July 17, 2019

USDCAD open (6:00 am EDT) 1.3054-57 Overnight Range: 1.3055-1.3092

Canada June inflation data was mildly disappointing, and it has underpinned USDCAD. June CPI fell 0.2% m/m, as expected while Core CPI was flat compared to the consensus forecast for a 0.1% rise. Year over year, Headline and Core CPI rose 2.0%. Statistics Canada blamed the drop on lower energy prices and noted that when energy prices are excluded, Core CPI rose 2.6%. Today’s data suggests that the Bank of Canada will be in no hurry to reduce interest rates.

May Manufacturing Shipments rose 1.6%, below the forecast for a 2.0% increase but well above April’s 0.4% decline. The increase was due to higher transportation sales.

USDCAD bounced between 1.3050-75 as the data was released and settled in at 1.3075.

The US dollar opened in New York on a mixed note but with little change from the close. FX prices went on a “walk-about” in Asia and Europe. Brexit, Trump, Iran, US interest rates, and oil concerns played a role in the price action.

In Asia, NZDUSD rallied on the back of the 2.7% rise in GlobalDairyTrade auction prices and opened in New York with a 0.39% gain compared to Tuesday’s close. AUDUSD underperformed. President Trump’s comments yesterday, suggesting that the trade talks have a long way to go, led to initial AUDUSD gains in Asia, disappearing. The currency pair opened unchanged in New York.

Traders shrugged off other remarks from Mr Trump saying he would end the tariff truce if the trade talks don’t progress. China responded by naming their reportedly hardline Commerce Minister, Zhong Shan to the negotiating team.

USDJPY rallied above 108.00 yesterday and spent the overnight session chopping about in a 108.12-31 band. Yesterday’s better than expected US data suggested the Fed may be more patient than expected with the pace of US rate cuts.

GBPUSD consolidated yesterday’s losses in a 1.2384-1.2418 band. Traders are concerned about the rising risks of a “no-deal” Brexit and an early election that decimates Labour and anoints Boris Johnson as Prime Minister. Today’s round of UK data was mixed and didn’t have a lasting impact on FX markets. June CPI was 0.0%, as expected but down from the 0.3% rise in May.

EURUSD traded in a narrow 1.1201-16 band and continues to be weighed down by the dovish ECB outlook. Higher than expected inflation data did not give the single currency any support. June Eurozone CPI rose 0.2% (forecast 0.1%) and 1.3% year over year. (forecast 1.2%)

Oil prices plunged yesterday following Trump’s comments about making progress in talks with Iran. Prices found a floor when Iran officials said its missile program was not negotiable. WTI oil dropped from $59.97/barrel to $57.15 yesterday before recovering to $59.99/b overnight. The API report of a 1.4 million barrel reduction in US crude inventories helped to support prices.

Today’s US Housing reports were lower than expected but markets are more focused on Wall Street price action as the quarterly earnings season kicks off in earnest

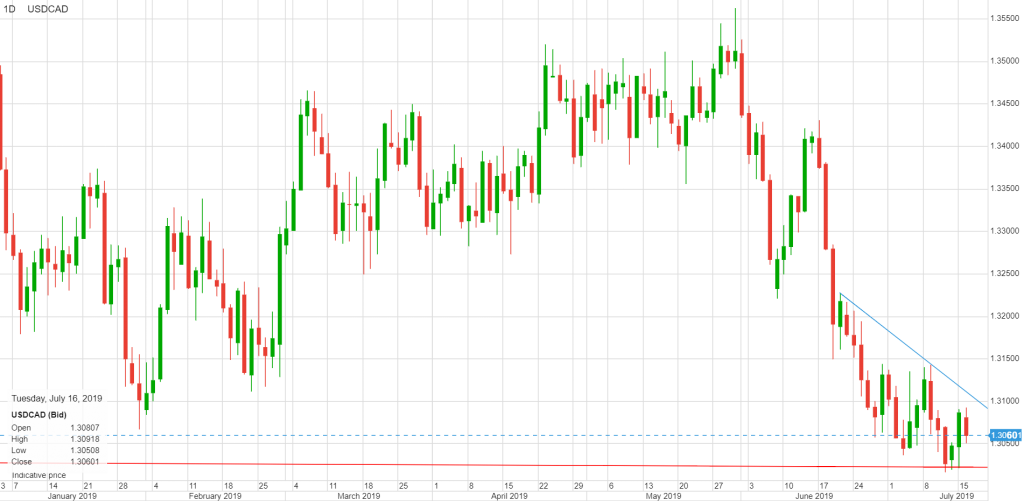

USDCAD Technical Outlook

The intraday USDCAD technicals are bearish while prices are below 1.3070 which guards the longer term downtrend line at 1.3120. A break above 1.3120 targets 1.3190. A move below 1.3020 targets 1.2990. Longer term USDCAD is consolidating losses in a 1.3000-1.3090 range while the downtrend from June 20 remains intact below 1.3120.. For today, USDCAD support is at 1.3020 and 1.2990. Resistance is at 1.3080 and 1.3120. Today’s Range 1.3020-1.3090

Chart: USDCAD daily