Source: Pixabay

- Year of the Tiger begins

- Canada November GDP beats estimates

- US dollar gives back some of month-end gains

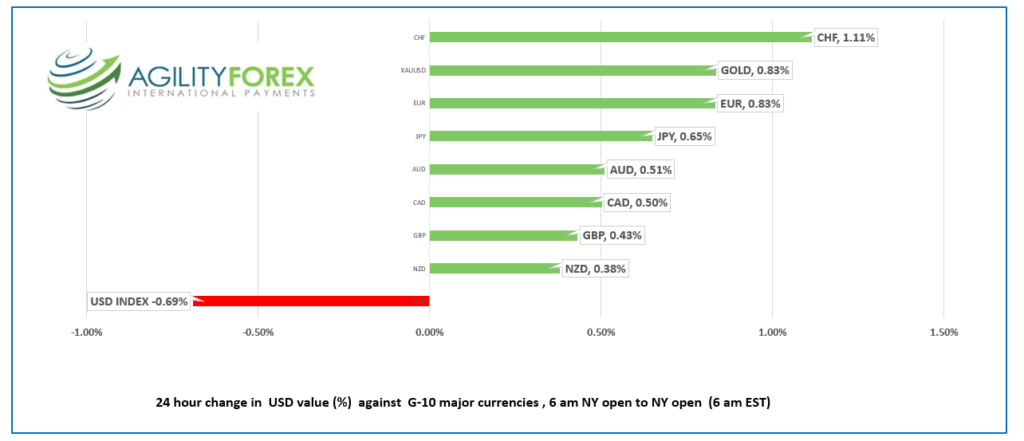

FX at a Glance

Source: IFXA Ltd/RP

USDCAD Snapshot: Open 1.2674-78, Overnight Range-1.2657-1.2721, previous close 1.2707

Canada’s economy is now 0.2% pre-pandemic February 2020 level, a notable achievement considering the disruption from BC floods in November. November GDP rose 0.6% m/m, more than double the 0.3% that was expected.

Alas, the stellar results did not have any immediate impact on the currency

Nevertheless, USDCAD is well below yesterday’s peak level as it continues to consolidate Monday’s losses that occurred after the 11:00 am fixing portfolio rebalancing window slammed shut. The USDCAD sell-off was not driven by any domestic factors but by broad US dollar weakness.

WTI oil dropped as well, but prices bounced off of support in the $86.60/barrel area and are trading at $87.54 in NY. WTI continues to be supported by bullish price forecasts due to an expected demand rebound, and by geopolitical issues.

Price action is directed by the hawkish Fed rate outlook even though the Bank of Canada outlook is similar. Forecasters are predicting 0.25% hikes in 2022 in both countries.

Technical view: The intraday USDCAD technicals turned bearish due to the failure to break above resistance at 1.2810 and yesterday’s drop below 1.2710, which snapped the January uptrend. Further losses below 1.2640 will target 1.2550. A move above 1.2810 puts 1.3000 in play.

For today, USDCAD support is at 1.2640 and 1.2590. Resistance is at 1.2710 and 1.28540. Today’s Range 1.2640-1.2720

Chart USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

It’s the Year of the Tiger. If it is your birth year you are vigorous and ambitious, daring, and courageous, enthusiastic, generous, self-confident with a sense of justice and a commitment to help others for the greater good.

Those qualities will be in high demand in 2022 as Covid lingers, oil prices rise, Russia wants to remake the USSR, Middle East tensions flare, and China salivates over Taiwan.

The Lunar New Year celebrations made for a dull Asia session. The Nikkei 225 rose 0.26%, while Australia’s ASX 200 gained 0.49%. European bourses have started the new month with a positive outlook, with the German DAX rising 1.10% and leading the other indexes higher. Wall Street futures are flitting around flat as is WTI oil, while gold posted a small gain. The US 10 year Treasury yield is 1.752%.

A chorus of Fed officials reminded markets that US rates are going higher. Their comments weren’t new and didn’t cause much of a reaction.

EURUSD caught a bid yesterday, rallied throughout the session, and continued overnight, rising from 1.1222 to 1.1279 in NY. Eurozone PMI data, higher than expected French inflation results, and falling EU unemployment suggested that EU economies were recovering from Covid, adding to EURUSD demand. However, gains may be capped around the 1.1310 level ahead of Thursday’s ECB meeting.

GBPUSD rallied on broad US dollar weakness, rising from 1.3436 to 1.3513. Prices were supported by modestly better than expected UK Manufacturing PMI (actual 57.3 vs forecast 56.9) and UK Housing Prices, which rose 0.8% in January. The intraday technicals are bullish above 1.3420, looking for a break above 1.3520 to extend gains to 1.3600.

USDJPY retreated on the heels of the lower 10-year Treasury yield, dropping to 114.62 from 115.18.

AUDUSD rallied alongside the other G-10 currencies, rising from 0.7068 to 0.7102 while ignoring the dovish RBA monetary policy result. The RBA ended QE as expected, raised its inflation forecast, and provided an upbeat outlook for the economy. Then they stomped on any thought of raising interest rates saying, “ceasing purchases under the bond purchase program does not imply a near term increase in interest rates.”

NZDUSD rallied due to broad US dollar weakness, climbing to 0.6617 from 0.6687.

Chart of the Day: AUDUSD 30 minutes

Source: Saxo Bank

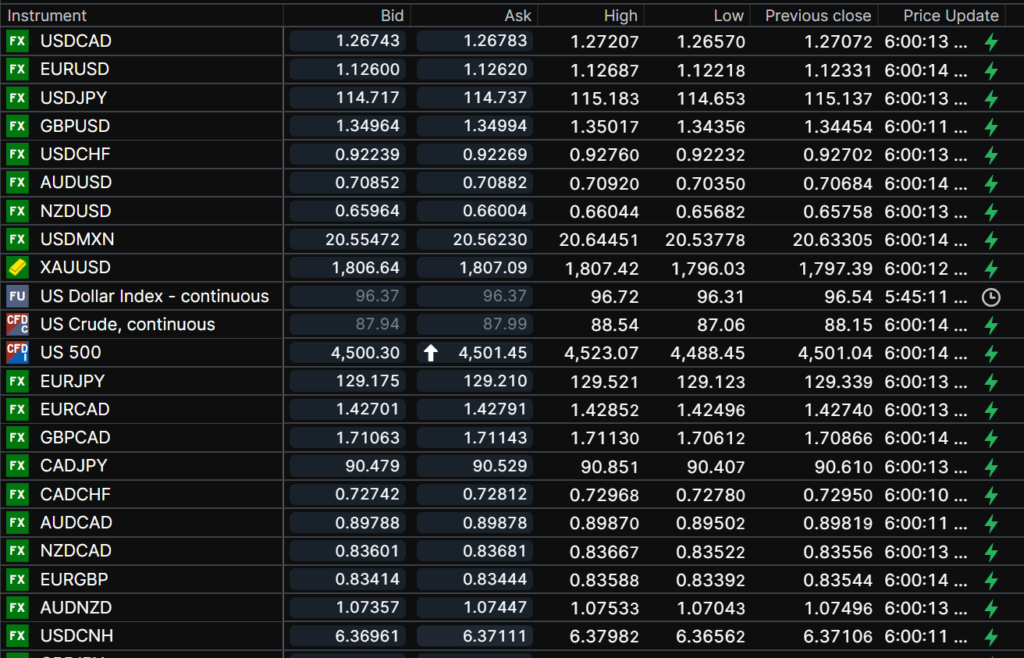

FX open, high, low, previous close as of 6:00 am ET

Chart: Saxo Bank

China Snapshot

Today’s Bank of China Fix 6.3746, previous 6.3746-Close

Shanghai Shenzhen CSI 300 closed

Chinese New Year-January 31 to February 15.

Chart: USDCNH 30 minutes

Source: Saxo Bank