March 18, 2024

- Six Central Bank meetings this week.

- Canada CPI due Tuesday

- US dollar opens on mixed note.

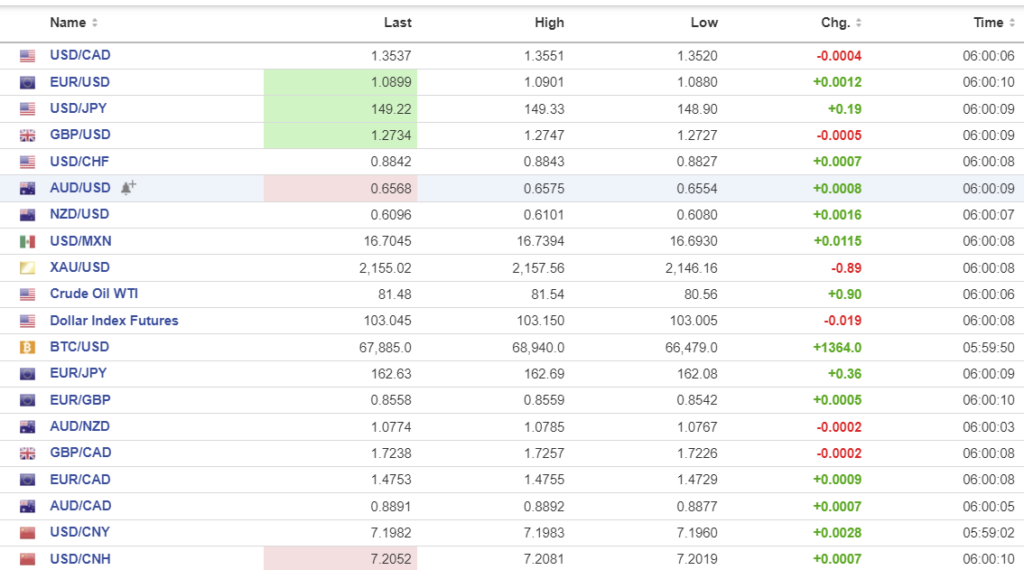

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open 1.3533-1.3537, overnight range 1.3520-1.3551, close 1.3545

USDCAD is consolidating Friday’s gains that were fueled by surging US Treasury yields which led to CAD/US interest rate differentials widening in favour of the US. Canadian inflation data is due on Tuesday. February CPI is expected at 3.1% y/y (previous 2.9%) with the monthly numbers at 0.6% compared to o% in January. Those are not rate cutting results which will underpin USDCAD.

WTI oil prices are in the middle of the $80.56-$8158 range after Chinese Retail Sales and Industrial Production data rose more than expected.

Canada Raw Materials rose 2.1% compared to a 1.2% increase in January. Industrial Product prices rose 0.7% m/m compared to -0.1% in January. The results did not have any impact on USDCAD trading.

USDCAD Technicals

The USDCAD intraday technicals are bullish above 1.3520, looking for a decisive break of resistance in the 1.3550-1.3560 area to extend gains to 1.3610. A move below 1.3520 suggests a retest of support at 1.3480 but only a move below 1.3440 negates the uptrend.

Longer term, the USDCAD uptrend line from the beginning of January is intact while prices are above 1.3450 and looking for a break above 1.3620 to extend gains to 1.3770. A break below 1.3440 targets 1.3350.

For today, USDCAD support is at 1.3520 and 1.3480. Resistance is at 1.3560 and 1.3590. Today’s range is 1.3480-1.3570.

Chart: USDCAD daily

Source: Investing.com

G-10 FX

The Leprechauns have returned to their enchanted forests, and the developed market central bankers are on the march. The FOMC meeting on Wednesday is bracketed by policy decisions from the BoJ and RBA tomorrow, and the BoE, SNB, and Banxico on Thursday. That meant Irish-for-a-day partiers could nurse their hangovers in peace.

Traders also ignored the Russian election results. Vladimir Putin managed to win another term by killing or imprisoning all opposition but even then, did not get 100% of the votes.

Japan’s Nikkei 225 index closed with a 2.67% gain, while Australia’s ASX 200 closed nearly flat. European bourses are in positive territory, led by a 0.20% gain in the German Dax. S&P 500 futures are up 0.39%.

EURUSD inched quietly higher , rising from 1.0880 to 1.0907-1.0901 range, Eurostat reported “The euro area annual inflation rate was 2.6% in February 2024, down from 2.8% in January. European Union annual inflation was 2.8% in February 2024, down from 3.1%.

GBPUSD is at the top of its 1.2727-1.2747 range. Wednesday’s UK inflation report is expected to show that Core CPI rose 4.6%, which is well-blow the January reading of 5.1%. The BoE may be encouraged by the results but not enough to suggest that they are close to cutting rates.

USDJPY is steady in a 148.90-149.33 band. Traders have ignored this morning’s slight increase in the US 10-year Treasury yield to 4.324% from 4.306% where it opened in NY. The odds that the BoJ ends its negative interest rate policy at tomorrow’s meeting are 50/50, supported by an article in on Nikkei news that claims a rate hike is likely.

AUD/USD is a tad firmer, rising from 0.655 to 0.6575. Traders do not expect a policy change a Tuesday’s RBA meeting.

NZD/USD traded firmer in a 0.6080-0.6101 range with prices getting a boost from Services Sector PMI, which was 53 in February (Previous 52.1). BNZ’s Head of Research, Stephen Toplis, said, “When we combine the PMI and PSI together to get an indicator of activity, there is a strong suggestion of growth returning later this year.”

USD/MXN traded cautiously in a 16.6930-16.7394 range with Mexican markets closed for a National holiday today. The Banxico monetary policy meeting is Thursday, where there is a risk of a rate cut.

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.0943 vs exp. 7.1995 (prev. 7.0975)

Shanghai Shenzhen CSI 300 rose 0.94% to 3603.53.

Analysts are concerned that the stronger than expected Industrial Production data suggests that authorities will delay adding more stimulus.

Retail Sales 5.50% y/y (forecast 5.2%) Industrial Production 7% (forecast 5.0% y/y)

NBS data shows property investment fell 9.0% in January and February 2024.

Chart: USDCNY and USDCNH daily

Source: Investing.com