June 5, 2019

USDCAD Open (6:00 am EDT) 1.3367-70 Overnight Range 1.3367-1.3396

Fed Chair Jerome Powell lit a fire under Wall Street traders. He said the Fed is closely monitoring the implications around recent developments involving trade negotiations and their implications for the US economic outlook. He added, “as always, we will act as appropriate to sustain the expansion, with a strong labour market and inflation near our symmetric 2 percent objective.”

To market analysts, that sentence is a clear signal that US rates are going lower. Wall Street soared, and the US dollar fell, albeit not aggressively.

That theme continued overnight as Asia equity indices rallied. The Nikkei 225, gained 1.80%. European bourses climbed as well, but with a lot less enthusiasm. S&P 500 futures point to a positive open this morning as well.

In Asia, broad US dollar weakness fueled gains in AUDUSD and NZDUSD. Kiwi got added support after the RBNZ Assistant Governor Christian Hawkes said the RBNZ central view is for interest rates to remain broadly around current levels for the foreseeable future. AUDUSD underperformed against Kiwi after Australia Q1 GDP grew less than expected. (Actual 0.4% vs forecast 0.5%) Gains were limited by softer than forecast Caixin China Services PMI (Actual 52.7 vs forecast 54.3)

USDJPY chopped about until Europe opened and prices rallied from 107.99 to 108.33 in New York trading. US rate cut speculation and a small bounce in Treasury yields underpinned prices.

EURUSD is trading at its overnight peak of 1.1287. Eurozone economic data provided a mixed bag of results. May Services PMI was slightly better than predicted, Retail Sales were as expected, and PPI was worse than expected. Traders ignored the data and bought EURUSD. However, gains may be capped. The IMF is supposedly warning that Italy’s debt poses a major risk to the eurozone and that it is a violation of EU fiscal rules.

GBPUSD climbed on the back of the soft dollar and better than expected Markit Services PMI (Actual 51.0 vs forecast 50.6). Nevertheless, the risk that Boris Johnson, a hard Brexit proponent, could be the next Prime Minister, should limit gains.

WTI has rebounded from the Asia low. The weekly API crude stocks report showed US crude inventories rose 3.545 million barrels last week. WTI dropped from $53.60/barrel to $52.80/b. The improved risk tone in markets lifted WTI to $53.20/b in early New York trading.

USDCAD consolidated yesterday’s losses in a 1.3366-1.3396 range. Prices are flirting with uptrend line support in the 1.3370 area. Further USDCAD losses may not be sustained due to rising speculation that the Bank of Canada may be forced to cut rates. China is continuing with its policy of disruption in Canada trade. They’ve cancelled Canola imports, suspended pork permits, and yesterday they said they would increase “inspections “of all Canadian meat imports.

Today’s US data includes ADP Employment and ISM Non-manufacturing PMI. The Canadian calendar is empty.

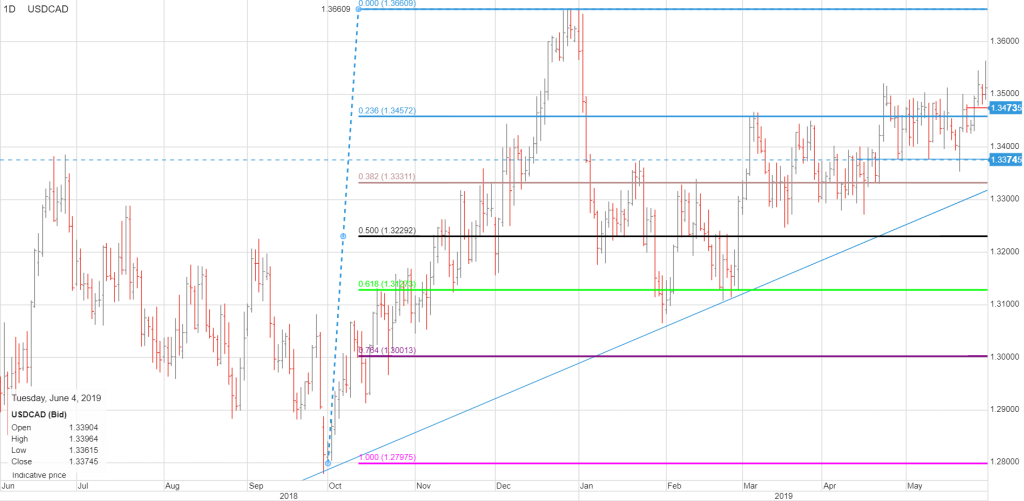

USDCAD Technicals

The intraday USDCAD technicals are bearish. The break of support at 1.3430 and 1.3405 target further losses to 1.3330 if support at 1.3370 can be overcome. That level has uptrend and double bottom support. Longer term, a break below 1.3330 suggests further losses to 1.3000, the 76.4% Fibonacci level of the October 2019-January 2019 range. A move above 1.3460 would put 1.3550 in focus.. For today, USDCAD support is at 1.3370 and 1.3330. Resistance is at 1.3410 and 1.3430. Today’s Range 1.3370 1.3410

Chart: USDCAD daily