November 22, 2019

USDCAD open 1.3281-1.3285 (6:00 am EST) Overnight Range 1.3256-1.3286

At first glance, the headline Canada Retail Sales number for September was disappointing as it showed a drop of 0.1% m/m. It wasn’t. When motor vehicles and parts sales were stripped out, Retail Sales rose a healthy 0.7%. USDCAD sank on the news, breaking below support at 1.3270 to 1.3256.

The FX majors were little changed overnight, but the US dollar is poised to end the week with solid gains across the G-10 major currency spectrum. A mixed bag of Eurozone data, and negative risk sentiment from US/China trade talks renewed dollar demand during the European session.

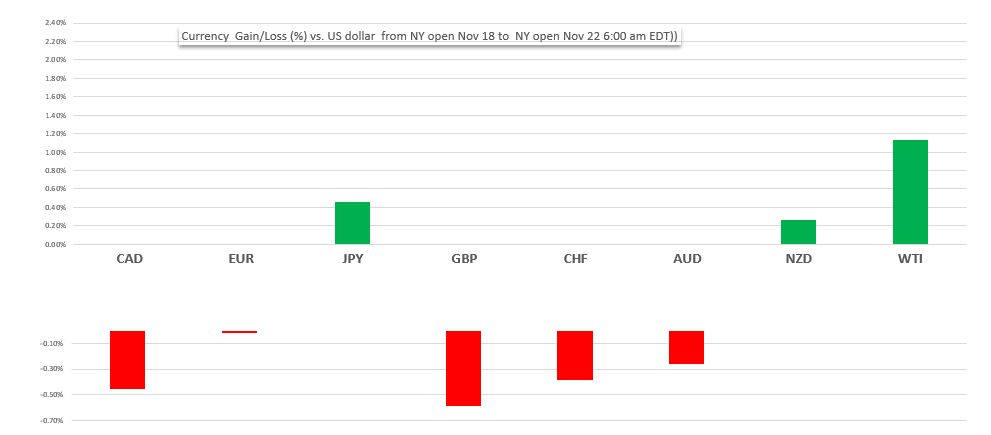

As of 6:00 am EST today, the British pound is narrowly beating the Canadian dollar for the title of biggest currency loser compared to Monday’s 6:00 am New York open.

FX Market Snapshot

Change in currency value against the US dollar from Nov 18 NY open to Nov 22 NY open

Source: Saxo Bank/IFXA

EURUSD traded erratically at the start of the European session. German Q3 GDP rose 1.0% y/y, as expected, which supported the single currency, initially. A mixed bag of Eurozone PMI data saw both sides of a 1.1048-1.1086 band touched before prices settled below 1.1060. Eurozone Markit Manufacturing PMI, at 46.6, beat the 46.4 forecasts but is still in contraction territory. ECB President Christine Lagarde said (stating the obvious) “the global environment is marked by uncertainty”

Chinese President Xi Jinping made noises about wanting to work out a Phase 1 trade deal, but also said China didn’t start the war and is not afraid of a fight.” On Tuesday Trump said “China is going to have to make a deal that I like … If we don’t make a deal with China, I’ll just raise the tariffs even higher.” Those comments suggest hopes for a near term trade deal are unwarranted.

GBPUSD plunged to 1.2865 from 1.2928 after Market Manufacturing, and Services PMI were weaker than expected and the lowest readings since the Brexit vote. Some economists noted that the data is consistent with a drop of 0.3% in Q4 GDP.

USDJPY drifted in a 108.54-70 range with FX price action tracking US Treasury yields. Rising yields lifted USDJPY to the top of the range while mild risk aversion sentiment and dip in yields just before New York opened, sent prices to the bottom.

NZDUSD outperformed AUDUSD this week and overnight with widening interest rate differentials favouring Kiwi. AUDUSD is suffering from a dovish central bank outlook and fears of a prolonged US/China trade war.

WTI oil prices have held on to most of this week’s gains. Rising expectations that Opec and Russia will extend production cuts for another three months have offset lower demand concerns due to the China/US trade war.

USDCAD dropped from 1.3320 to 1.3267 yesterday when BoC governor told an Ontario Securities Institute audience that the BoC “has monetary conditions about right, for the current situation.” Traders interpreted that statement to mean Canadian interest rates will stay unchanged which is the exact opposite of what they thought after Deputy Governor Wilkins speech, Tuesday.

Canada September Retail Sales data (forecast -0.1%) and Retail Sales, ex-autos (forecast 0.1%) will provide some short-lived excited for USDCAD

US data includes Michigan Consumer Confidence (forecast 95.7) US Thanksgiving is next Thursday, and it is a big holiday week for Americans, which suggests a quiet afternoon session.

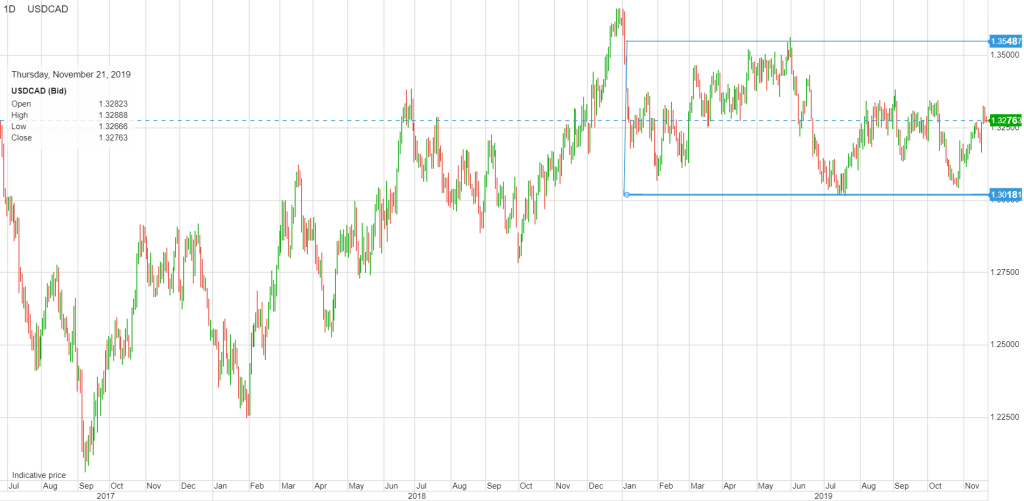

USDCAD Technical View

The intraday USDCAD technicals flipped again. Now they are bearish. The break below 1.3290 shifts the focus to support at 1.3220. However, longer-term, the flip-flop in direction is just noise. The uptrend from the end of October is solidly in place above 1.3220. While trading at 1.3280-ish, USDCAD is in the middle of its 1.3020-1.3550 range, which has contained price action since the beginning of the year. For today, USDCAD support is at 1.3240 and 1.3220. Resistance is at 1.32900 and 1.3310. Today’s Range 1.1.3240-1.3290

Chart: USDCAD daily

Source: Saxo Bank