Source: HDClipart.com

- ECB hikes 75 bps with more increases likely

- Risk sentiment improves with lower Treasury yields.

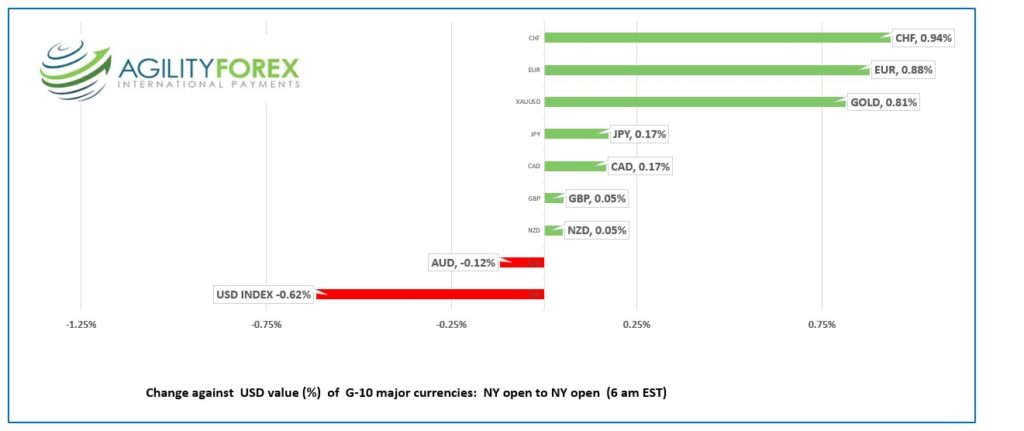

- US dollar gives back some gains, CHF outperforms

FX at a glance:

Source: IFXA Ltd/RP

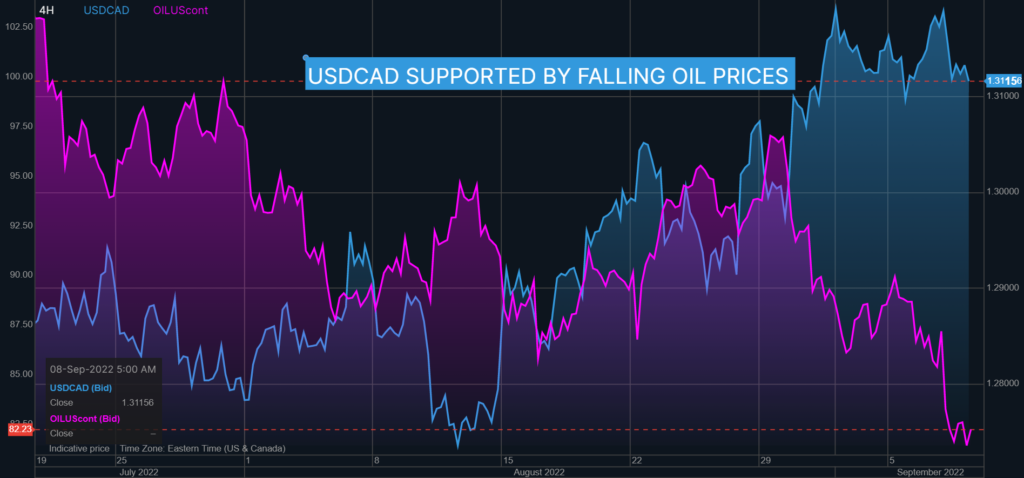

USDCAD Snapshot open 1.3136-40, overnight range 1.3108-1.3146, close 1.3120

USDCAD dropped following the Bank of Canada’s 75 bp rate hike. However, the BoC’s actions were not a factor in the sell-off, which was all due to the Wall Street rally which lifted the S&P 500 index from 3908.19 to 3979.87.

BoC Deputy Governor Carolyn Rogers will give more details on the BoC’s rate hike decision this afternoon in a speech in Calgary (2:30 pm ET). She is unlikely to say anything more than the Bank is committed to bringing inflation down to its 2.0% target.

USDCAD is not getting any support from crude prices. WTI oil broke through support at $85.90/b decisively yesterday and the technicals suggest further losses to $59.10/b. The sell-off is exacerbated by stale “long crude” positions getting unwound and by elevated concerns that China’s covid lockdowns is choking off demand. The API crude stocks report showing US inventories rose 3.65 million barrels as of September 2, didn’t help.

There are no Canadian economic reports today.

USDCAD Technical outlook

The intraday USDCAD technicals are bullish above 1.3060 representing the uptrend line from August 12 and previous resistance. A break above resistance in the 1.3210 area will extend gains to 1.3230 and then 1.3340. A break below 1.3060 suggests steeper losses to 1.2980.

For today, USDCAD support is at 1.3080 and 1.3050. Resistance is at 1.3160 and 1.3190. Today’s range: 1.3060-1.3160

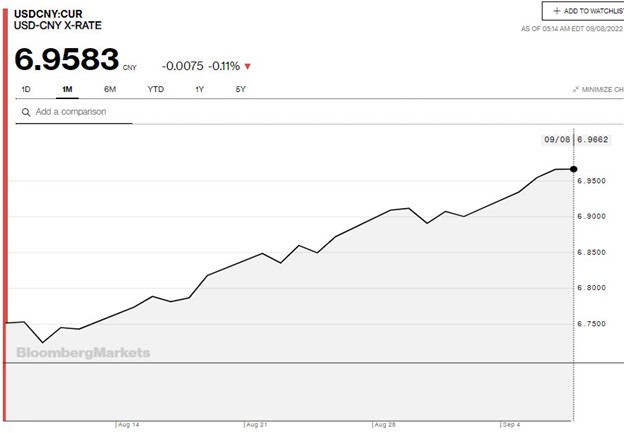

Chart: USDCAD and WTI oil 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

Traders were getting tired of being negative and grasped at straws to find something positive yesterday.

They found it when the US 10-year Treasury slid from its peak of 3.344% to 3.222%. Wall Street rallied, and the greenback retreated.

Fed Vice Chair Lael Brainard echoed earlier hawkish sentiment when she said rates need to rise “to get inflation down.” The comments weren’t new and were ignored.

Overnight, markets were far more cautious and looking ahead to today’s ECB monetary policy announcement and press conference.

Asia equity indexes followed Wall Street’s lead and closed with gains led by a 2.31% rise in Japan’s Nikkei 225 index. European bourses were subdued but posted small gains except for the German Dax, which dipped 0.31%. S&P 500 and DJIA futures are flitting around unchanged.

Gold prices are modestly higher, while WTI oil is unchanged from the NY close.

Risk sentiment may sour again, after Fed Chair Jerome Powell’s remarks in Washington, starting at 9:10 am.

US data weekly jobless claims were 222,000 well below the forecast 240,000, and better than the downwardly revised (228,000) results last week. The news helped undermine recent S&P 500 gains.

EURUSD traded narrowly in a 0.9977-1.0029 overnight, then dropped from the peak to 0.9992 after the ECB raised rates 75 bps, as expected. The statement suggested policymakers were more concerned about soaring inflation that economic risks from higher rates.

The statement said, “This major step frontloads the transition from the prevailing highly accommodative level of policy rates towards levels that will ensure the timely return of inflation to the ECB’s 2% medium-term target.” That comment implies a smaller rate increase next time. Christine Lagarde’s press conference to provide direction.

Analysts speculate that escalating energy tensions following Russia shutting down Nord Stream 1 and the EU planning to cap Russian gas import prices will limit any EURUSD rally from a rate hike.

GBPUSD climbed from 1.1478 to 1.1560 due to profit-taking after risk sentiment improved. Some analysts are disillusioned after earlier comments by Bank of England officials suggesting a timid pace to rate hikes. Policymaker Silvana Tenreyro said, “I judged that the more gradual pace of tightening will allow us to reduce those risks, because we will see the effects of the data and we can always stop.” GBPUSD sellers are likely to emerge if prices get near the 1.1630 area.

USDJPY came within inches of 145.00 yesterday and traded in a 143.44-144.55 range overnight. Traders will continue to drive prices higher until they force the Bank of Japan to either scrap the 0.25% yield curve control cap or intervene in FX. Intervention is most unlikely as it would be ineffective.

AUDUSD is trading near the bottom of its overnight 0.6715-0.6773 range, erasing all yesterday’s gains. Worse than expected traded data (actual 8.733 billion vs 17.13 billion) due to sharply lower iron-ore and coal exports. Prices were also weighed down after RBA Governor Philip Lowe said, “All else equal, the case for a slower pace of increase in interest rates becomes stronger as the level of the cash rate rises.” Really? No kidding.

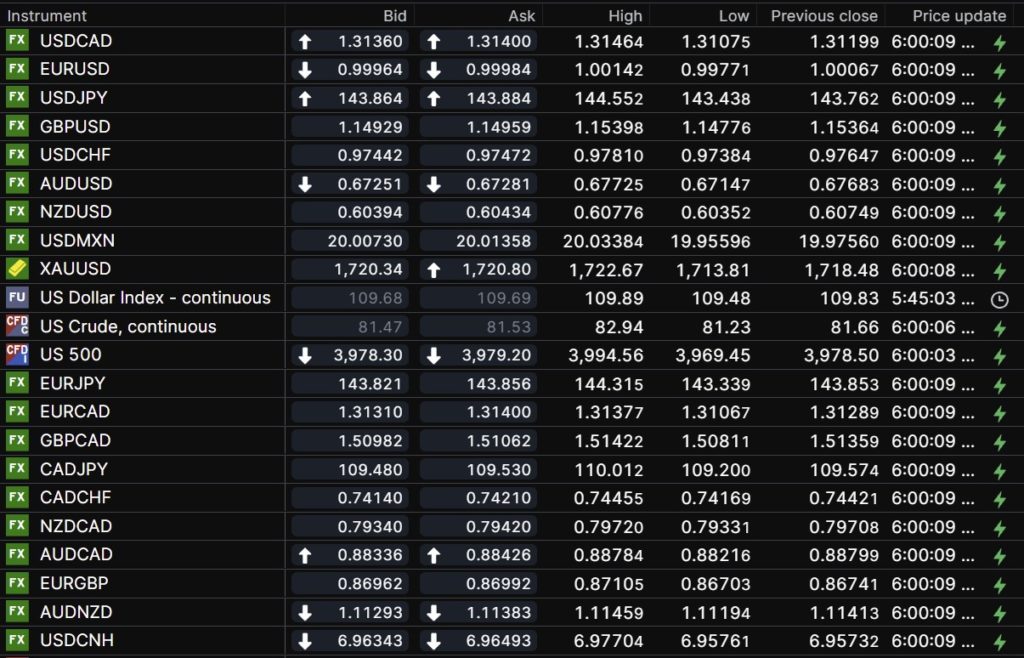

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

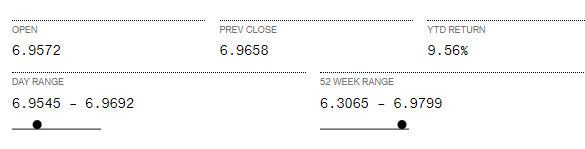

China Snapshot

Today’s Bank of China Fix: 6.9148, previous 6, 6.9160

Shanghai Shenzhen CSI 300 rose 0.49% to 4,037.66

CNN reports that since August 20, 74 cities with a population total of 313 million are in various lockdown stages, including 15 provincial capitals.

Chart: USDCNY 1 month

Source: Bloomberg