Photo: Jim Davis

June 20, 2023

- China trims 1 and 5 year LPR, as expected.

- US housing and building permits data surprise to the upside.

- US dollar clawing back losses in early NY trading.

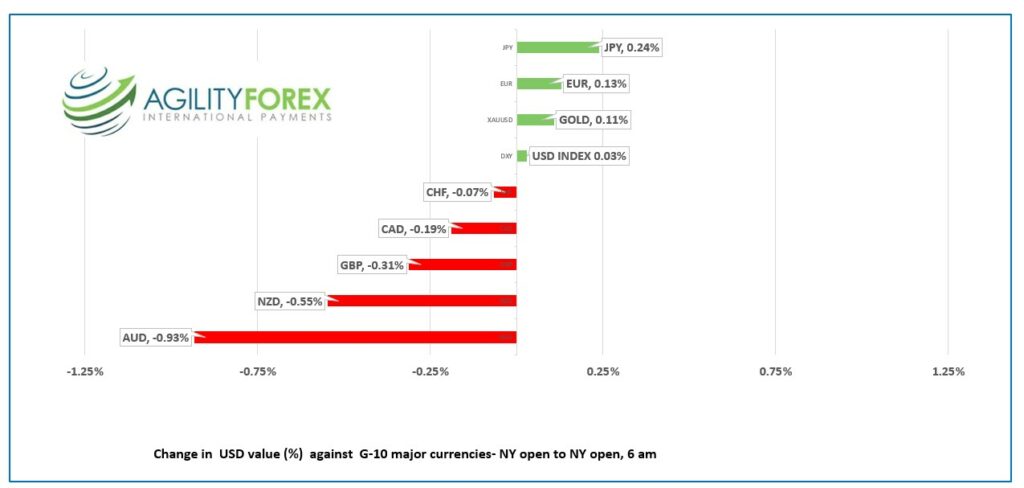

FX at a glance

Source: IFXA Ltd/

USDCAD Snapshot: open 1.3228-32, overnight range 1.3208-1.3237, close 1.3210

USDCAD is trading sideways albeit with a bearish bias and garnering a bit of support from higher oil prices. China announced well-telegraphed cuts to its 1 and 5-year Loan Prime Rates but as yet have not announced any fiscal stimulus, which is why markets are reluctant to embrace a risk-seeking mode.

Oil traders may be more optimistic. WTI rose from $70.63/b to $72.08, partly because a China fiscal stimulus package is expected to shore up demand.

USDCAD direction will track S&P 500 moves, as usual in the absence of actional Canadian economic reports.

USDCAD Technical Outlook

The USDCAD technicals are unchanged from yesterday. They are bearish and in a downtrend channel bound by 1.3080 and 1.3260.

The intraday technicals are mildly bullish above 1.3205, looking for a break above 1.3240 to test resistance at 1.3270 and perhaps 1.3340. A break below 1.3205 targets 1.3150.

The long term uptrend line at 1.2990 should limit losses initially.

For today, USDCAD support is at 1.3180 and 1.3150. Resistance is at 1.3240 and 1.3270

Today’s range 1.3170-1.3240

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

US markets are reopening with a cautious note after a long weekend due to a lack of top-tier data releases and ahead of Fed Chair Powell’s testimony to Congress on Wednesday.

US Secretary of State Anthony Blinken met with China President Xi Jinping, but markets are not reacting as much to reduce US/China tensions. Those tensions may worsen if China follows through on plans to build a military base in Cuba.

Asia equity indexes, except those in China, closed with small gains. The major Chinese indexes posted losses due to disappointment from a lack of fiscal stimulus announcements. European traders were cautious, and the major bourses are in the red, except for the UK FTSE 100 index, which is up by 0.10%. S&P 500 futures are down 0.28% (as of 5:30 am PDT)

US Housing Starts surged in May, rising 21.7% compared to the forecast for a 0.8% decline. Building Permits rose 5.2% instead of falling 5.0%. Both reports indicate that the US economy is chugging along, making it easier for the Fed to keep raising interest rates.

EURUSD drifted in a range of 1.0912-1.0945. There is a school of thought suggesting that the ECB will stop raising rates before the Fed. That’s because some policymakers are not as hawkish as President Lagarde. Chief Economist Philip Lane is one of them, saying, “At this point, we are surely data-driven. July is not so far away, we can say unless there’s a material change, another hike is likely, but to me, September is so far away.” The intraday EURUSD technicals are bullish around 1.0860.

GBPUSD is in retreat, having fallen from 1.2805 in Asia to 1.2737 in NY, mostly due to profit-taking after last week’s gains ahead of tomorrow’s key inflation report. Headline CPI is expected to fall to 8.4% from 8.7%, while core CPI remains unchanged at 6.8% y/y. The intraday GBPUSD technicals are bullish above 1.2630.

USDJPY is trading defensively in a range of 141.45-142.24, with the pressure stemming from a dip in the US 10-year Treasury yield from 3.826% to 3.734% before it climbed to 3.77% in NY.

AUDUSD is the worst-performing G-10 currency pair since yesterday’s open, falling from 0.6854 in Asia to 0.6772 in NY. The catalyst for the sell-off was the RBA minutes, which revealed that policymakers were less hawkish than expected.

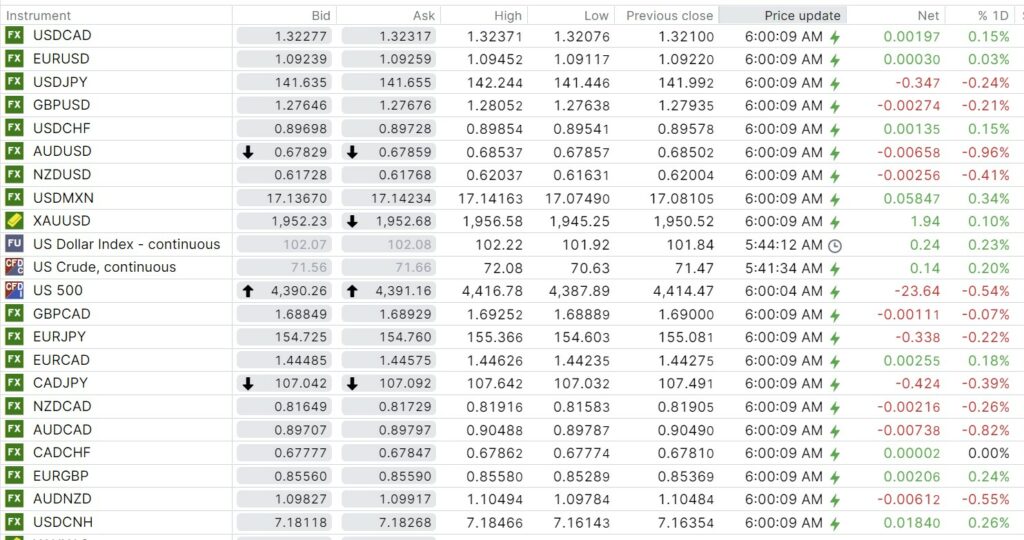

FX open, high, low, previous close as of 6:00 am ET

Source: Bloomberg

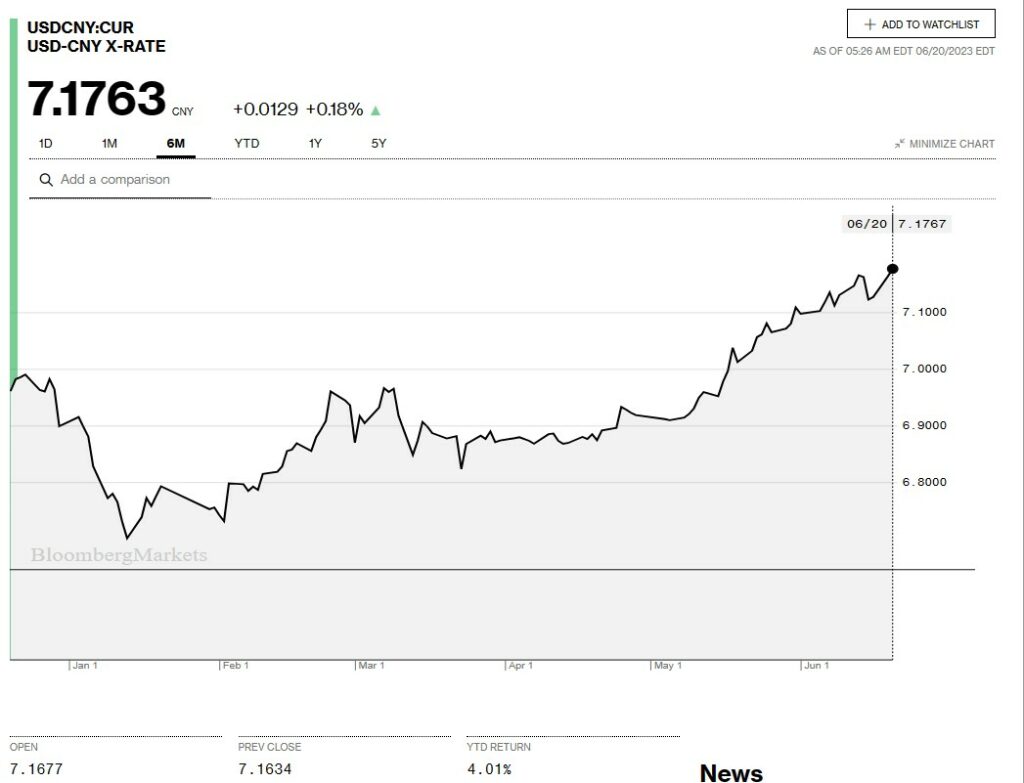

China Snapshot

Bank of China Fix: 7.1596, previous 7.1201.

Shanghai Shenzhen CSI 300 fell 0.17% to 3924.24.

PboC cuts 1-year Loan Prime Rate(LPR) to 3.55% from 3.65% and cuts 5-year LPR to 4.2% from 4.3%. the move was widely expected after announcing other rate cuts last week. However, a 10 bp cut is hardly the spark required to re-ignite a slumping economy and government officials have not delivered any new fiscal stimulus. Lots of talk, but no action.

Chart: USDCNY 6 month

Source: Bloomberg