Image by DALL-E

November 17, 2023

- Falling crude prices weigh on Loonie.

- Fed officials appear to push back against talk of easing.

- US dollar consolidating this weeks losses-CAD underperforms.

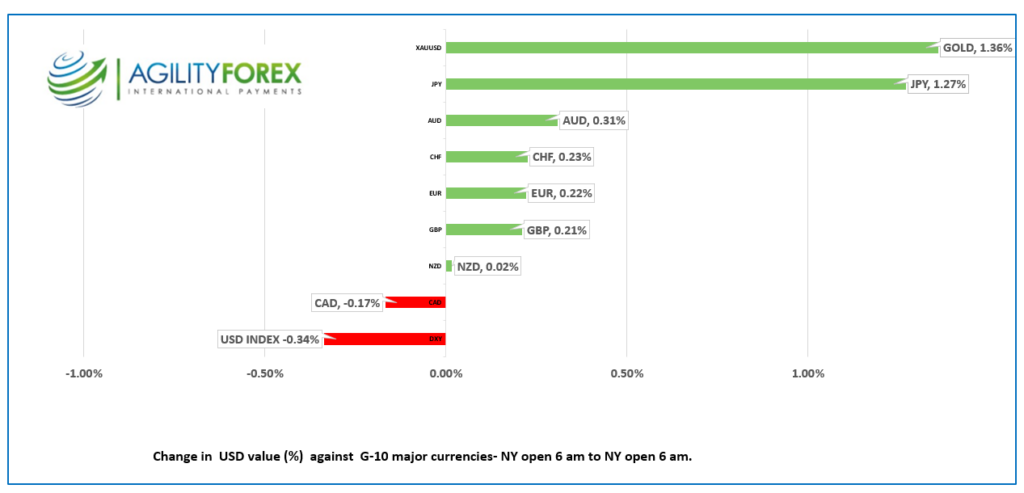

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open 1.3723-27, overnight range 1.3711-1.3772, close 1.3757

USDCAD resisted broad US dollar selling pressure overnight and is the best performing G-10 major currency today. That is not saying much as USDCAD is in a mild downtrend since last Friday’s peak. USDCAD gains are hampered by the slight improvement in the CAD/US 10-year yield spread but falling oil prices are limiting losses.

WTI oil added to this weeks losses and fell to $72.75/b overnight before bouncing back to $73.86 /b in NY. The downside drop is being fueled by rising supply with reports that Guyana and the North Sea shipments will increase next month. In addition, US crude inventories have also increased.

Canada Industrial Product Price index fell 1.0% (September 0.4%) and the Raw Material Price Index dropped 2.5% )September 3.9%)

USDCAD Technicals:

USDCAD continues to amble aimlessly in the 1.3550-1.3880 range which has contained price action since October. 10. The intraday downtrend below 1.3820 is targeting the uptrend from October 11 at 1.3640. A break either side is worth 100 bps.

Longer-term, there is no change from yesterday. The uptrend channel from the September is intact and suggesting a 1.3640-1.3980 range. A break below the bottom of the channel sets the stage for deeper losses to the 1.3350-1.3360 zone.

For today, USDCAD support at 1.3710 and 1.3660. Resistance at 1.3780 and 1.3820. Today’s expected range is 1.3710-1.3790.

Chart: USDCAD 4 hour

Source: Investing.com

G-10 FX recap

It’s almost a wrap. It’s the last day of trading for many American traders before they break for Thanksgiving week. China has Golden Week, encompassing about seven days of national holidays where everything that can be closed is. The USA does it differently. Businesses and government offices are only officially closed on one day, and this year it is Thursday, November 23, but many people book the entire week off.

Traders have worked themselves into a lather following the weaker-than-expected inflation report and slightly weaker Retail Sales data, convinced that the Fed will soon be cutting rates. The S&P 500 index has rallied 3.72% since last Friday, the 10-year yield has dropped from 4.69% on November 10 to 4.40% today, and gold prices climbed 2.8% to $1989.56 today.

Fed officials are suggesting caution. San Francisco Governor Lisa Cook said she believed a soft landing was possible but warned, “There is a risk that such continued momentum in demand could keep the economy and labor market tight and slow the pace of disinflation.” Cleveland Fed President Loretta Mester didn’t sound too eager to cut rates when she said, “It’s going to take some time to get inflation back down to 2%.”

Wall Street’s mixed close did not provide much guidance for Asian equity indexes. A falling yen lifted Japan’s Nikkei 225 index 0.48%, while the Australian ASX 200 dipped down 0.13%. Hong Kong’s Hang Seng index fell 2.12%. Chinese equity traders did not seem impressed with the outcome of the Jinping/Biden meeting and were confused as to why American business leaders attending a dinner gave the Chinese emperor a standing ovation. Did the American’s think the man was America’s Got Talent winner, magician Shin Lim? Both Lim and Jinping make things disappear, one does cards, the other does business executives.

European bourses are surging, led by a 0.91% rise in the UK FTSE, which is just slightly better than the 0.84% gain in the German DAX. S&P 500 futures point to a positive open on Wall Street.

EURUSD traded with a mixed bias in a 1.0825-1.0877 range. Traders are content to let developments elsewhere guide direction although it has a bit of a bid from bullish technicals above 1.0750 and lower US Treasury yields.

GBPUSD is chopping around in a 1.2374-1.2438 band. Sterling closed in NY at 1.2413 then dropped to the session low after sharply weaker-than-expected UK October Retail Sales data (actual -2.7% y/y vs forecast -1.5% and -1.0% in September). The decline was blamed on high interest rates and bad weather and increased concerns of a recession. Deputy Governor Dave Ramsden said that monetary policy needs to remain restrictive for some time, which is helping to support GBPUSD.. The intraday technicals are bearish while below 1.2450.

USDJPY dropped to 149.20 overnight after touching 151.47 yesterday due to tumbling US Treasury yields.

AUDUSD had a choppy session bouncing in a 0.6452-0.6512 range with price action mirroring US dollar sentiment.

US Building Permits rose 1.1% in October while Housing Starts were up 1.9%.

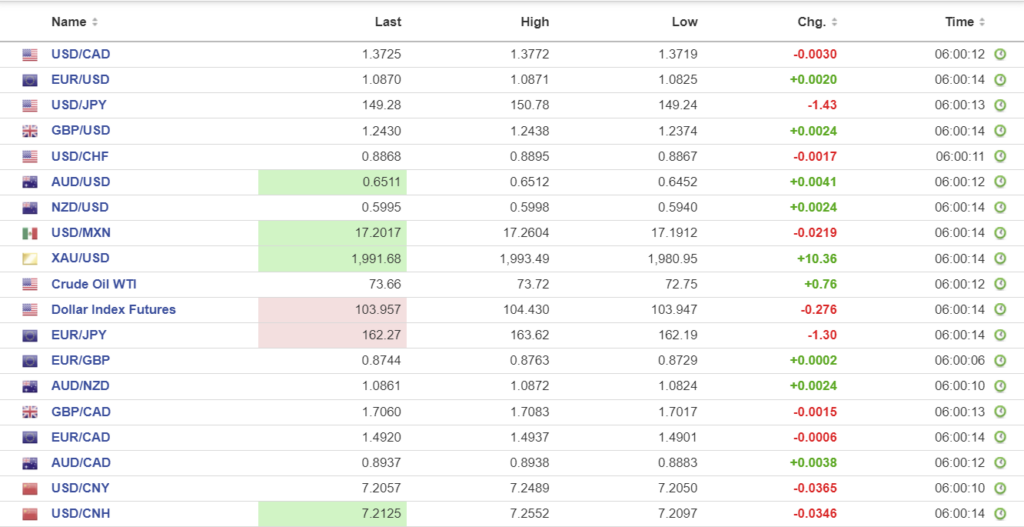

FX high, low, open

Source: Investing.com

China Snapshot

PBoC fix: today 7.1728, expected 7.2473, previous 7.1724.

Shanghai Shenzhen CSI 300 fell 0.17% to 3568.07.

Chart: USDCNY (onshore) vs USDCNH (offshore) 3 months

Source: Investing.com