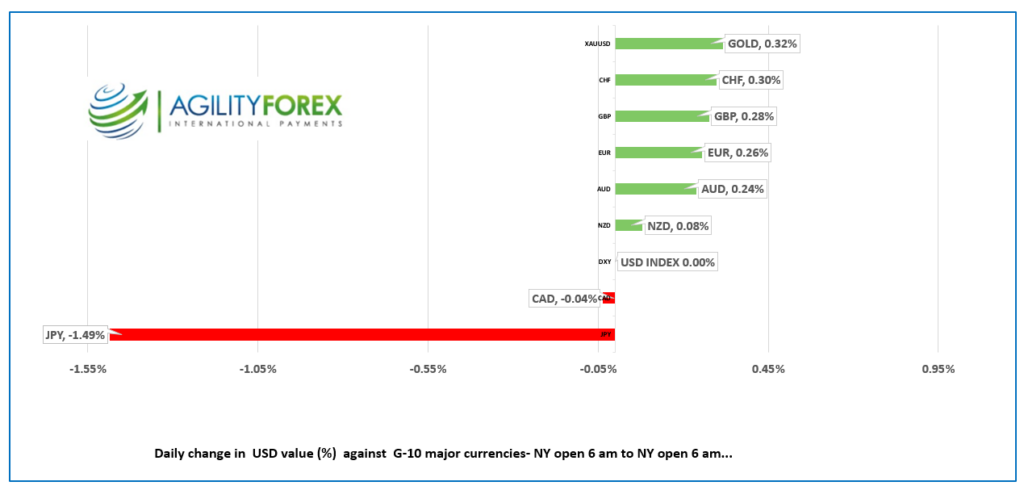

G-10 FX recap

It was another drab FX session overnight, unless you were involved in USDJPY, which managed to rally nearly 1.5% from yesterday’s NY open. Traders have fully embraced the seasonal holidays, and many have closed their books for the year.

It is the time for peace on Earth and goodwill to all men, unless you are an Ayatollah of Iran. They are determined to bring their medieval ideology worldwide, which is one of the reasons the US is leading a Naval task force to protect Red Sea shipping from Iran-proxy Houthi rebels in Yemen. The task force includes the UK, Bahrain, France, Italy, the Netherlands, Norway, the Seychelles, Spain, and Canada. Canada’s contribution will be minimal after the government cut the National Defence budget in the latest Fiscal update.

EURUSD is modestly bid, rising from 1.0915 to 1.0949. Headline Harmonized CPI fell -0.6% in November (forecast -0.5%), but rose 2.4% y/y as expected. The results had little impact on FX markets, as the numbers were in line with the ECB forecast of 2.8% y/y in Q4.

GBPUSD has a minor bid, as prices climbed in a 1.2636-1.2710 range, supported in part by BoE officials suggesting that UK rates will not be cut in 2024. Traders are looking ahead to Wednesday’s UK CPI and PPI data.

USDJPY popped from 142.32 yesterday to 144.93 in NY trading today then retreated. Traders were disappointed with Bank of Japan actions, or rather inaction. After teasing markets with suggestions of monetary policy tweaks since the beginning of November, Governor Ueda and company left its negative overnight rate at -0.1% and left the yield curve control policy unchanged. Some analysts are suggesting that the BoJ is in no hurry to change policy now that the other major central banks are cutting rates.

AUDUSD was rangebound inside a 0.6701-0.6734 range. The RBA minutes from the December 5 meeting reveal a board that is sucking and blowing simultaneously. Australian interest rates could go up if they don’t go down, depending upon inflation. That’s a familiar refrain to USDCAD traders.

NZDUSD traded sideways in a 0.6206-0.6241 range. Kiwi was underpinned after the ANZ Business Confidence survey rose to 33.2 from 30.8 in December. The NZ trade deficit narrowed to $1.234 million from -$1.730 million.

US Housing starts and building permits data are on tap.

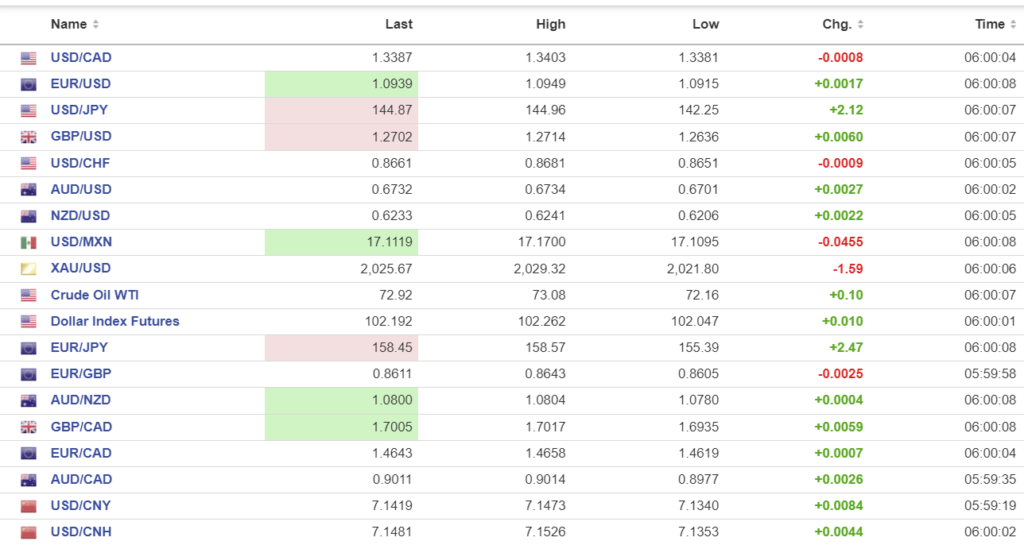

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: today 7.0982, expected 7.1347, previous 7.0933.

Shanghai Shenzhen CSI 300 rose 0.14% to 3334.04.

Chart: USDCNY and USDCNH

Source: Investing.com