Photo: Bing AI

October 5, 2023

- Challenger Job cuts and weekly jobless claims highlight resilient Labour market.

- Yield curve inversion/recession talk resurfaces.

- Canadian dollar underperforms as US dollar corrects.

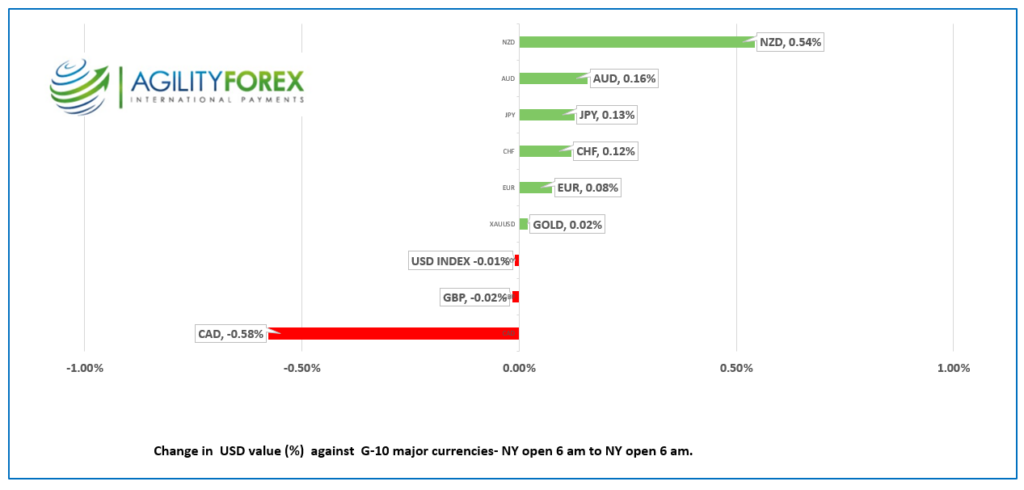

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open: 1.3775-79, overnight range: 1.3711-1.3786, close 1.3745

USDCAD did not get any lasting benefit from widespread US dollar selling seen yesterday and overnight. In fact, it is the only currency pair that strengthened compared to yesterday’s NY open. Part of the USDCAD strength stems from Canada’s close ties to America. If the US falls into a recession, can Canada be far behind? And which of the two countries is best situated to weather the storm?

USDCAD may have caught a bid after WTI oil prices went into free-fall this week, dropping from $91.41/barrel on Monday to $82.36/b today, for a loss of nearly 10%. The Energy Information Agency (EIA) reported a substantial increase in gasoline inventories and that news combined with rising recession fears suggested oil bulls, hoping for an increase in global demand, may have gotten ahead of themselves.

Canada’s $0.44 billion July trade deficit turned to a $0.72 billion trade surplus in August.

USDCAD Technicals

The intraday USDCAD technicals are in an uptrend while above 1.3710, a level which is guarding the 1.3690 support area, and looking for a move above 1.3790 to extend gains to 1.3860, then 1.3977. a level seen one year ago. A move below 1.3690 targets support in the 1.3640-60 area.

For today, USDCAD support is at 1.3710 and 1.3690. Resistance is at 1.3790 and 1.3860. Todays Range 1.3730-1.3830.

Chart: USDCAD 4 hour

Source: Investing.com

G-10 FX recap

The US dollar retreated yesterday and overnight but it still remains within its recent ranges. Yesterday’s ADP data, which was significantly weaker than expected, combined with mixed readings from the ISM services report, added selling pressure to the greenback. This came after the 10-year Treasury yields had already fallen sharply from a peak of 4.884% in Asia on Wednesday.

The drop in the US 10-year yield, which closed at 4.735% on Wednesday, triggered a Wall Street rally, leading the S&P 500 to close with a 0.81% gain. This positive sentiment extended to Asia, with Japan’s Nikkei 225 and Australia’s ASX 200 indices closing up by 1.80% and 0.51% respectively.

Following this mornings US data, European bourses turned from mixed to positive led by a 0.57% rise in the UK FTSE 100 index. S&P 500 futures recovered overnight losses and are up 0.32%. The US 10-year yield has inched higher, rising from its overnight bottom of 4.71% to 4.76% after strong Challenger Job cuts and weekly jobless claims data.

Challenger wrote “U.S.-based employers announced 47,457 cuts in September, down 37% from the 75,151 cuts announced in August.” However, the report did note that the September results were the eighth time that cuts were higher than the corresponding month last year.

The weekly jobless claims report showed claims rising a mere 2,000 which underscores the resiliency of the US employment market.

Yield curve inversion and its record for predicting a recession is gaining attention again, primarily because markets are anxious, ahead of US nonfarm payrolls report. (forecast 170,000).

EURUSD bounced between 1.0501 and 1.0530 and is back at its session low in NY. Divergent ECB and Fed monetary policies suggest gains are capped at 1.0550. German trade data disappointed, with exports falling 1.2% m/m in August, and July’s numbers being revised lower.

GBPUSD traded in a 1.2116-1.2164 range, consolidating Wednesday’s losses. Gains were limited due to the weak Construction PMI index, which plummeted to 45 from 50.8 in August. S&P Global mentioned that this was “the steepest decline in construction output since May 2020.”

USDJPY traded negatively in a 148.27-149.13, impacted by lower US Treasury yields and apprehensions regarding further BoJ FX intervention. However, prices have since climbed to the top of the band.

AUDUSD is trading in the middle of the overnight0.6318-0.6378 range, primarily due to US dollar selling pressures post the Wall Street rally and the decline in Treasury yields.

There are plenty of Fed speakers on tap today including, Barkin, Daly, and Mester.

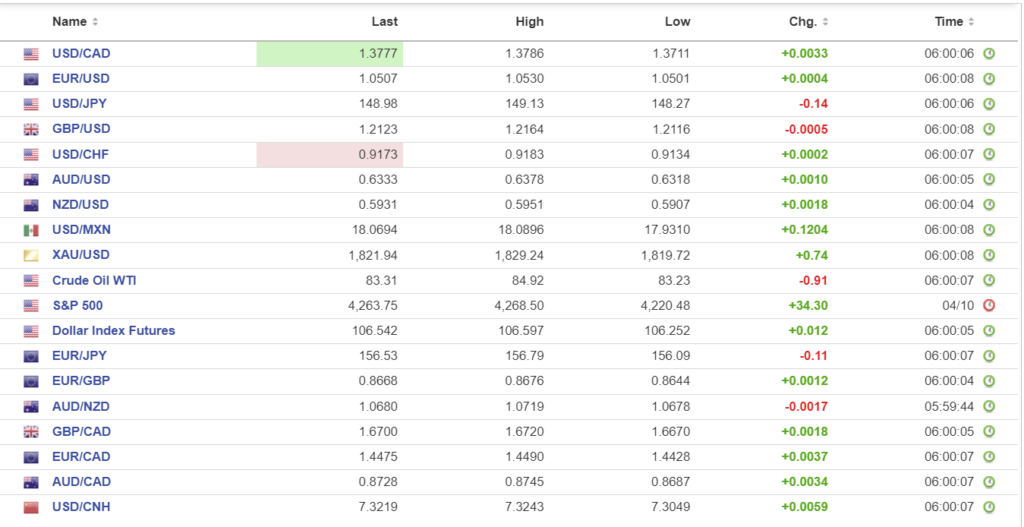

FX high, low, open

Source: Investing.com

China Snapshot

Chinese markets are closed for Golden Week holidays.

Bank of China Fix: closed. previous 7.1798.

Shanghai Shenzhen CSI 300 closed for Golden Week.

Citigroup raised China growth forecast for 2023 to 5.0% from 4.7%. The economists are suggesting that the economic downturn has reached a cyclical bottom.

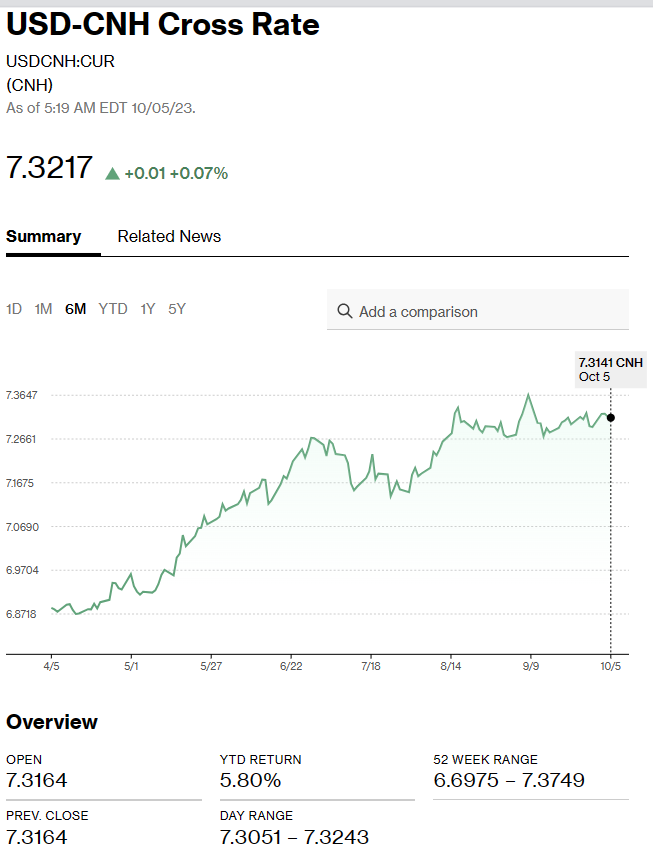

Chart: USDCNH (offshore)

Source: Bloomberg