Photo: Bing AI

October 25, 2023

- US dollar resumes rally.

- Bank of Canada expected to leave rates unchanged.

- US dollar extends yesterdays gains-GBPUSD underperforms.

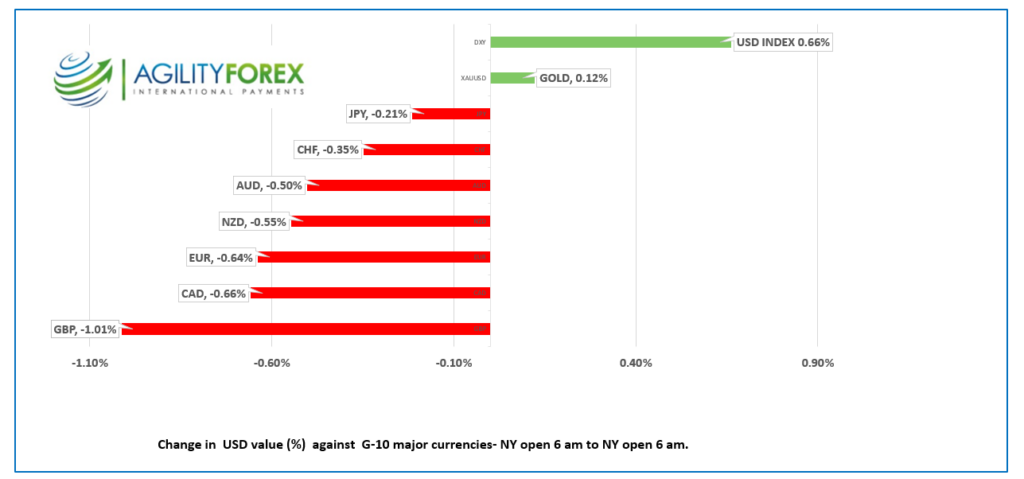

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open: 1.3775-79, overnight range 1.3730-1.3784, close 1.3742

USDCAD rallied yesterday and then added to its gains overnight, fueled by widespread US dollar demand and modestly lower WTI oil prices. The impact of oil prices may be even more significant, as Canada’s largest crude export, Western Canada Select (WCS), is trading at a US$47 discount. This substantial discount is partly due to a decline in demand from US Midwest refineries.

WTI oil traded within a range of $83.17 to $84.01 overnight, with traders overlooking the API data that indicated a fall in crude inventories by 2.67 million barrels last week.

USDCAD may also be receiving support due to market expectations that the Bank of Canada will not raise interest rates at today’s meeting. The statement is anticipated to have a somewhat hawkish tone, warning of additional rate hikes if incoming data supports such a move. However, given that forward-looking central bank statements have frequently been inaccurate since the onset of Covid, they do not carry much weight nowadays.

USDCAD Technicals:

The USDCAD technicals are bullish across hourly, 4-hour, and daily charts. The hourly chart reveals an uptrend line from yesterday, coming into play above 1.3740, while the 4-hour chart’s uptrend line is at 1.3680. The daily chart’s uptrend line sits at 1.3200. All charts suggest that a decisive break above the 1.3790-1.3800 range could extend gains to 1.4000 to start, although resistance is expected at 1.3890.

For today, USDCAD support is positioned at 1.3740 and 1.3680, with resistance at 1.3790 and 1.3860. Today’s expected trading range is between 1.3730 and 1.3830.

Chart: USDCAD daily

Source: Investing.com

G-10 FX recap

The US dollar caught a bid yesterday and rallied hard, although there were no specific catalysts to explain the sudden move. It could have been sparked by relief from the apparent ceasefire in the US Republican Party’s war with itself. The GOP may have found a palatable candidate for Speaker of the House which, if so, reduces the risk of a government shutdown in November. It could have been triggered by weak European and UK PMI data, underscoring the growing economic divergence with the US. It could have been because the 10-year US Treasury yield found a bit of a floor in the 4.80% area. In addition, headlines may have raised fears that Western nations will get sucked into a Middle East war against Iran and its proxy terrorist groups. Or the rally could have been due to a combination of the above.

It’s not unusual. FX markets tend to see screwy moves ahead of FOMC meetings, and without any actionable US data on tap today, the same should hold true today.

Asian equity indexes closed with Japan’s Nikkei 225 advancing by 0.67% and Australia’s ASX closing nearly unchanged. European bourses are trading in negative territory while S&P 500 futures are down. The US 10-year Treasury yield is at 4.863%.

EURUSD turned bearish and dropped from a peak of 1.0696 yesterday to a low of 1.0566 today. The single currency did not get much support from higher-than-expected German Ifo survey results. Business climate was 86.9 (forecast 85.9), Current assessment was 89.2 (forecast 88.5), and Expectations were 84.7 (forecast 83.3).

The Ifo press release said, “Companies are more satisfied with their current business and were less pessimistic in their views for the coming months.” Others disagreed. The UK Guardian quoted Capital Markets Senior European economist Franziska Palmas, who said, “The small rise in the Ifo business climate index (BCI) in October still left the index in contractionary territory, echoing the downbeat message from the composite PMI released yesterday.”

GBPUSD sank like a stone yesterday, falling from 1.2290 to close at 1.2159, then added to those losses overnight in a 1.2114-1.2177 range. The catalyst for the move was yesterday’s soft PMI data combined with broad-based US dollar demand after Treasury yields appeared to find a floor. The intraday GBPUSD technicals are bearish below 1.2170, with a break below 1.2100 targeting the October low of 1.2040.

USDJPY barely budged, inside a 149.79-149.94 range. The yen dynamics are unchanged. USDJPY support stems from the outlook for a hawkish Fed meeting on November 1, and firmer Treasury yields which is countered by speculation that the BoJ will soon tighten monetary policy and fear of BoJ intervention on a move above 150.00.

AUDUSD traded in a 0.6340-0.6400 range with the top occurring in the aftermath of hotter-than-expected inflation data. September CPI rose 5.4% y/y (forecast 5.3%) and 1.2% q/q (forecast 1.1%), which raised the odds for the RBA to raise rates by 0.25% on November 6. The rally was short-lived, and firmer US treasury yields and soft European equity markets sent AUDUSD to its session low in early NY trading.

There is no significant US data available.

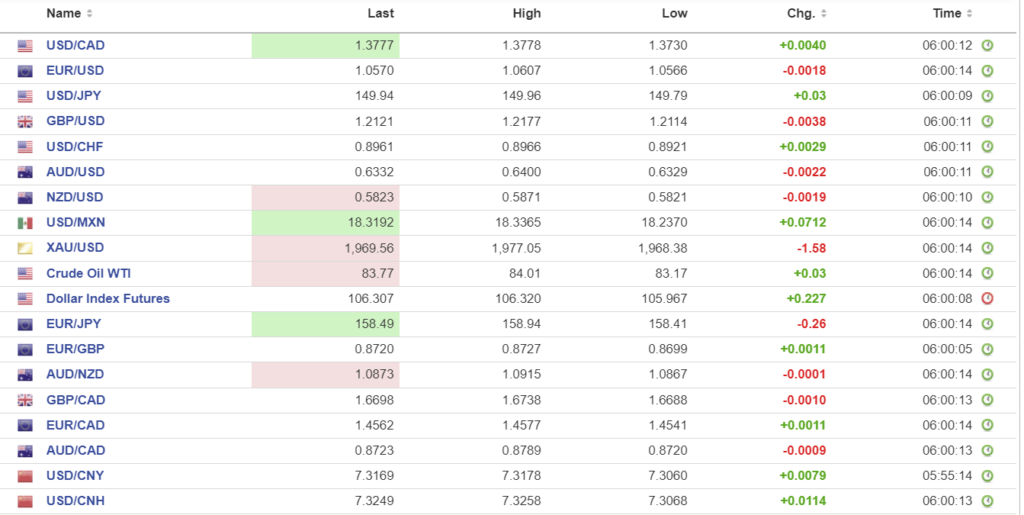

FX high, low, open

Source: Investing.com

China Snapshot

PBoC fix: today 7.1785, expected 7.3213, previous 7.1786.

Shanghai Shenzhen CSI 300 rose 0.50% to 3504.46.

China announces new stimulus by increasing the fiscal deficit by $137.0 billion (one trillion yuan) the first increase of the budget deficit above 3.0% since 2008. The move is designed to signal that authorities are committed to supporting growth.

The news is too late for Country Garden Holdings Co. The company is in default on a dollar bond and principal and interest is due immediately, if those holding at least 25% of the outstanding amount, demand it.

Chart: USDCNY (onshore) vs USDCNH (offshore)

Source: Investing.com