Image by DALL-E, Imagined by me.

December 12, 2023

- Financial markets on hold ahead of FOMC this afternoon.

- EIA cuts oil price forecast, upwardly revised US production.

- US dollar opens steady-consolidates yesterday’s post CPI gains.

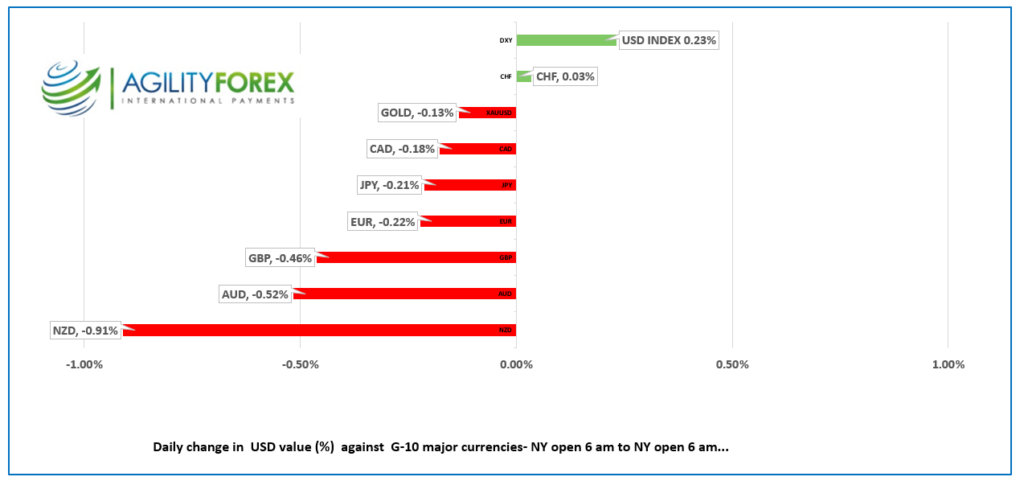

FX at a glance

Source: IFXA/RP

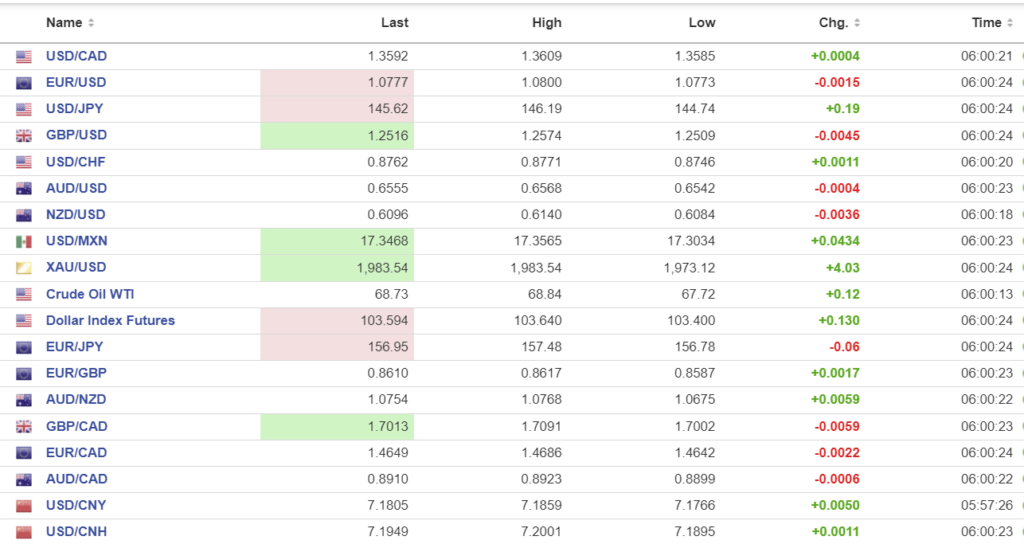

USDCAD Snapshot: open 1.3590-94, overnight range 1.3585-1.3609, close 1.3590

USDCAD sat at 1.3555 yesterday just ahead of the US inflation data, then popped to 1.3620 after the results were a tad disappointing. Headline inflation increased 0.1% m/m (forecast 0.0), while the more important Core-CPI was unchanged at 4.0%. The Fed’s inflation target is 2.0%, hence the market unhappiness. Analysts do not believe the results will change the FOMC’s outlook for rates, but CME futures traders have pushed out expectations for the first rate cut to May from March.

The US Energy Information Administration (EIA) slashed its forecast for Brent Crude to $83.00/barrel from $93.00/b for 2024, citing “ongoing concerns around global oil demand growth,” for the move. The agency is also predicting increased US crude exports.

Meanwhile, COP28 wrapped up with a request for countries to contribute to the global transition effort from fossil fuels to other sources of renewable energy, which do not yet exist in any commercially viable manner. Failure to adhere to the request does not have any consequences. The conference concluded, and none of the delegates left on solar-powered aircraft or drove away in electric vehicles.

Canada’s Environmental Minister and Chinese Communist Party employee, Steven Guilbeault, continues to spend Canadian tax dollars to advise Beijing on how to build two coal-fired electricity plants each week. Apparently, coal emissions are green energy if the green is US dollars.

WTI prices extended the November decline and fell from $68.85/b to $67.72/b overnight.

USDCAD Technicals:

The intraday USDCAD technicals turned bullish yesterday with the rally through 1.3570 and is in an uptrend above 1.3580, on an hourly chart. A break above 1.3620 will extend gains to 1.3660, while a break of 1.3580 will target 1.3540. Both sides could be tested after today’s FOMC meeting.

Longer term, USDCAD is forming a triangle or wedge on the daily chart. The uptrend line from July will , currently at 1.3510, will soon meet the downtrend line from the November peak at 1.3760. A break of either side will result in a 500 bp move.

For today, USDCAD support at 1.3550 and 1.3510. Resistance is at 1.3620 and 1.3660. Today’s range 1.3560-1.3660.

Chart: USDCAD daily

Source: Investing.com

G-10 FX recap

Oil sheiks may be having temper tantrums over falling prices, but Fed Chair Jerome Powell may be feeling a little smug about his interest rate outlook. Mr. Powell has been steadfast in his view that US rates may need to remain at elevated levels for longer than the market expects, and yesterday’s CPI data supported his outlook. Inflation is falling, but at a snail’s pace, and more work may need to be done before CPI hits the 2.0% target.

This afternoon’s FOMC statement and Powell’s press conference is enough event risk for traders to enjoy an extended breakfast. US Producer Price data ( actual 0 % m/m vs forecast 0.1% had little immediate impact on markets.

Asian equity indexes closed with small gains, led by a 0.37% rise in Australia’s ASX 200. European bourses are in positive territory with the UK FTSE 100 posting a 0.32% gain. S&P 500 futures are up 0.10% while the US 10-year Treasury yield is just above the overnight low at 4.17%.

EURUSD traded in a 1.0773-1.0800 range as it consolidated yesterday’s post-CPI losses. Eurozone Industrial Production was weaker than expected, falling 0.7% in October, compared to September’s 0.1% decline. German politicians have reportedly come to a budget agreement which avoided suspending the “debt brake.”

GBPUSD is having a bad day and trading negatively in a 1.2509-1.2574 range. The UK economy contracted by 0.3% in October. Industrial Production and Manufacturing production were worse than expected. That led to Goldman Sachs and JPMorgan cutting their UK GDP growth forecasts to 0.5% from 0.6%.

USDJPY had another choppy session with a 144.74-146.19 range. The Tankan survey was better than expected with Business confidence at large Japanese manufacturers rising to a two-year peak. The results provided some support to those expecting the BoJ to begin tightening monetary policy.

AUDUSD traded in a 0.6542-0.6568 range with prices tracking broad US dollar sentiment.

NZDUSD dropped to 0.6084 from 0.6140 overnight and was the worst-performing G-10 currency. Traders appeared unhappy with news that the NZ current account deficit widened.

FX high, low, open (as of 6:28 am ET)

Source: Investing.com

China Snapshot

PBoC fix: today 7.1163, expected 7.1717, previous 7.1174.

Shanghai Shenzhen CSI 300 fell 1.67% to 3369.60.

Chinese equity traders disappointed about lack of fresh stimulus news and dumped stocks.

Chart: USDCNY and USDCNH

Source: Investing.com