March 12, 2024

- UK wage growth slows which supports eventual BoE rate cut.

- US CPI data hotter than hoped for

- US dollar moves higher post-CPI.

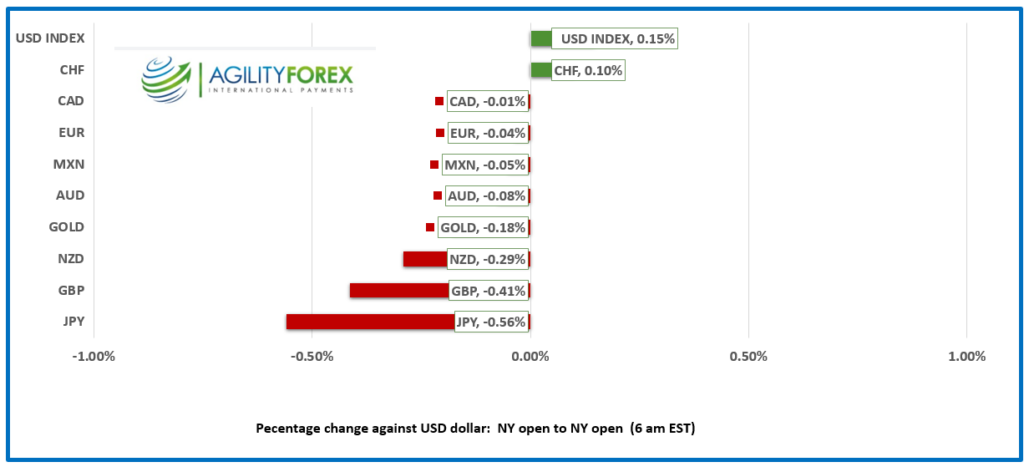

FX at a Glance

Source: IFXA/RP

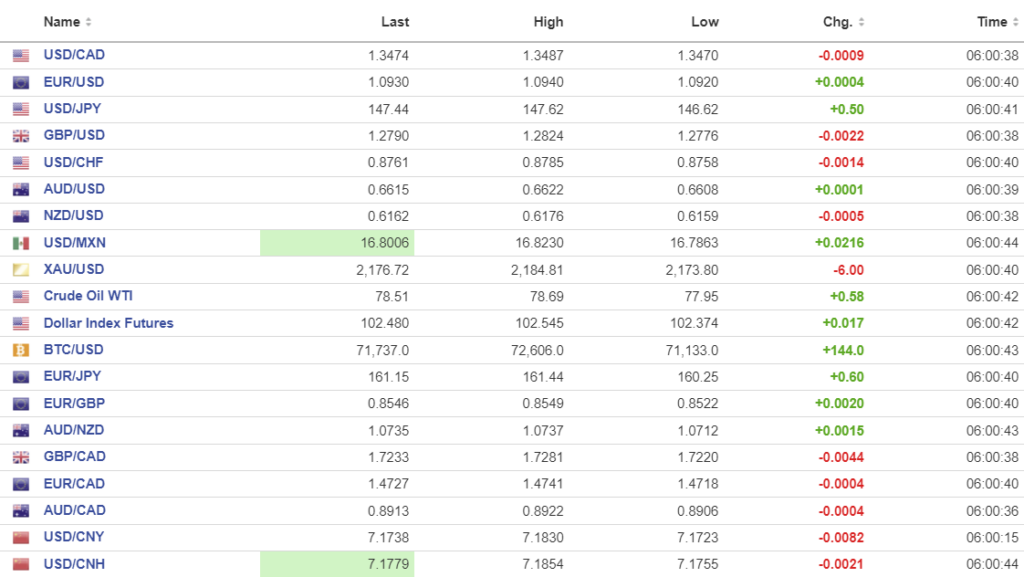

USDCAD Snapshot: open 1.3472-76, overnight range 1.3470-1.3513, close 1.3484

USDCAD opened right where it did yesterday and blew through the top in the wake of the hotter-than-expected US inflation data, rising from 1.3474 to 1.3513. The gains were erased just as quickly.

The results do not change the outlook for next week’s FOMC meeting, which is for no change in monetary policy.

Canada’s post-Covid economic rebound has greatly lagged that of the US due to many reasons, including draconian lockdown measures which hampered the recovery. In addition, the current government’s anti-business, anti-fossil fuel policies have driven foreign investment to Mexico, which became America’s largest trading partner in 2023, a title Canada owned since forever.

WTI oil chopped in a $77.95-$78.69 range, with prices supported by news that Russia’s seaborne crude shipments were at their highest level this year, worth $1.86 billion to Putin’s war machine. It is also a reason why OPEC production cuts are not having the desired effect.

The Canadian data calendar is empty.

USDCAD Technicals

The USDCAD technicals are neutral inside a 1.3440-1.3520 range. A break above 1.3520 targets 1.3560, then 1.360, while a move below 1.3440 targets 1.3410.

USDCAD is in a gradual uptrend channel that began at the beginning of the year and has guided prices higher, albeit somewhat erratically, in a 1.3410-1.3620 range as of today. When prices are below 1.3520, the floor is vulnerable, and when above 1.3520, the ceiling is in play.

For today, USDCAD support is at 1.3440 and 1.3410. Resistance is at 1.3505 and 1.3530. Today’s range is 1.3460-1.3530.

Chart: USDCAD daily

Source: Daily FX

G-10 FX

The US dollar rallied then retreated just as quickly following the hotter-than-expected US inflation data. US inflation rose 3.2% y/y in February (forecast 3.1%) and Core inflation rose 3.8% (forecast 3.7% y/y).

The data is inconclusive. Core CPI rose more than expected but it was below January’s 3.9% increase. Traders have already shifted their focus to Thursday’s US Retail Sales report.

Asian equity markets were indecisive. The Nikkei 225 index ticked slightly lower, while Australia’s ASX 200 index inched higher. European bourses are in the green, led by the German Dax gaining 0.32%. SP500 futures are up 0.12%, while the US 10-year Treasury yield is little changed at 4.09%.

EURUSD broke out of its 1.0920-40 range after the CPI data and dropped to 1.0903 before rebounding to 1.0943. German inflation data was as expected.

GBPUSD traded in a 1.2776-1.2824 range overnight then dropped and popped post-CPI, touching 1.2755 before bouncing to 1.2803. Earlier, data showing that UK wage growth slowed weighed on prices as it is a key metric for the BoE (actual Average earnings 5.6% 3ms, 5.8% previously). UBS Economists have revised their forecast for the first BoE rate cut to August from May.

USDJPY traded in a 146.62-147.62 range overnight, rallied to 148.15 post-CPI then dropped to 147.34. BoJ Governor Kazuo Ueda put a damper on anticipation of a March rate hike when he pointed out that although the economy was improving there were weak spots.

AUDUSD chopped in a 0.6608-0.6639 range with the top occurring after today’s US data. Prices saw additional support in the early going when the Australia Business Confidence rose more than expected (actual 10 vs previous 7).

NZDUSD traded in a 0.6137-0.6184 range. Electronic Card Retail Sales were -1.8% m/m in February, a sharp drop from the 2% rise in January. ASB economists suggest the results reveal a weak underlying retail position, but it won’t be enough for the RBNZ to cut rates, yet.

USDMXN traded quietly in a 16.7733-16.8558 range. Mexico Industrial output rose 2.9% y/y compared to 0% in December. The peso is also benefiting from increased investment demand as companies move from globalization to regionalization.

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.0963 vs exp. 7.1885 (prev. 7.0969.

Shanghai Shenzhen CSI 300 rose 0.23% to 3597.49.

Chart: USDCNY and USDCNH daily

Source: Investing.com