August 9, 2024

- Canada lost 2,800 jobs and the unemployment rate was unchanged at 6.4%

- Global equities rally hard, following Wall Street lead.

- US dollar opens defensively but grinding out gains in NY.

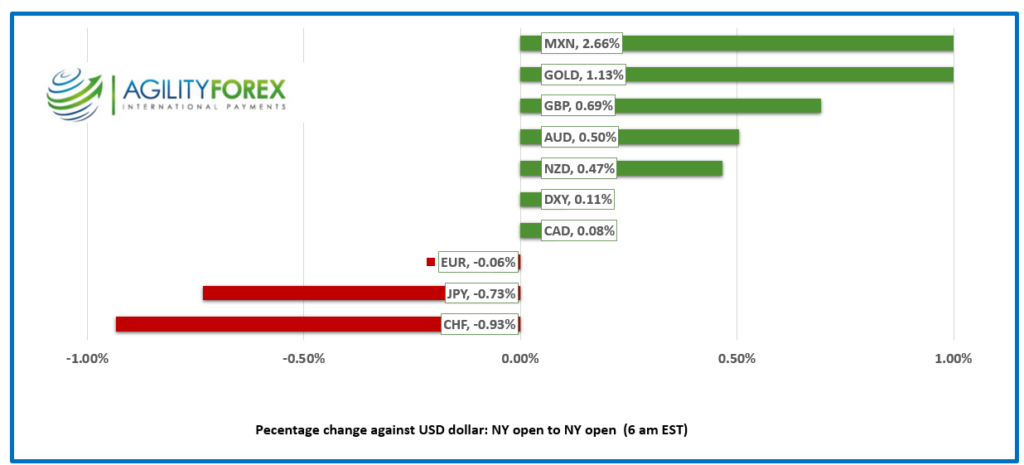

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3733, overnight range 1.3718-1.3755, previous close 1.3735

Equity traders are deep in thought, plucking petals from a daisy, whispering, “The market loves me; the market loves me not.” All week, they’ve oscillated between hope and despair, much like a Simone Biles gold medal floor routine. This equity gymnastics is driving global risk sentiment, with USDCAD hitching a volatile ride.

The Canadian Labour Force Survey (LFS) unveiled a very weak job environment. The only sector creating jobs is the government. Public sector employment rose by 41,000 in July and is up 205,000 year/year. That’s nuts! Rising public sector employment when private sector jobs are decreasing risks the reduced private sector workers facing a higher tax burden to pay for the government workers. Public sector workers do not generate economic value or produce goods and services that fuel market expansion. The July Monetary Policy report warned that a widening output gap would lead to slower growth. Canada’s economic growth does not have much room to slow before it starts contracting.

Comments from Fed policymakers yesterday did not suggest officials were in any hurry to cut rates. Richmond Fed President Thomas Barkin expressed skepticism about labor market weakness, while Kansas City Fed President Jeff Schmid noted that current Fed policy isn’t overly restrictive, with inflation still above the 2.0% target.

Despite this, the CME FedWatch Tool places the odds of a 50 bp rate cut on September 18 at 53%. This expectation has pushed the 10-year CAD/USD interest rate spread lower, putting downward pressure on USDCAD.

USDCAD Technicals

The intraday USDCAD technicals are bearish. Support at 1.3780 has reverted to resistance following Monday’s move lower. USDCASD is in a minor downtrend channel between 1.3695 and 1.3750. A topside break will test resistance, which if broken suggests another rally to 1.3890.

Longer term, USDCAD has been riding a kiddie rollercoaster since snapping a downtrend in the first week of January. A series of higher lows have guided prices toward the 1.4000 area. Only a decisive move below the 1.3590-1.3620 area will negate the upward pressure.

For today, USDCAD support is at 1.3710 and 1.3690. Resistance is at 1.3770 and 1.3810. Today’s Range 1.3710-1.3790

Chart: USDCAD daily

Source: DailyFX

Stopping to Smell the Roses

With no actionable data points on the US economic calendar today and after the significant equity market swings this week, traders are taking a breather and metaphorically have their noses in the flower beds. The weekend is here, and with US inflation numbers due next Wednesday, it’s the perfect excuse to sit tight and do nothing.

Wall Street Leads the Pack

Asian equity indexes closed with robust gains. Australia’s ASX 200 finished up 1.25%, while Japan’s Topix rose 0.88%. European bourses are trading higher, led by a 0.56% gain in the French CAC 40 index. Yesterday’s S&P 500 rally of 2.30% still leaves the index down 2.3% since last Friday, and S&P 500 futures (+0.18%) suggest the index will end the week with a loss.

EURUSD

EURUSD is at the bottom of it 1.0911-1.0929 band. The Euro area economic calendar was empty and no ECB policymakers were heard, leaving traders to bide their time until next week when there will be plenty of top tier Eurozone and US economic reports available. EURUSD is modestly bid above 1.0890.

GBPUSD

GBPUSD is steady in a 1.2773 to 1.2737. Next week is a big week for UK data with employment data out Tuesday, followed by inflation, PPI, and Retail Sales Wednesday. GBPUSD is underpinned by speculation that the Bank of England will leave UK rates steady for the near term, while the FOMC cuts rates by up to 50 bps next month.

USDJPY

USDJPY consolidated yesterday’s gains in a 146.72-147.82 range after soaring from 145.43 to 147.55 following Thursday’s US jobless claims numbers. The prospect of sharply lower rates and dovish comments from BoJ Deputy Governor Shinichi Uchida fueled the moves.

AUDUSD and NZDUSD

AUDUSD is trading at its session low in a 0.6570-0.6605 range as risk sentiment sours with falling S&P 500 futures.

NZDUSD is steady in 0.6002-0.6036 band with traders focused on the Wednesday’s RBNZ meeting

USDMXN

USDMXN shrugged off higher-than-expected inflation data and a 25 bp rate cut to 10.75%, falling from a peak of 19.3364 yesterday to 18.7759 today.

Bitcoin (BTCUSD)

BTCUSD rallied yesterday and extended the gains overnight, trading in a 56,792-62,770 band. Prices are supported by improved risk sentiment as yesterday’s US jobless claims data eased fears of a hard landing.

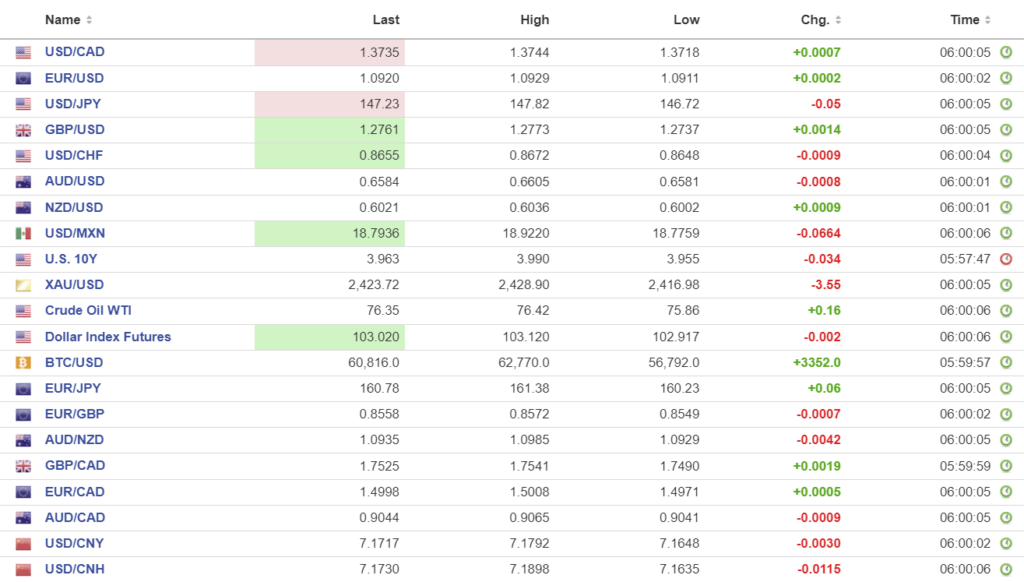

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1449 vs exp. 7.1690 (prev. 7.1460)

Shanghai Shenzhen CSI 300 rose 0.04% to 3342.94.

July CPI rose 0.5% m/m, previous -0.2%. Producer prices fell 0.8%, unchanged from June. The results CPI gain was attributed to seasonal factors,

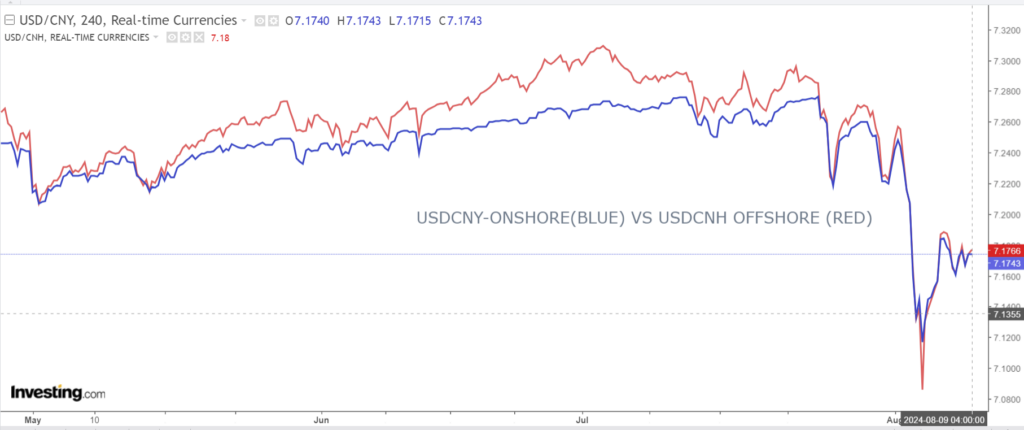

Chart: USDCNY and USDCNH

Source: Investing.com