Photo: BingAI

July 13, 2023

- Positive risk sentiment bolstered by peak Fed rates talk.

- Canadian dollar rallies but is the G-10 currency laggard.

- USD dives after CPI-extends losses overnight.

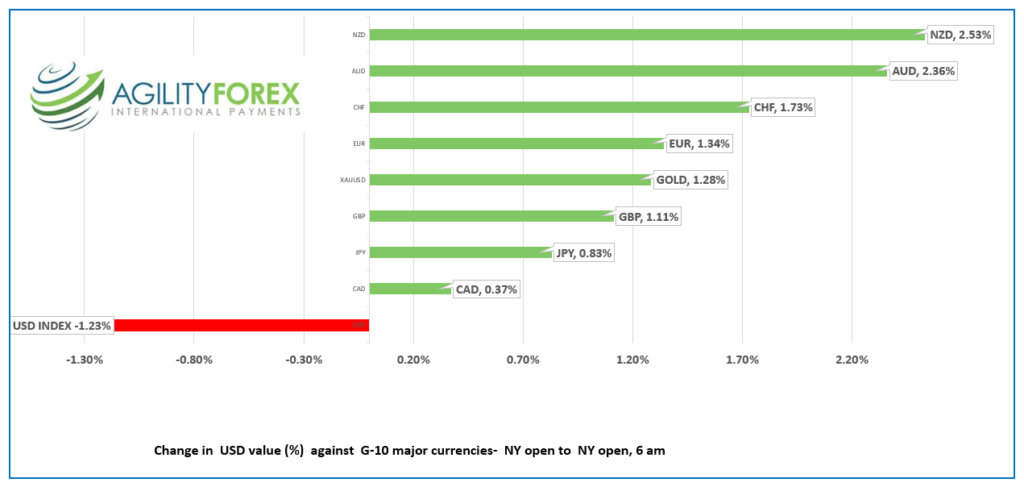

FX at a glance:

Source: IFXA Ltd

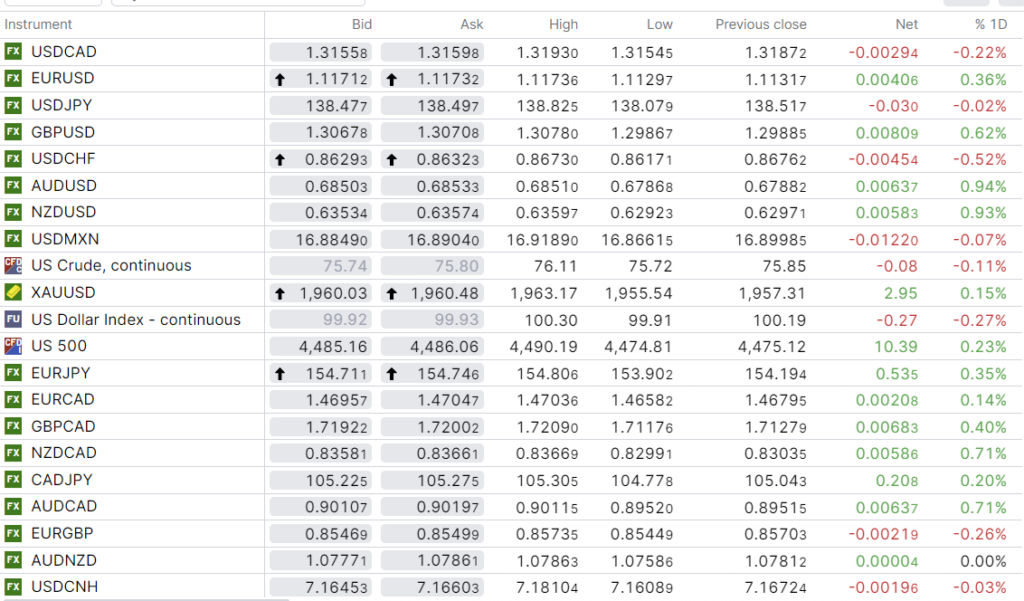

USDCAD Snapshot: open 1.3156-60, overnight range 1.3152-1.3193, close 1.3187

USDCAD dropped after the US CPI data but found support in the 1.3150 area. It was unable to move below 1.3150 even after the Bank of Canada hiked rates by 25 bps and delivered a somewhat hawkish outlook.

The response is to be expected as BoC Governor Tiff Macklem has a poor track record for providing consistent, accurate forward guidance. Traders have been scorched following his advice many times in the past, so it makes sense that the latest monetary policy statement and quarterly Monetary Policy Report barely caused a ripple in FX markets.

Higher oil prices weighed on USDCAD. WTI rose to $76.11/b from $75.72/b overnight, but gains were hampered by a downbeat International Energy Agency (IEA) forecast, suggesting that although oil demand will hit a record high, it will be lower than previously expected due to a deepening manufacturing slump in Europe.

USDCAD is trading with a negative bias due to broad US dollar weakness, but its moves are expected to lag behind those of the other G-10 currencies. A $900 million 1.3200 option strike maturity today may help contain price action until 10:00 am EDT.

USDCAD Technical Outlook

The intraday USDCAD technicals are bearish below 1.3190, looking for a break below 1.3150 to target 1.3110. A move above 1.3190 will test 1.3220, the downtrend line from July 7 but if it holds, it suggests another drop to 1.3150 is likely.

Longer term, the March downtrend is intact below 1.3470 and is guarded by the June downtrend line at 1.3360 . The breach of the 1.3182 level (50% Fibonacci retracement of the April-October 2022 range)suggests a drop to the 1.2990-1.3000 (61.8% Fibonacci)

For today, USDCAD support is at 1.3150 and 1.3090. Resistance is at 1.3190 and 1.3230.

Today’s range 1.3100-1.3190

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap

The allure of myths and legends has captured the hearts of glory-seekers for centuries. Men have been searching for the Holy Grail, the Fountain of Youth, and the Philosopher’s Stone with no success. The most recent quest was the search for a US economic soft landing.

Eureka! The soft landing has been found, at least that’s what traders believe after yesterday’s cooler-than-expected US inflation report.

US CPI cooled more than expected in June (actual Core-CPI 4.8% y/y vs 5.3% in June). In terms of the peak fed funds rate, traders no longer just see a light at the end of the tunnel but instead are looking at the vivid luminosity of the Las Vegas Strip at midnight. One and done!

Today’s US data results supported the view that Fed may soon be done. June PPI only rose 0.1% compared to the forecast for a 0.2% gain, while weekly jobless claims fell 12,000 to 237,000.

The US dollar got hammered following the CPI release. The US dollar index smashed through the 2023 low of 100.50, and with a decisive breach of 99.38, it will target the pandemic low of 98.35. The S&P 500 index is trading at a level last seen in April 2022 and has gained 16.5% YTD.

The US 10-year Treasury yield plunged from 4.09% on Monday to 3.818% today, which fueled the positive risk sentiment. The falling greenback also gave gold and oil prices a lift.

Asian equity indexes followed Wall Street’s lead and rallied. Australia’s ASX 200 gained 1.54%, followed by Japan’s Nikkei 225 index, which rose 1.49%. Hong Kong’s Hang Seng index was the frontrunner, gaining 2.60%.

European bourses opened in positive territory, and the 0.56% rise in the French CAC 40 index leads the pack.

EURUSD soared yesterday then extended the gains in a 1.1130-1.1189 overnight. The ECB minutes did not change the narrative. The central bank will raise rates in two weeks. However, some analysts think the tightening cycle will end in September which is supported by ECB Governing Council member Ignazio Visco. He suggested that rates would peak by the end of 2023. Eurozone Industrial production data (actual -2.2% y/y in May vs forecast -1.2%) was ignored.

GBPUSD rose from 1.2987 to 1.3078 as traders embraced the idea that the Fed may be done raising rates sooner than expected. Prices were also supported after UK GDP fell less than anticipated (actual 0.1% m/m vs forecast -0.3%).

USDJPY extended losses and dropped to 138.08 from 138.95 thanks to sharply lower US Treasury yields and the belief that the Bank of Japan may begin tightening as Fed rates peak.

AUDUSD climbed from 0.6787 to 0.6869 in NY despite weaker than expected Chinese trade data due to widespread US dollar selling.

NZDUSD followed AUDUSD higher, rising from 0.6292 to 0.6374.

FX open, high, low, previous close as of 6:00 am ET

Source: Bloomberg

China Snapshot

Bank of China Fix: 7.1527 (expected 7.1623) Previous 7.1765

Shanghai Shenzhen CSI 300 rose 1.43% to 3898.42.

Reuters Poll: PboC expected to cut RRR rates by 0.25 bps in Q3.

China’s Trade Surplus rises to $70.62 billion (forecast $74.8b, vs May $65.8 b).

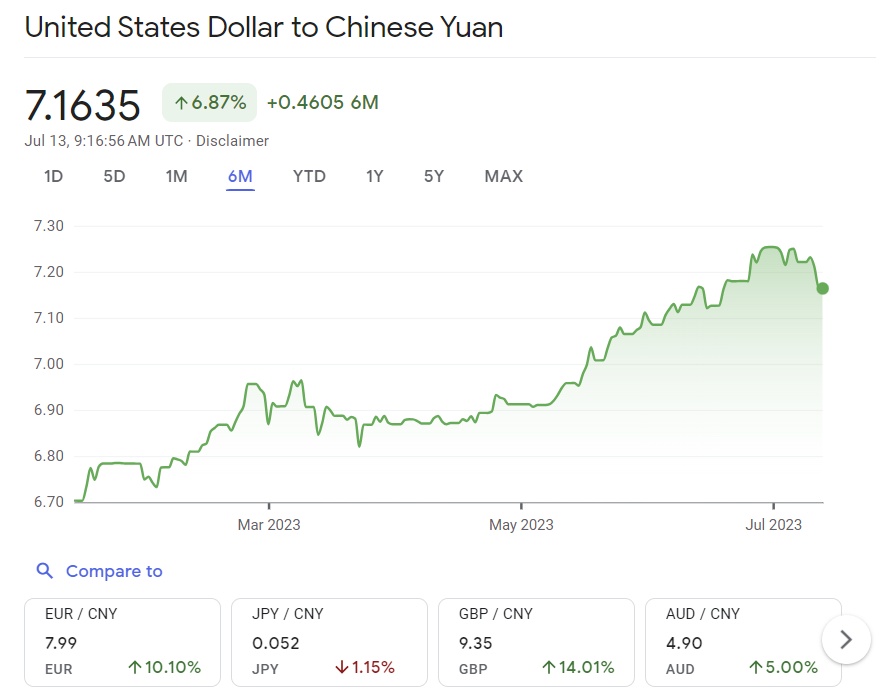

Chart: USDCNY 6 month

Source: Bloomberg