January 31, 2024

- Canada November GDP rises 0.2%-beats forecast.

- ADP employment falls 51,000 to 107,000

- US dollar opens with a bid.

FX at a glance

Source: IFXA

USDCAD Snapshot: open 1.3428-32, overnight range 1.3397-1.3433, close 1.3399.

USDCAD is ticking lower in the wake of the slightly better than expected November GDP report which showed the Canadian economy grew by 0.2%, compared to the 0.1% forecast. Statistics Canada is predicting 0.3% growth in December. Canada may have avoided a recession but the Canadian data pales in the face of the US Q4 GDP growth rate of 3.4% tested.

The IMF ranked Canada to be the third fastest-growing advanced economy (forecast 1.4%) in 2024 behind the US and Japan, which is far more optimistic than the Bank of Canada’s 0.8% forecast.

US ADP employment was a lot weaker than expected which is helping to drive USDCAD down to its overnight low but the focus is on this afternoons FOMC meeting.

USDCAD Technicals:

The intraday USDCAD technicals are bearish while trading below 1.3440 and looking for a decisive breach of 1.3380-1.3400 support to extend losses to 1.3320 then 1.3260. A break above 1.3460 shifts the focus to 1.3550. Fibonacci retracement of the January 2024, 1.3180-1.3550 range points to support at 1.3400 (38.2% Fibo retracement level) and stronger support at 1.3360 (61.8% Fibo). For today, USDCAD support is at 1.3380 and 1.3350. Resistance is at 1.3450 and 1.3490. Today’s range is 1.3360-1.3460

Chart: USDCAD daily

Source: Daily FX

G-10 FX recap

ADP Employment fell 51,000 to 107,000. It was 158,000 in December and analysts were looking for a smaller decline to 145,000. The results improved the odds of a March rate cut to 50% from 40.4% yesterday but that may change after the FOMC meeting today.

Equity traders are grumpy, Elon Musk is fuming, bond traders are cautious, and US dollar traders are flexing their muscles. Shareholders were underwhelmed with Alphabet and Microsoft earnings reports and knocked stock prices lower overnight.

A Delaware judge said voided the $56 billion pay package that Tesla directors gave Musk. The Judge essentially said that the compensation process was flawed as the directors were Musk-puppets.

Bond traders appear to believe that US rates are not going any higher and that the Fed will cut rates in March which is one of the reasons that the US 10-year Treasury yield has dropped to 4.02% today. It touched 4.10% yesterday after the US JOLTS job openings data showed job openings rose in December. It also showed that fewer Americans quit their jobs which may be because a slew of American companies are laying off employees including, Alphabet, Amazon, Blackrock, Citigroup, eBay, Microsoft, Salesforce, and UPS.

The IMF World Economic Outlook is rather optimistic and forecasts that global growth will rise 3.1% in 2024, an improvement over its October forecast of 2.9%.

The FOMC is universally expected to leave rates unchanged and will likely acknowledge that the next rate move is a cut, but unfortunately, the timing of such a move is uncertain.

EURUSD see-sawed in a 1.0806-1.0848 range which is almost identical to yesterday’s band, then climbed to 1.0861 in NY, post ADP. Yesterday, ECB President Christine Lagarde said, “if we have the option of either hiking or cutting, will be a cut.” That comment helped to limit EURUSD gains. German inflation rose just 2.9% y/y compared to 3.7% in December, but the drop is mostly due to base effects.

GBPUSD traded in a 1.2683-1.271 range and is at the top of its band in NY. UK Nationwide Housing Prices rose 0.7% compared to the forecast for a 0.1% rise.

USDJPY traded in a 147.19-147.50 range and is sitting at 147.50. Prices were underpinned after the BoJ’s Summary of Opinions showed policymakers still had a dovish bias.

AUDUSD is at the top of its 0.6559-0.6604 range following US dollar selling pressure after the ADP report. Australian inflation dropped sharply in December (actual 3.4% y/y vs November 4.3%) leading to speculation that the RBA will need to cut rates sooner than expected.

The Chicago Purchasing Managers Index is due.

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

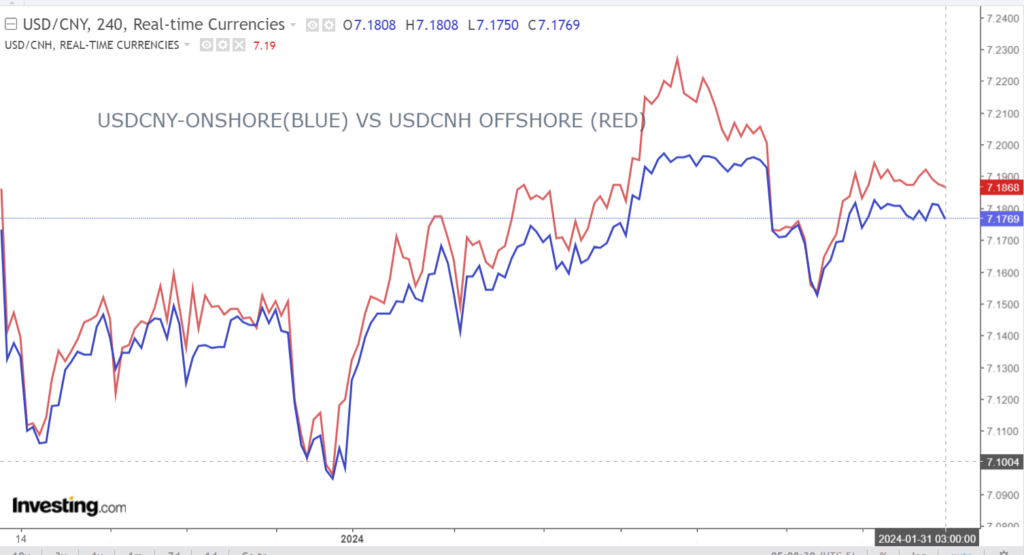

China Snapshot

PBoC fix: today 7.1739, expected 7.1727, previous 7.1055.

Shanghai Shenzhen CSI 300 fell 0.91% to 3215.36.

Official China January Manufacturing PMI 49.2 (forecast 49.2, December 49.0)

January Non-Manufacturing PMI 50.7 (forecast 50.6, previous 50.4)

Chart: USDCNY and USDCNH 4 hour

Source: Investing.com