September 26, 2024

- China brings Fiscal Stimulus to the table

- US data largely ignored.

- US dollar opens little changed but MXN underperforms

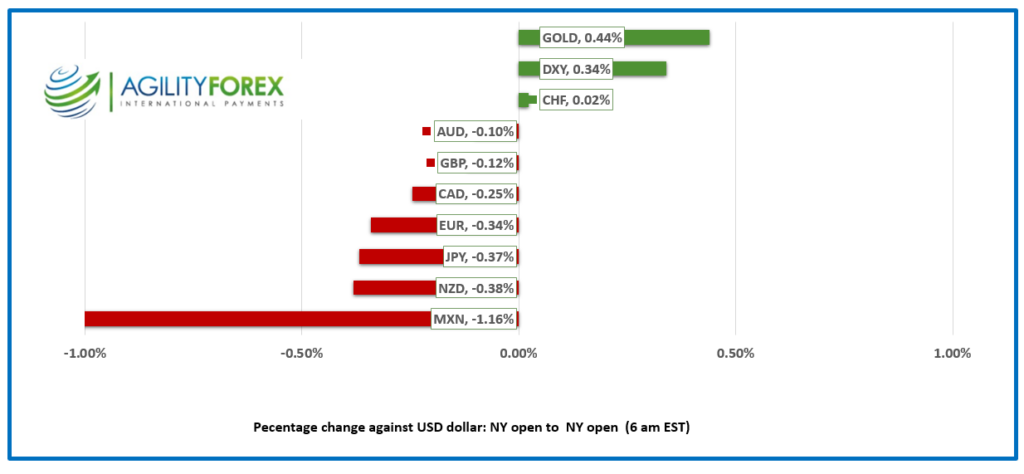

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3470, overnight range 1.3460-1.3487, previous close 1.3484.

USDCAD dropped yesterday but the selling pressure was not sustained, and prices rebounded to the 1.3480 resistance area. The failure to move about that levels raises the odds for another downside probe. However, further losses below the 1.3420 area may be tough to come by because of increased odds that the BoC could cut rates by 50 bps on October 23.

WTI oil prices have retreated from Tuesday’s peak of 72.39 and are sitting 67.79 in NY, a 6.35% drop. The move occurred despite a 4.47 million barrel decline in US crude inventories last week. That’s’ because Saudi Arabia is reportedly planning to boost production in December. In addition, Libyan factions have reached a deal which will lead to the resumption of crude production.

USDCAD technicals

The intraday USDCAD technicals are bearish below 1.3480,a nd looking for another test of 1.3420 to extend losses to 1.3380. A break above 1.3480 targets 1.3550.

Bollinger band studies show that USDCAD is just above the third standard deviation level of 1.3373 which indicates extreme oversold which suggests prices could rebound to 1.3550.

For today, USDCAD support is at 1.3430 and 1.3410. Resistance is at 1.3480 and 1.3510.

Today’s Range 1.3430-1.3510

Chart: USDCAD daily

Source: Oanda.

Ceasefire Plans Shot Down in Flames

The global risk sentiment tone was improving following reports that Israel and Hezbollah were close to agreeing to a ceasefire, which was being aggressively pushed by the US and France. That idea was shot down in flames by Israel’s Foreign Minister. He tweeted (X’d?) “There will be no ceasefire in the north. We will continue to fight against the Hezbollah terrorist organization with all our strength until victory and the safe return of the residents of the north to their homes.”

US Data Barely Causes a Ripple

Initial Jobless Claims rise 218,000 (forecast 225,000) while last week’s number was revised up by 3,000 to 222,000. August Durable Goods rose 9.9% with ex-transportation rising 0.5%. The data suggest that the Fed will achieve a soft landing. Markets will hear more about that today as Fed Chair Powell headlines a parade of six other Fed officials making speeches today.

The Big Apple is Rotten to the Core

The Mayor of New York, Eric Adams, may soon be adding prison pinstripes to his wardrobe. Federal investigators have indicted the Mayor, with the details of the indictment to be released today. About 20 other city officials and campaign workers or friends have been indicted, charged, or questioned in a sweeping corruption investigation that includes receiving illegal foreign donations.

China Cracks the Piggy Bank

China’s President Xi Jinping and his Politburo are planning to issue sovereign debt amounting to 2 trillion yuan (US $284 billion) in an effort to put an end to the economic malaise infecting the country. Today’s news followed the PBoC’s monetary policy announcement and helped to give Asian equity indexes a boost. Hong Kong’s Hang Seng Index soared 4.13%, Japan’s Topix rallied 2.79%, and Australia’s ASX 200 gained 0.96%. European bourses followed suit, led by a 1.41% rise in the French CAC 40 Index, while S&P 500 futures are up 0.84%.

EURUSD

EURUSD is choppy in a 1.1126-1.1158 band, with prices at the top of that range in early NY. Reuters is reporting that the October 17 ECB meeting is up in the air. Doves on the council want a 25 bp rate cut due to a series of soft economic data, including the weak German Ifo Surveys, while the hawks want to wait until the December meeting. The Swiss National Bank delivered a “dovish” 25 bp rate cut today, which took the benchmark rate down to 1.0% from 1.25%. The central bank said, “downside risks to inflation are currently higher than the upside risks,” suggesting more rate cuts were likely.

GBPUSD

GBPUSD drifted higher in a 1.3312-1.3369 range. The gains were due to improved global risk sentiment after the Chinese government announced fiscal stimulus plans. GBPUSD remains underpinned by contrasting Fed and Bank of England interest rate outlooks.

USDJPY

USDJPY rose from 144.44-145.20 in Europe, then dropped to 144.59 into the New York open. Prices retreated with the US 10-year Treasury yield ticking lower to 3.77% from 3.79%. Traders were also cautious ahead of today’s rash of Fed speakers and the US economic data dump.

AUDUSD and NZDUSD

AUDUSD is trying to recoup yesterday’s losses, rising from a low of 0.6819 in Asia to 0.6874 in early NY. The gains are due to the latest fiscal stimulus news from China and hopes that today’s US data dump reinforces the outlook for another 50 bp rate cut.

NZDUSD followed Aussie moves and firmed in a 0.6252-0.6294 range.

USDMXN

USDMXN rallied yesterday and then consolidated the gains in a 19.5683-19.6620 range ahead of the Banxico monetary policy meeting today. A 25 bp rate cut to 10.5% is priced in, although some analysts are suggesting a 50 bp cut is on the table. Nevertheless, selling pressures are hampered by ongoing concerns about pending judicial reforms.

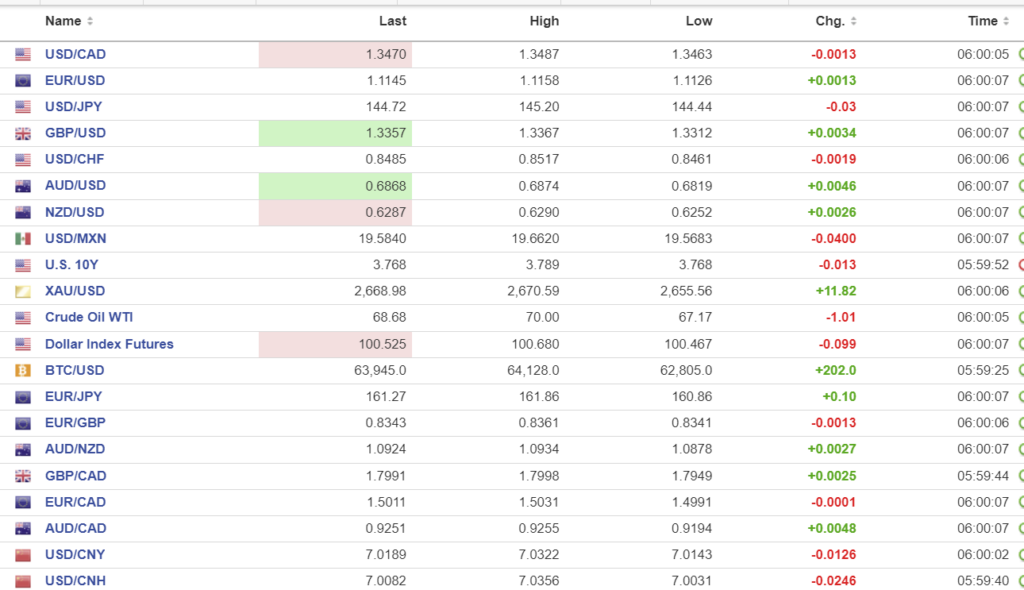

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.0354 (prev. 7.0202)

Shanghai Shenzhen CS! 300 rose 4.23% to 3545.32

China’s President Xi Jinping and his Politburo delivered a jumbo round of fiscal stimulus overnight, on the heels of yesterday’s PBoC monetary policy stimulus. The Politburo plans include injecting $142 billion of capital into its biggest state banks, along with a pledge to support fiscal spending and to make the real estate market “stop declining.” The Politburo also called for the “foreceful” implementation of rate cuts. The news sent equity markets soaring.

China plans to issue $285 billion in special sovereign bonds to fund the stimulus initiatives.

Chart: USDCNY and USDCNH

Source: Investing.com