Photo: freepik

June 15, 2023

- ECB hikes 25 bps, raises inflation forecast.

- US Retail Sales rebound.

- US dollar opens mixed-JPY underperforms.

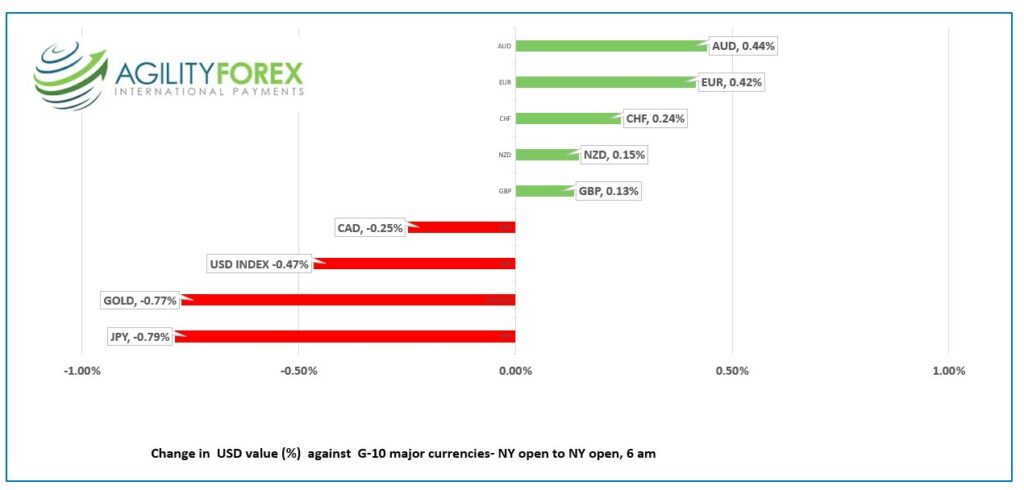

FX at a glance

Source: IFXA Ltd/

USDCAD Snapshot: open 1.3320-24, overnight range 1.3322-1.3353, close 1.3323

USDCAD direction did not become any clearer even after the FOMC surprised markets by projecting at least two more rate increases in 2023. USDCAD rallied from 1.3270 before the Fed announcement to 1.3350 afterwards, then consolidated the gains overnight.

USDCAD is struggling to make further gains because the Bank of Canada’s forward guidance is somewhat hawkish after it ended its “rate pause” period on June 7 when it raised rates by 25 bps. The BoC statement indicated that monetary policy was not sufficiently restrictive which implies another rate increase sooner, rather than later.

WTI oil prices chopped about in a $68.02-$69.06 range. Support from the EIA report of a 7 .92 million barrel build in US crude inventories was offset by the hawkish Fed outlook.

USDCAD direction will follow broad US dollar sentiment while the prospect of higher oil prices and a hawkish BoC may slow gains.

Canadian May housing starts fell to 202,500 from 261,400 in April while Manufacturing Sales rose 0.3% (forecast -0.2%). ahead.

USDCAD Technical Outlook

The USDCAD technicals are unchanged. Support in the 1.3250-70 area held but gains were capped by the June downtrend line.

The intraday USDCAD technicals are bearish below 1.3360 and looking for break below 1.3305 to extend losses to the 1.3270 support area. A downside break targets 1.3220. A move above 1.3360 targets 1.3420 then 1.3460.

The long term uptrend line is intact while prices are above 1.2990, and it will be tested on a break below 1.3220 which is also the 38.2% Fibonacci retracement level of the May 2021 -October 2022 range. If broken, it puts 1.2760 ( 61.8 Fibonacci) in play.

For today, USDCAD support is at 1.3305 and 1.3270. Resistance is at 1.3360 and 1.3420

Today’s range 1.3290-1.3380

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

The Fed is proving that forward guidance ain’t what it used to be. Fed Chair Jerome Powell set the market up for a pause before one final rate increase. The FOMC members had other plans and projected two more rate hikes in 2023.

When the dust settled, the US dollar was mixed and mostly for non-US reasons. AUD rallied in anticipation of more RBA rate hikes, while recession news sank NZD. EUR and GBP rallied ahead of today’s ECB meeting.

Not surprisingly, US Treasury yields rose, but so did Wall Street, at least initially. The S&P 500 closed with a tiny 0.06% gain, the Nasdaq rose 0.39%, while the Dow Jones dropped 0.68%.

Asian markets closed with gains except for those in Japan. European bourses are trading negatively in the wake of the ECB announcement.

S&P 500 futures retreated overnight and are down 0.28% in early NY trading. Oil traders are torn between hopes for Chinese stimulus to boost global demand and fears of higher US interest rates. The higher US rate outlook spooked gold traders, and prices are probing support in the $1935.00 area.

Today’s US data dump was mixed. Initial jobless claims were weaker than forecast (262,000 vs forecast 249,000 and the Philadelphia Fed Manufacturing Index was -13.7 compared to the previous reading of -10.4. On the plus side, Retail Sales rose 0.3% m/m (forecast -0.1%) and the Empire State Manufacturing Index jumped to 6.6 compared to the forecast of -15.1.

EURUSD churned post-FOMC and finally found its footing at 1.0805 in Asia. Prices climbed steadily to 1.0877 in early NY, just after the ECB raised its benchmark rate by 25 bps to 3.50%. The inflation forecast was revised higher with headline CPI rising to 5.4% in 2023 (previous 5.2%) and to 3.0% in 2024 (previous 2.9%). Core inflation is seen at 5.1% for 2023 compared to the previous estimate of 4.6%. The GDP forecast ticked down to 0.9% from 1.0%. The ECB press conference is just starting.

GBPUSD traded in a 1.2631 to 1.2673 range. Traders are keeping their eye on US dollar sentiment following today’s US data releases while awaiting the ECB press conference.

USDJPY jumped from 139.95 to 141.50 following the hawkish Fed surprise which lifted the US 10-year yield to 3.845% today. The yield slid to 3.79% after the US data and USDJPY dropped to 140.85. Traders are awaiting tomorrow’s BoJ meeting which could see a yield curve control (YCC) tweak, according to JPMorgan.

AUDUSD traded with a bullish bias in a 0.6768-0.6827 range. Prices were underpinned by the latest PboC rate cut and expectations for another round of fiscal stimulus. Australia added 75,900 new jobs (forecast 15,000), and Consumer Inflation expectations rose which suggests the RBA may raise rates at the next meeting in July.

NZDUSD underperformed and is at the bottom of its 0.6163-0.6216 range. The Q1 GDP report showed the country entered a technical recession. Q1 GDP fell 0.1% q/q following a 0.7% drop in Q4 GDP.

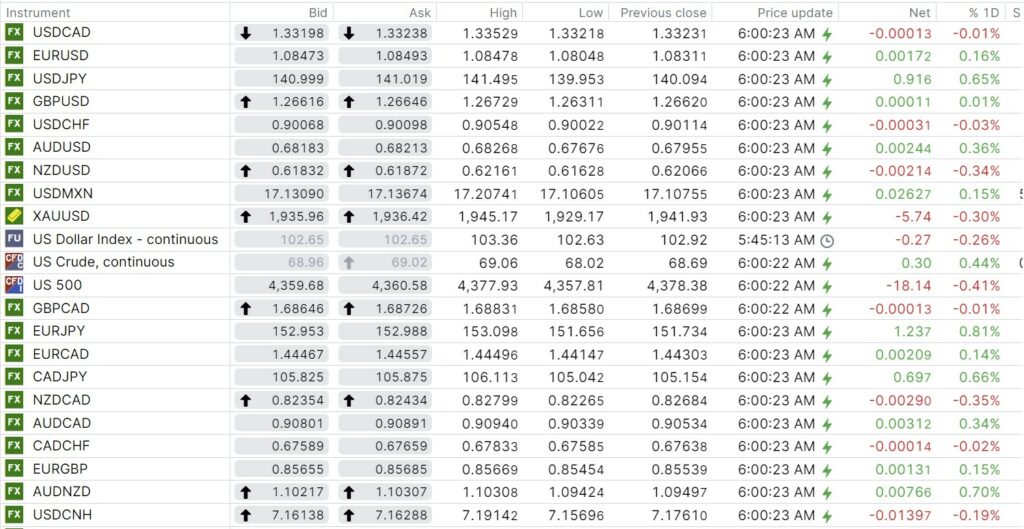

FX open, high, low, previous close as of 6:00 am ET

Source: Bloomberg

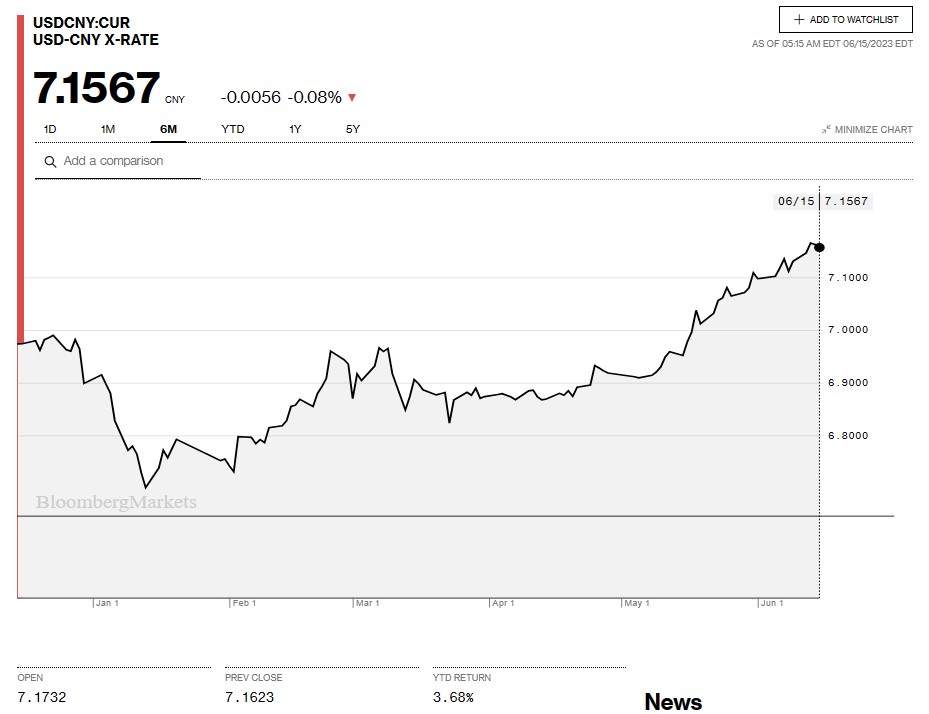

China Snapshot

Bank of China Fix: 7.1489, previous 7.1566

Shanghai Shenzhen CSI 300 rose 1.59% to 3925.50.

PboC cuts 1-year medium term lending facility rate to 2.65% from 2.75%.

China Retail Sales rose 12.7% y/y in May vs 18.4% in April. Industrial production rose 3.5% y/y vs 5.6% in April.

Analysts suggest the latest rate cuts and anticipated Loan Prime Rate cuts (June 20) reflect the governments concerns about the sluggish economy. The analysts expect additional fiscal stimulus measures will be announced soon.

Chart: USDCNY 6 month

Source: Bloomberg