Photo:Rolling Stones.

August 11, 2023

- Markets appear lost and are looking for a fresh catalyst.

- US PPI rises a tad more than expected

- USD dollar consolidates Thursday’s gains.

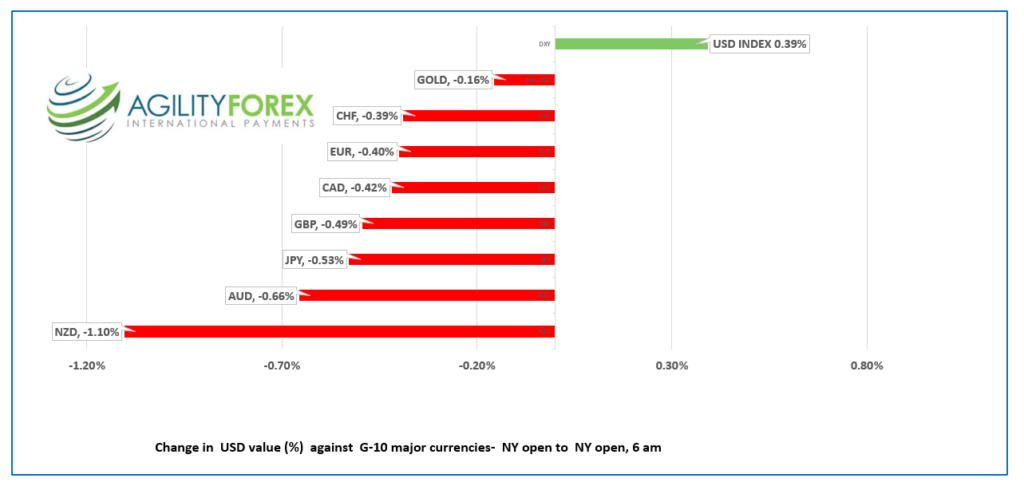

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open: 1.3456-60, overnight range: 1.3428-1.3459, close 1.3448

USDCAD traded with a “up-down-up-down” pattern all week and that doesn’t look to be changing any time soon. Global risk sentiment has soured and that has put a damper on Canadian dollar demand while this week’s oil price rally stalled out below resistance in the $85.00/b area.

The oil price rally could resume today after the International Energy Agency (IEA) warned ” “Deepening OPEC+ supply cuts have collided with improved macroeconomic sentiment and all-time high world oil demand.” On the other hand, the IEA forecast was expected.

USDCAD will find direction from S&P 500 and US 10-year Treasury yields.

USDCAD Technicals

The intraday USDCAD technicals are bullish above 1.3360, looking for a decisive break above 1.3500 to extend gains to 1.3560 then 1.3660. A break below 1.3360 targets 1.3290.

Longer term, USDCAD has a bullish bias above 1.3080, the uptrend line from June 2021 with prices trapped inside a trapped in a wide 1.3090-1.3990 range that has contained price action since September 2022.

For today, USDCAD support is at 1.3400 and 1.3360. Resistance is at 1.3460 and 1.3490. Today’s range 1.3390-1.3490.

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap

Yesterday, traders were dusting off their rally pants, expecting that a below-forecast CPI print would trigger a big stock market rally and a US dollar sell-off. They got the result but not the rally leaving many singing “I can’t get no satisfaction.”

The good news was that US CPI rose a lower than expected 3.2% (forecast 3.3% y/y) in July while Core CPI rose 4.7% y/y vs 4.8% in June. The bad news was that bond traders were focused on the US 30-year Treasury auction.

It went poorly. Treasuries sold for 4.189%, the highest level since 2011. The 30-year yield was 4.233% at the close and is 4.272% in NY today. The surge in 30-year Treasury yields boosted the 10-year yield, which sparked US dollar demand and knocked equities lower.

Things didn’t improve much overnight. Traders are looking at more current information like rising oil prices, and a still tight labor market and starting to buy into Fed Chair Powell’s comments from the last FOMC meeting when he said, “We intend to keep policy restrictive until we’re confident inflation is coming down sustainably to our 2% target, and we’re prepared to further tighten if that’s appropriate.”

Today’s US Producer Price Index data supports Powell’s view. PPI rose 0.3% m/m in July (forecast 0.2%, June 0.0%) while the ex-food and energy component rose 0.3% (forecast 0.2% June -0.1%)

Asian equity indexes closed with gains led by a 0.84% increase in Japan’s Nikkei 225 index, although the rally was mainly due to the softer yen. European bourses are all in negative territory, and S&P 500 futures are down 0.27%. The US 10-year yield is slightly firmer at 4.125% (close 4.08%).

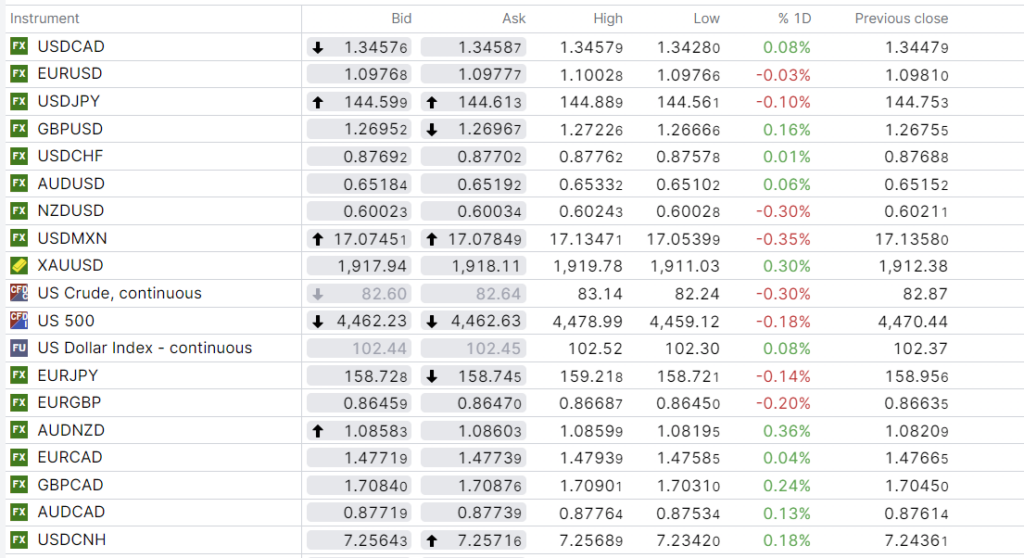

EURUSD traded negatively in a 1.0974 to 1.1002 range The single currency is struggling due to the rebound in US dollar demand, but getting a modicum of support slightly higher than expected French inflation.

GBPUSD chopped about in a 1.2667-1.2738 range and is in the middle of that band in NY trading. Prices were supported by better than expected data. The economy grew at a better pace than economists expected with Q2 GDP rising 0.2% q/q( forecast 0%). In addition, Manufacturing Production (actual 2.4% m/m, forecast 0.2%), and Industrial Production (actual 1.8% m/m vs forecast 0.1%) were stronger than predicted as well.

USDJPY is at the top of its 144.56 to 144.89 range due to firmer US Treasury yields. However, traders were cautious as they expect Bank of Japan intervention on a break above 145.00.

AUDUSD traded narrowly in a range of 0.6510 to 0.6533. Soon-to-be-ex Governor Philip Lowe said Australian rates are restrictive and predicted that the worst is over for inflation.

FX high, low, close

Source: Saxo Bank

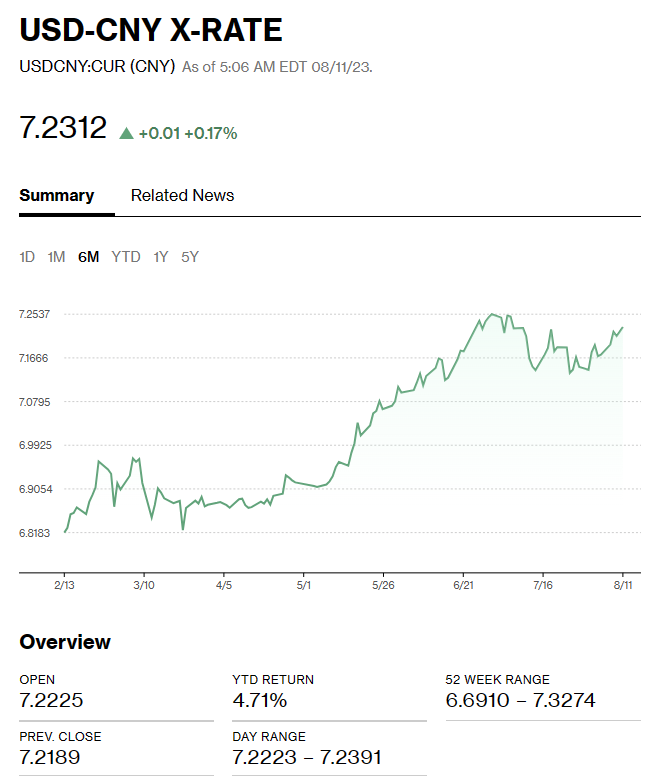

China Snapshot

Bank of China Fix: Today 7.1587 , expected 7.2193, previous 7.1576.

Shanghai Shenzhen CSI 300 fell 2.30% to 3884.25.

Property developer, Country Garden Holdings, continued to free-fall overnight, adding to the negative stock market sentiment, and raising fears about a Chinese-made debt crisis.

Chart: USDCNY 6 month

Source: Bloomberg