Photo: freepik

June 14, 2023

- Markets moving sideways until FOMC.

- UK April GDP rises 0.2% as expected.

- US dollar trading sideways and defensively.

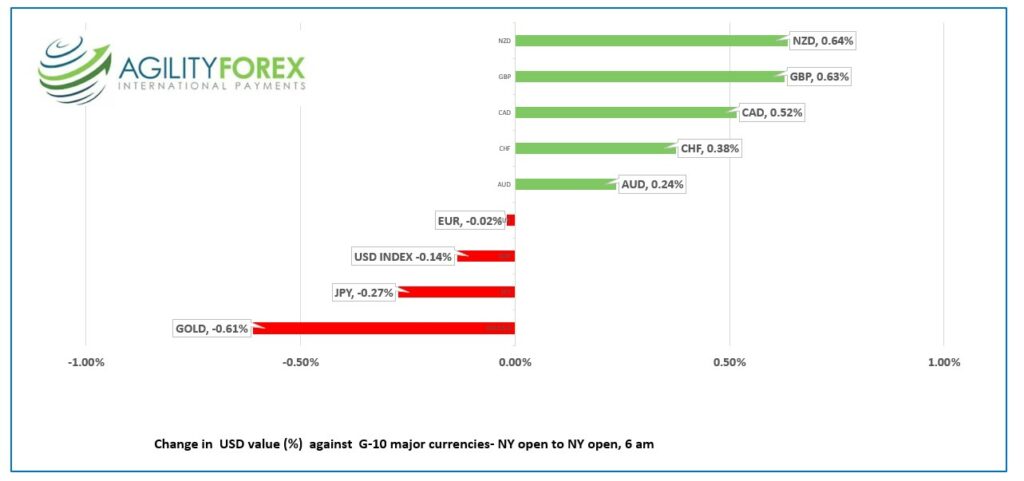

FX at a glance

Source: IFXA Ltd/

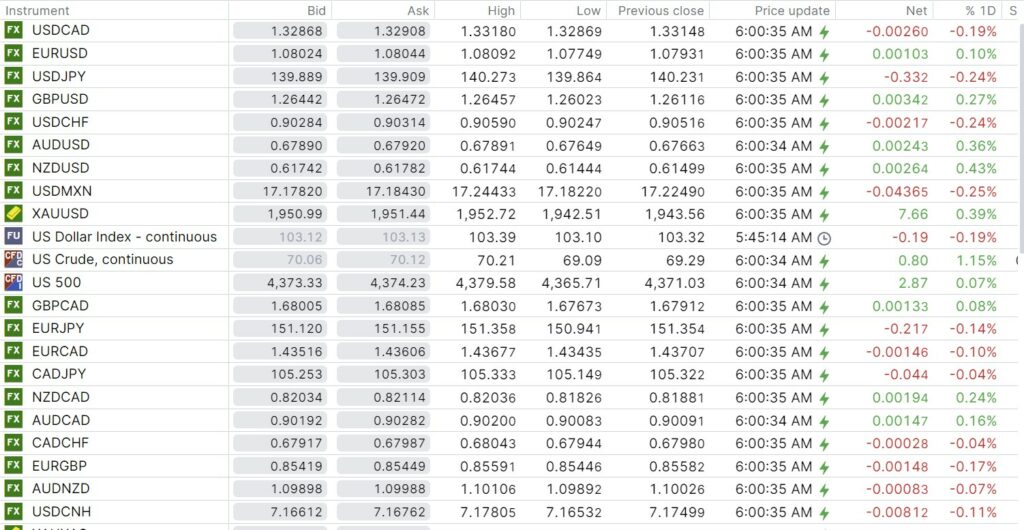

USDCAD Snapshot: open 1.3287-91, overnight range 1.3287-1.3318, close 1.3315

USDCAD is testing support in the 1.3290 area. The downside pressure is almost all due to widespread US dollar selling pressures on speculation that the Fed is at the end of its tightening cycle. In addition, hopes for higher oil prices and the latest BoC rate hike are also contributing to the downward pressure on prices.

WTI oil rose from $69.09/b to $70.46/b during the overnight session, supported by the American Petroleum Institute (API) reporting a 1.02 million barrel increase in crude stocks last week. The International Energy Agency warned that oil demand growth will slow down as it approaches its peak in 2028. The IEA predicts that this decline will be due to the increased use of electric vehicles, although the agency did not specify the source of all the required electrical capacity.

The direction of USDCAD will be determined by today’s FOMC meeting.

USDCAD Technical Outlook

The USDCAD technicals are bearish below 1.3360 and looking for a break below the 1.3270-1.3290 area to extend losses to 1.3220. A break above 1.3360, negates the downtrend and suggests a period of 1.3270-1.3460 consolidation.

The long term uptrend line is intact while prices are above 1.2990, and it will be tested on a break below 1.3220 which is also the 38.2% Fibonacci retracement level of the May 2021 -October 2022 range. If broken, it puts 1.2760 ( 61.8 Fibonacci) in play.

Today’s range 1.3240-1.3340.

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

“To be or not to be, to skip or not to skip?” Those are the questions. The answers will come after 2:00 pm EDT today when the FOMC releases its monetary policy statement and Fed Chair Jerome Powell’s press conference. The Fed is expected to hike by 25 bps, with the quarterly Summary of Projections being a key focus. Analysts will be seeing more dots than at a Dalmatian day at the dog park.

Yesterday, the US inflation report showed inflation slowing enough to allow the Fed to skip a rate hike but not enough to suggest rates will be lowered at any time in 2023. Nevertheless, the CPI report gave Wall Street a boost, and Asian equity indexes followed suit. Japan’s Nikkei 225 index rose by 1.42%, while Australia’s ASX 200 index gained 0.32%. European bourses shrugged off a sluggish open and are posting gains, led by the French CAC 40 index, which has risen by 0.67%. S&P 500 futures are up by a mere 0.11%, while the US 10-year Treasury yield, at 3.82%, has barely changed. WTI oil and gold prices are also higher.

China’s Foreign Minister Qin Gang reportedly chastised US Secretary of State Blinken in a phone call. Mr. Gang said the US should stop interfering in China’s internal affairs, respect China’s view on Taiwan, and stop hurting China using competition as an excuse. Mr. Blinken’s press release was far vaguer and more diplomatic. The call is a prelude to rumored Blinken’s China visit, scheduled for June 18.

EURUSD traded in a range of 1.0775-1.0809, with prices consolidating post-US CPI gains and in anticipation of the Fed skipping a rate increase. Eurozone industrial production rose by 1.0% compared to the 3.8% drop in March, which analysts described as an underwhelming recovery. EURUSD needs to break above 1.0850 or risk a retest of 1.0700.

GBPUSD climbed from 1.2602 to 1.2648 on broad-based US dollar weakness and garnered a bit of support from the 0.2% rise in April GDP compared to the -0.3% drop in March. Some analysts are suggesting that the March GDP recovery reduces the risk of a recession. However, Deputy Chief Economist Ruth Gregory at Capital Economics disagrees. She said high interest rates will drive the economy into a recession.

USDJPY consolidated yesterday’s gains in a range of 139.86-140.27. The gains are supported by expectations for a hawkish Fed “skip” and another dovish BoJ monetary policy meeting on Friday.

AUDUSD traded sideways in a range of 0.6764-0.6793, supported by hopes that the US rate hike cycle has ended and by higher commodity prices.

The US Producer Price Index fell 0.3% m/m in May (forecast -0.1%, April 0.2% m/m)

.,FX open, high, low, previous close as of 6:00 am ET

Source: Bloomberg

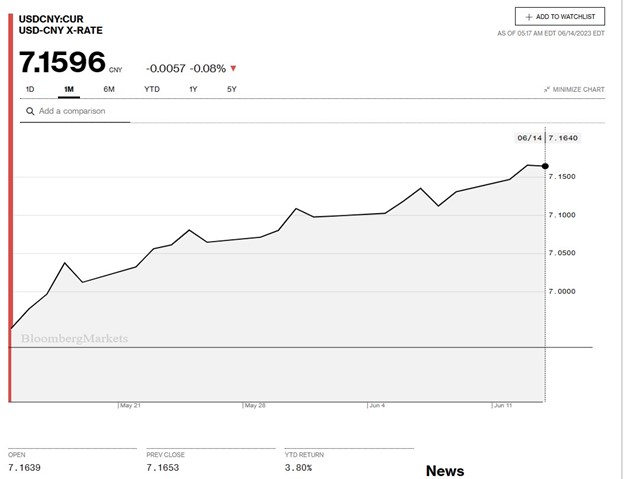

China Snapshot

Bank of China Fix: 7.1566, previous 7.1498

Shanghai Shenzhen CSI 300 fell 0.02% to 3864.02.

Chart: USDCNY 6 month

Source: Bloomberg