Photo:Bing Image Creator

August 23, 2023

- Weak UK Services PMI sinks pound.

- USD dollar is rangebound but with a bid.

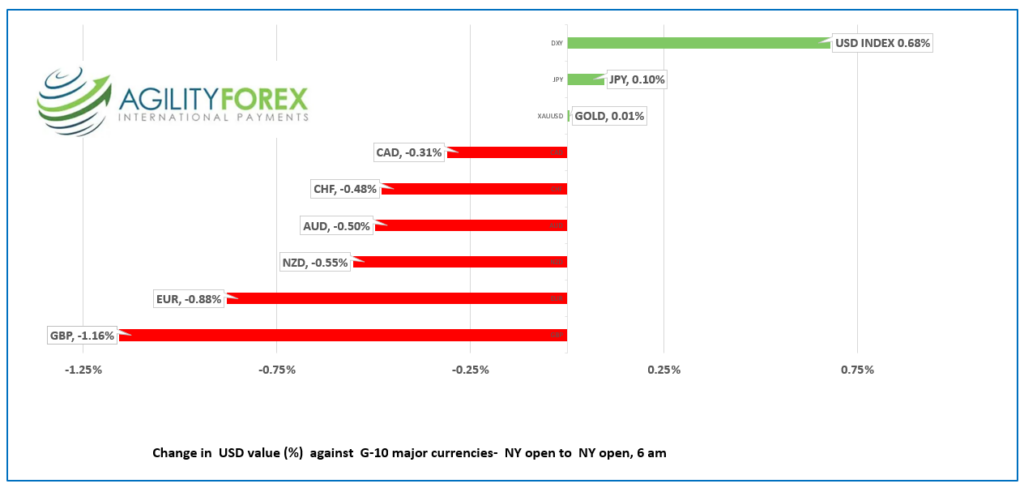

FX at a Glance

Source: IFXA/R

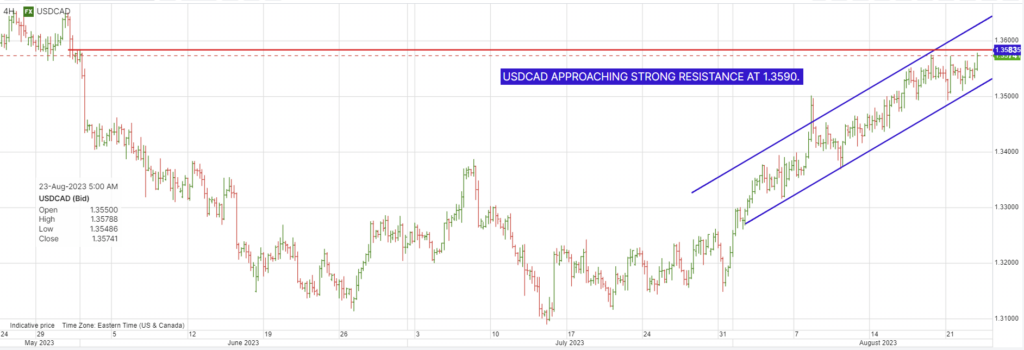

USDCAD Snapshot: open: 1.3566-70, overnight range: 1.3533-1.3592, close 1.3551.

USDCAD continued to grind higher following this mornings release of June retail sales data. Core retail Sales (ex-autos) fell 0.9% compared to forecasts for a 0.3% increase. Statistics Canada said “the largest sales declines were seen at general merchandise retailers (-1.4%) and food and beverage retailers (-0.9%). The decline at food and beverage retailers was primarily due to lower sales at beer, wine, and liquor retailers (-2.8%)

Headline Retail sales rose 0.1% compared to Statistics Canada’s advance estimate for 0.0%. The advance estimate for July is 0.4%.

The results help alleviate any pressure on the Bank of Canada to raise interest rates on September 6, as it is evidence that previous rate hikes are leaving a mark.

USDCAD may also be seeing some support from WTI oil prices which have fallen for the third day in a row. WTI is near the low of its $78.31-$79.89 overnight range, partly because of the firmer US dollar. Traders appear to be more concerned with the risk of slowing global demand then they are by news that the API reported a 2.41 million barrel drop in US crude stocks last week.

Canada Retail sales ex-autos are expected to have risen by 0.3% m/m in June while the headline number is flat.

USDCAD Technicals

The intraday USDCAD technicals are bullish with the August uptrend channel intact between 1.3510 and 1.3630. USDCAD has strong resistance at 1.3590 which has capped rallies since May 31. A decisive break above this level targets 1.3680 which is the 61.8% Fibonacci retracement level of the March-July range.

For today, USDCAD support is at 1.3530 and 1.3510. Resistance is at 1.3570 and 1.3640. Today’s range 1.3530-1.3630.

Chart: USDCAD daily

Source: Saxo Bank

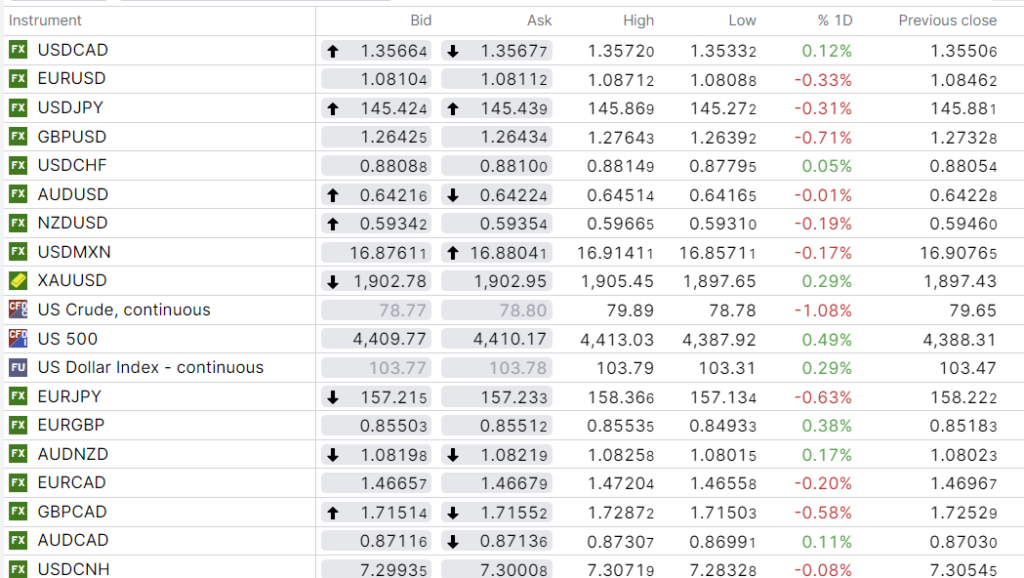

G-10 FX recap

The US dollar rally resumed yesterday morning and then gained fresh legs overnight from weaker-than-expected PMI data. The major central banks are united in claiming that rate decisions are data-dependent, and today’s data make those rate hike decisions more difficult.

The US 10-year Treasury yield slid from yesterday’s 4.36% peak to 4.265% this morning. There was not any specific catalyst for the decline.

Asia equity markets ignored the sell-off in the Shanghai Shenzhen 300 index and bought stocks. Japan’s Nikkei 225 index closed with a 0.46% gain, while Australia’s ASX 200 finished with a 0.38% increase.

European stock traders are bullish. The German DAX index is up by 0.157%, while the UK FTSE 100 index has risen by 1.01%. S&P 500 futures have climbed by 0.47%.

The latest US dollar rally appears to be in response to a Wall Street Journal article published at 5:30 am. Fed reporter Nick Timiraos writes that former St Louis Fed President James Bullard believes the US economy faces new risks of stronger growth which would necessitate higher interest rates.

EURUSD is at the bottom of its overnight 1.0807-1.0871 range in early NY trading. Prices were meandering higher at the session peak when German and Eurozone PMI data were released. German Services PMI (actual 47.3 vs forecast 51.5) and composite PMI (actual 44.7 vs forecast 48.3) disappointed, as did Eurozone Services PMI (actual 48.3 vs forecast 50.3). Analysts suggest the results make the ECB rate decision more difficult, as wage pressures are increasing services inflation but growth is deteriorating.

GBPUSD plunged to 1.2627 from 1.2764 in the wake of sharply weaker-than-expected UK Services PMI (actual 48.7 vs July 51.5). Bank of England officials may be smiling as it would appear that its rate hikes are finally starting to bite.

USDJPY dropped to 145.27 from 145.87 due to lower US Treasury yields. USDJPY topside moves from higher Treasury yields will be vulnerable to FX intervention.

AUDUSD traded defensively in a 0.6413-0.6453 range due to soft PMI data and concerns around China’s economic growth.

NZDUSD drifted in a 0.5929-0.5967 range. Prices were weighed down by soft Retail Sales data, which suggested GDP may be weaker than expected.

US July New Home Sales data is ahead.

Top of Form

FX high, low, close

Source: Saxo Bank

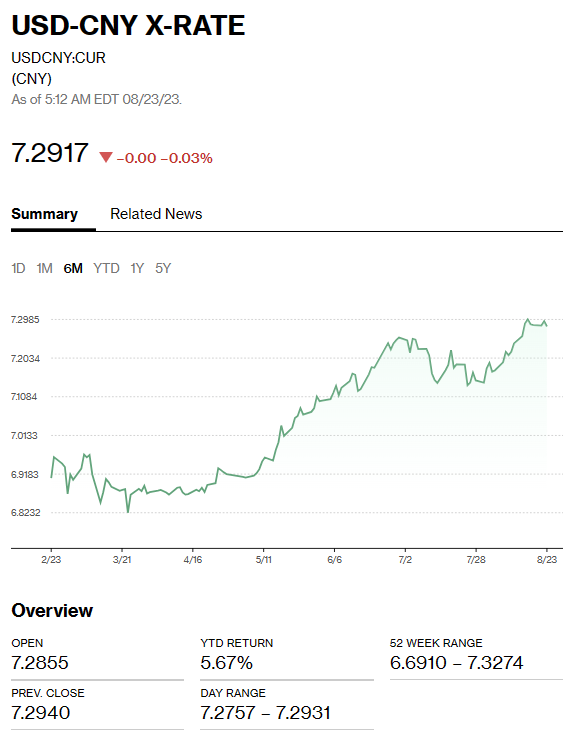

China Snapshot

Bank of China Fix: today 7.1988, expected 7.3050, previous 7.1992.

Shanghai Shenzhen CSI 300 fell 1.64%% to 3696.63.

PBoC said that reports of some banks permanently freezing some savings accounts are false.

Chart: USDCNY 1 month

Source: Bloomberg