Photo: BingAI

July 10, 2023

- BoC expected to hike rates Wednesday.

- Wednesday’s US CPI in focus

- USD opens weaker in fall-out from disappointing NFP.

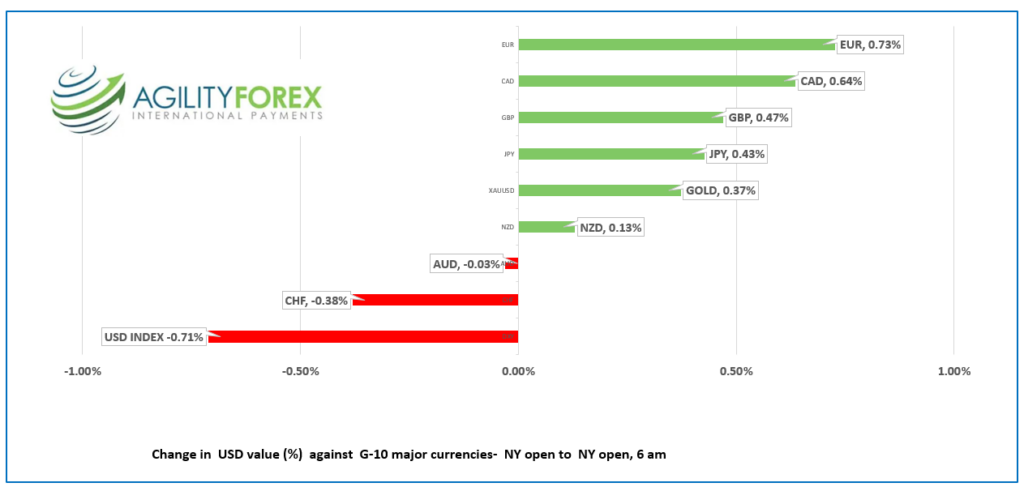

FX at a glance:

Source: IFXA Ltd

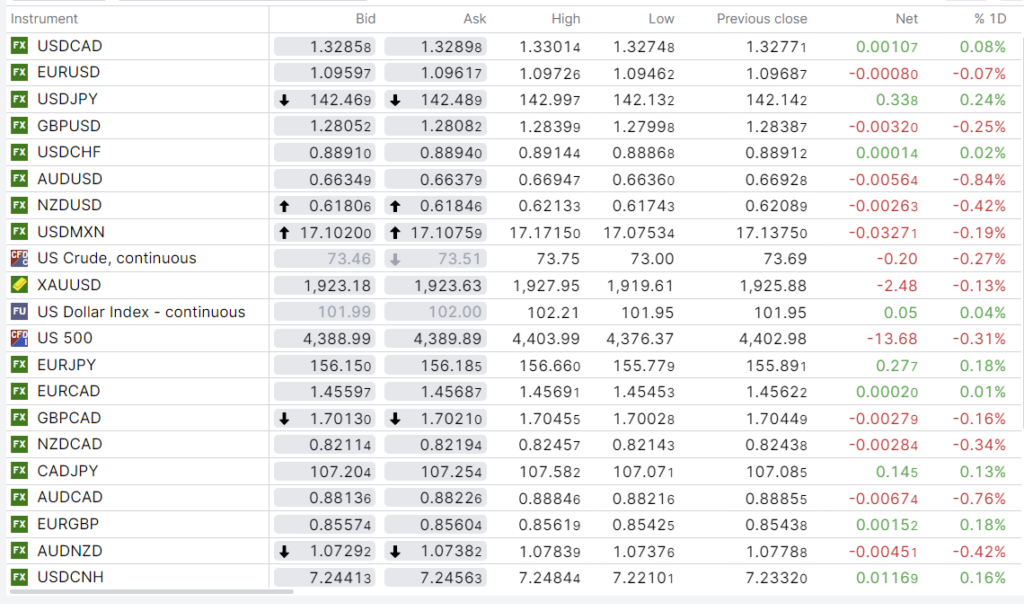

USDCAD Snapshot: open 1.3286-90, overnight range 1.3274-1.3301, close 1.3277

USDCAD is consolidating its losses following Friday’s stellar Canadian employment data and a disappointing US nonfarm payrolls report. Friday, USDCAD plunged from 1.3385 in Europe to a low of 1.3265 by lunch, then spent the rest of the day and overnight drifting higher.

USDCAD traders are looking ahead to Wednesday’s Bank of Canada (BoC) monetary policy meeting when a 25 bps rate hike to 5.0% is almost guaranteed by the hotter than expected jobs data. The BoC will release the summer Monetary Policy Report, which lately is a package of pretty charts containing inaccurate forecasts.

The BoC meeting is just one catalyst for USDCAD direction. The other is the release of US CPI for June which is expected to drop to 3.1% y/y from 4.0%. However, the more critical Core-CPI (ex food and energy) is expected at 5.0% which is too high for the Fed to ignore.

WTI oil prices rallied post-NFP, due to widespread US dollar weakness, which lifted prices from $$71.50/b to $73.75/b overnight. The latest production cuts from Saudi Arabia and Russia are also underpinning prices.

There are no top tier Canadian economic reports this week.

USDCAD Technical Outlook

The USDCAD intraday technicals are bullish above 1.3260 and looking for a move above 1.3320 to extend gains to 1.3380. A break below 1.3260 targets 1.3180, then 1.3110, which has contained downside moves since September 2022.

Longer term, USDCAD is bullish above the 1.3000-1.3020 area and only a decisive breech below that level would negate the uptrend.

For today, USDCAD support is at 1.3260 and 1.3220. Resistance is at 1.3320 and 1.3360.

Today’s range 1.3260-1.3330.

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap

The lower than expected US nonfarm payrolls data (actual 209,000, forecast 225,000) suggested that the while the US economy may be slowing and even avoid a recession, the decline was not enough to deter the FOMC from raising rates on July 26. Markets will hear a lot more about the Fed’s plans for rates this week. Today, San Francisco Fed President Mary Daly, Cleveland Fed President Loretta Mester, and Raphael Bostic of Atlanta will regale audiences with their insight.

There was plenty of geopolitical news over the weekend including Treasury Secretary Yellen’s visit to China, discussions around the upcoming NATO meeting this week, and the US sending cluster bombs to Ukraine. However, the news did not translate into FX activity.

EURUSD is drifting in a 1.0946-1.0973 range as demand following the disappointing US employment data fades and traders look ahead to US CPI on Wednesday. Traders are also cautious because of the many Fed policymakers speaking today and this week.

GBPUSD is at the bottom of its overnight 1.2774-1.2840 range due to a mix of profit-taking and caution ahead of Tuesday’s UK employment data and Thursday’s GDP report.

USDJPY is in the middle of its 142.13-143.00 range. Prices are supported by the US 10-year Treasury yield sitting at 4.06% but traders remain wary about the Bank of Japan intervening to drive USDJPY lower.

AUDUSD traded negatively in a 0.6634-0.6694 range due to divergent Fed and RBA interest rate outlooks.

NZDUSD traded in a 0.6634-0.6694 range with traders looking ahead to the RBNZ meeting on Wednesday. The market expects the RBNZ to leave rates unchanged at 5.5%.

FX open, high, low, previous close as of 6:00 am ET

Source: Bloomberg

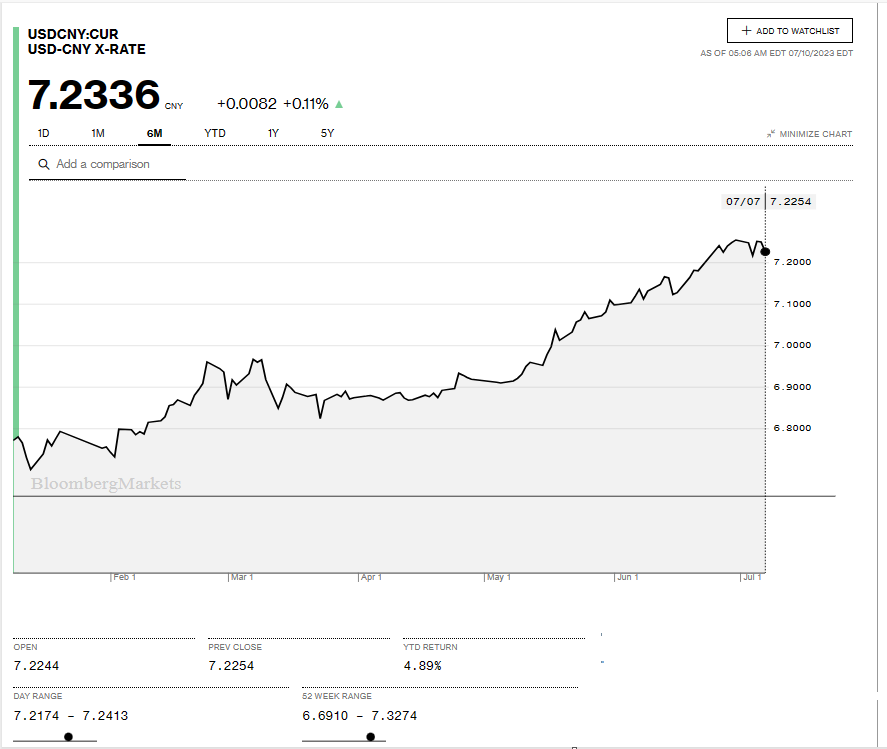

China Snapshot

Bank of China Fix: 7.1926 (expected 7.2132) Previous 7.2054

Shanghai Shenzhen CSI 300 rose 0.49% to 3844.33.

Chart: USDCNY 6 month

Source: Bloomberg