May 14, 2024

- Producer Prices rise more than expected.

- UK employment and German ZEW data barely cause a ripple.

- US dollar trades quietly and opens little changed from Monday.

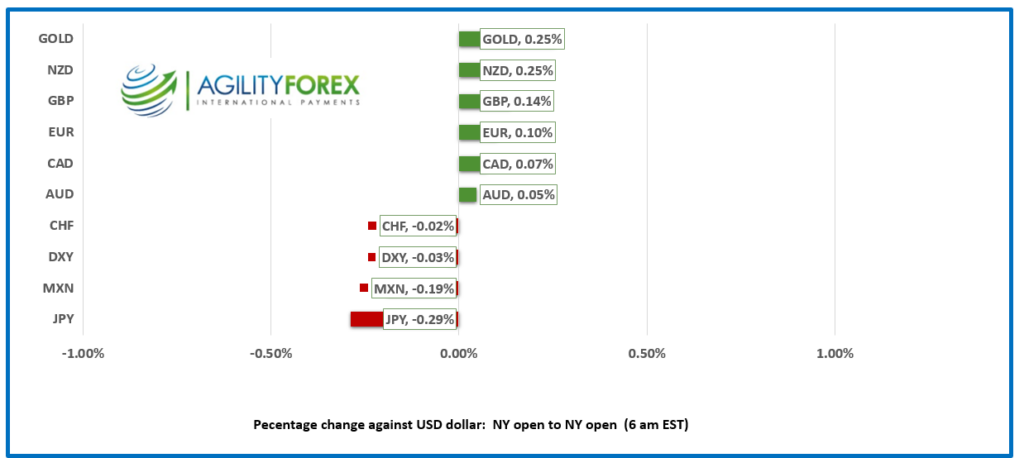

FX at a Glance

Source: IFXA/RP

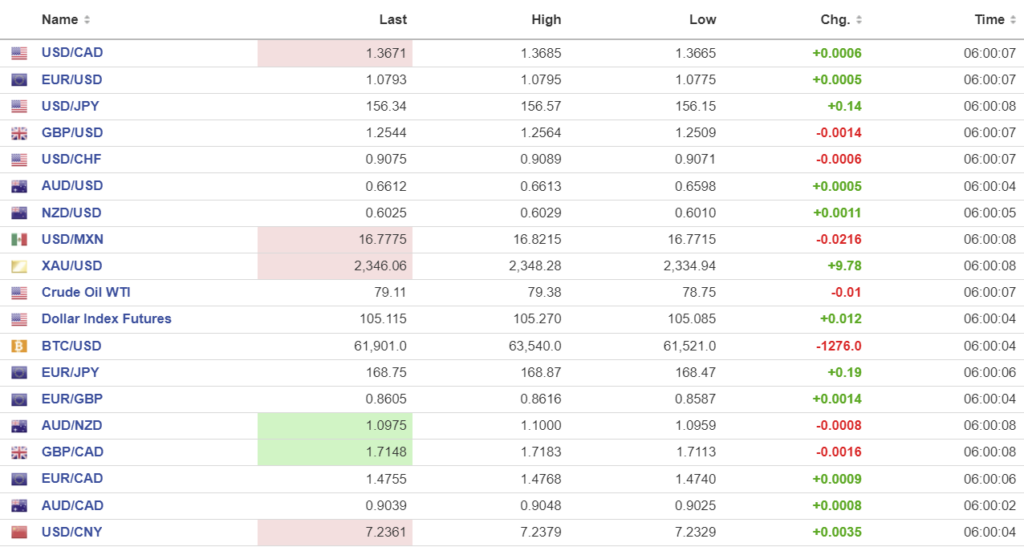

USDCAD Snapshot: open 1.3671, overnight range 1.3663-1.3685, close 1.3668

USDCAD is rather stagnant. Traders are content to await direction from US data while ignoring domestic economic reports. USDCAD barely acknowledge the narrowing of the 10-year CAD/US interest rate differential which moved from -83.5 last Wednesday to -75.9 yesterday. The narrow spreads should help limit USDCAD gains.

WTI is trading a tad firmer, rising from 788.75 to 79.38. Traders are a tad concerned that wild fires near Fort MacMurray, Alberta could disrupt 3.3 million b/day of crude supply and because Opec left its forecast that world oil demand would rise by 2.25 million b/day in 2024, unchanged.

USDCAD Technicals

The intraday USDCAD technicals are bearish below 1.3690 and looking to test the support line at 1.3620 that stretches back to April 10, on a four hour chart. A break above 1.3690 targets 1.3760.

The longer term technicals are unchanged and bullish while prices are above 1.3590. A break above 1.3740 targets 1.3900.

For today USDCAD support is at 1.3630 and 1.3610. Resistance is at 1.3690 and 1.3720. Today’s range is 1.3630-1.3720.

Chart: USDCAD 4 hour

Source: DailyFX

US Slaps China with More Tariffs.

The US election is proving costly for Chinese manufacturers. Trump got elected partly because he adopted a hard-line stance on what he described as unfair trade practices by China. Joe Biden decided that if that tactic worked for Donny, it would work for him. Biden announced an additional $18 billion in increased tariffs on Chinese electric vehicles, batteries and solar panels, among others.

Powell and Producer Prices Setting Up CPI

PPI rose 0.5% m/m in April (forecast 0.3%) and well above the downwardly revised -0.2% in March. PPI-ex food and energy rose 0.5% and the March result was revised lower to -0.1 from 0.2% m/m. The US Bureau of Labor Statistics noted, “On an unadjusted basis, the index for final demand moved up 2.2 percent for the 12 months ended in April, the largest increase since rising 2.3 percent for the 12 months ended April 2023.

That is not the direction that policymakers want to see. This mornings results should keep the greenback underpinned until tomorrow’s CPI release.

Fed Chair Jerome Powell is speaking from Amsterdam at 10:00 am although he is not expected to change his “wait and see” outlook.

EURUSD

EURUSD inched higher, rising to 1.0796 from 1.0775. The single currency is underpinned by improved ZEW Economic Sentiment which climbed to 47.1 from 42.9 in March. The Economic Situation also improved, rising 6.9 points to -72.3 but the economic pessimists are still firmly in control.

GBPUSD

GBPUSD dropped then popped in a 1.2509-1.2564 range after the UK employment report and comments by BoE Chief Economist Huw Pill, before settling at 1.2548 in early NY trading. Mr. Pill said, “I think it’s not unreasonable to believe that through the summer we will begin to see enough confidence in the decline in persistence that Bank Rate will come into consideration.” The UK jobs data was mixed. The employment market is cooling but wage growth is steady. UK ONS wrote, “Annual average regular earnings growth for the public sector remains strong at 6.3%; for the private sector, this was 5.9%, with growth last lower than this in April to June 2022 (5.4%).”

USDJPY

USDJPY extended yesterday’s rally and climbed from 156.15 to 156.57 which prompted Finance Minister Shunichi Suzuki to say “We’ll closely monitor the currency and take all possible measures.” He was ignored.

AUDUSD AND NZDUSD

AUDUSD traded quietly in a 0.6598-0.6313 range. Price action was abysmal due to a lack of actionable local data and the wait until US CPI is released. NZDUSD is at the top of its 0.6010-0.6029 range. NZ electronic card retail sales fell 3.8% y/y in April but any negativity was offset with the March results being revised lower, from -3.0% to -2.3%.

USDMXN

USDMXN traded in a 16.7715-16.8215 range and is sitting close to the session low in early NY trading. The initial “buy USD” reaction on fears of a renewed global economic slowdown after Biden announced new tariffs on China faded quickly. Traders are non-committal ahead of pending US inflation data. Banxico is expected to cut rates from 11.00% to 10.75% in June.

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1053 vs exp. 7.2307 (prev. 7.1030).

Shanghai Shenzhen CSI 300 fell 0.21% to 3657.05.

April CPI 0.1% m/m and 0.3% y/y (previous 0.1%), PPI -2.5%y/y (forecast -2.2, previous -2.8

US raises tariffs on $18 billion of imports of semi-conductors, batteries, solar cells and critical minerals as well as other tariffs.

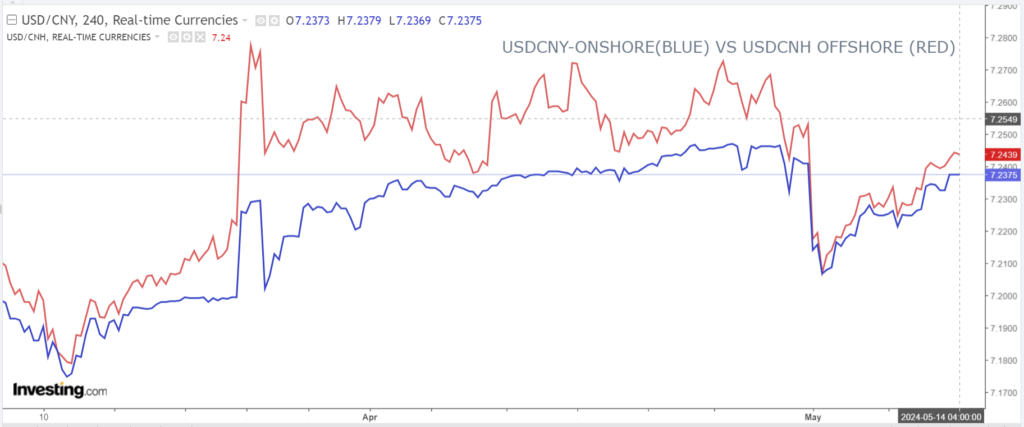

Chart: USDCNY and USDCNH

Source: Investing.com