Photo: HDClipart.com

- Risk sentiment soars in wake of soft CPI data

- US PPI slides, jobless claims as expected

- US dollar opens with large losses, AUD outperforms

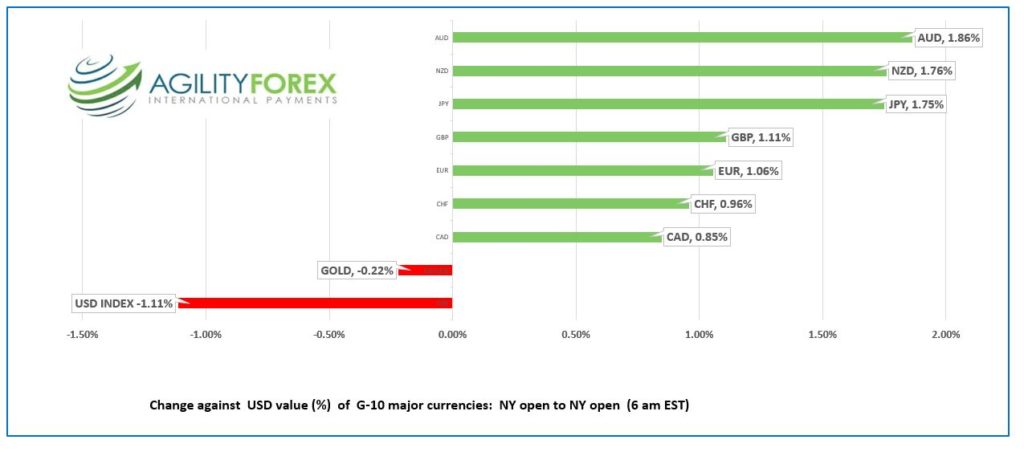

FX at a glance:

Source: IFXA Ltd/RP

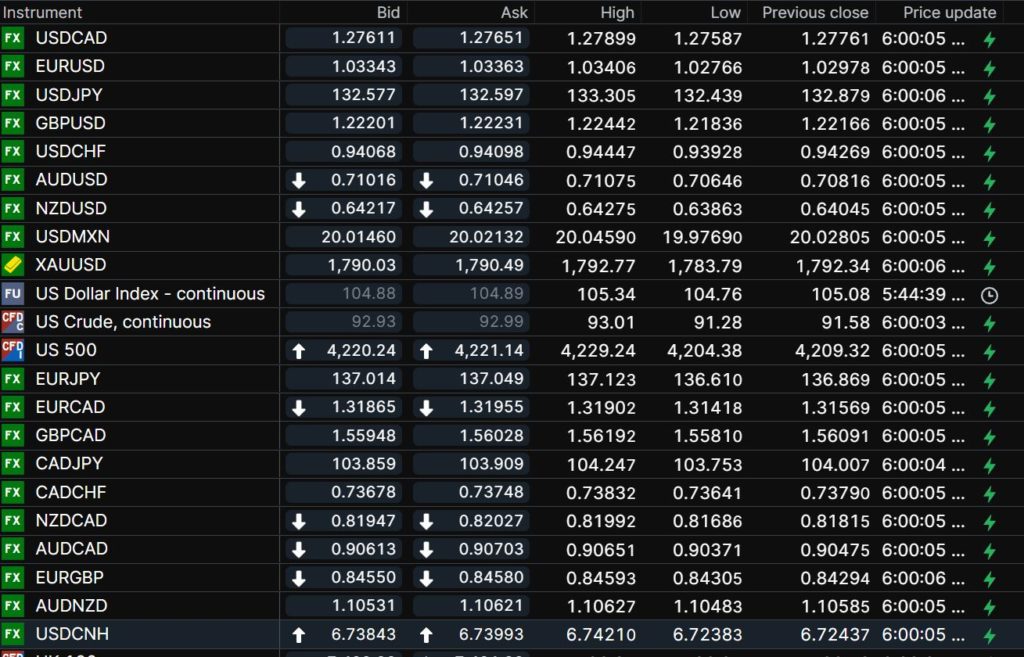

USDCAD Snapshot: open 1.2761-65, overnight range 1.2759-1.2790, close 1.2776

USDCAD dropped in response to broad US selling pressures after the US CPI print, and by a rebound in West Texas Intermediate oil prices. USDCAD direction is at the whim of broad US dollar moves and exaggerated due to reduced volumes from summer holidays.

USDCAD downside is limited because Canada’s economy is underperforming that of the US. Canada lost jobs two months in a row while the US added over 900,000 in the same period. The odds the Fed can engineer a soft landing are far better than the BoC’s chances, and both central banks are raising rates aggressively.

There are not top tier economic reports today.

USDCAD Technical outlook

The intraday USDCAD technicals turned bearish with yesterday’s move below 1.2850, then 1.2810, which extended losses to support at the 1.2750-60 area. A decisive breach below this level targets 1.2610, the uptrend line from June 2021. A break above 1.02850 suggests 1.2760-1.2890 consolidation.

For today, USDCAD support is in the 1.2750-60 area, then 1.2690. Resistance is at 1.2840 and 1.2880. Today’s range: 1.2740-1.2820

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

Wall Street greeted news of 8.5% US inflation warmly. “It wasn’t 9.1%.” July CPI rose 8.5% y/y, down 0.6% compared to June and below the 8.7% forecast.

Equity traders reacted to the news like Munchkins of Oz when a house fell on the Wicked Witch. The S&P 500 roared higher and closed with a 2.13% gain. The Nasdaq gained 2.89% and ended the longest Nasdaq bear market since 2008.

Equity traders ignored the part in the CPI report that showed the inflation decline was mainly due to falling oil prices and travel-related areas, both of which are anomalies. The sanctions on Russia are not going away, Chinese oil demand is not going to shrink dramatically, and airport dysfunction may be reversed, increasing travel demand.

Fed officials dismissed the equity reaction. San Francisco Fed President Mary Daly said it was far too early to declare victory and left the door wide open to another 75 bp hike in September. She added, “There’s good news on the month-to-month data that consumers and businesses are getting some relief, but inflation remains far too high and not near our price stability goal.”

Minneapolis Fed President Neel Kashkari said “”far, far away from declaring victory” on inflation and that he didn’t see anything that changes the need to raise rates to 4.4% by the end of 2023.

Bond traders are more circumspect. The US 10-year Treasury yield dropped from 2.77% to 2.688% immediately following the CPI data. Traders came to their senses, and yields settled into a 2.76-2.79% range.

Asian equity markets closed mixed. The Nikkei 225 lost 0.65% mainly due to yen strength, while Australia’s ASX 200 gained 1.12%. European bourses flipped from flat to lower to small gains. WTI oil is firmer while gold retreated from yesterday’s peak.

S&P 500 futures extended gains after today’s US data. The Producer Price Index for final demand fell 0.5 percent in July, seasonally adjusted. This decline followed advances of 1.0 percent in June and 0.8 percent in May. Weekly jobless claims were as expected. The results suggest inflation is falling and the economy is steady.

EURUSD extended yesterday’s rally and is trading at the top of its 1.0277-1.0342 range. The gains were fueled by stop-loss demand for EURUSD on the break above the 1.0280-1.0300 area and exacerbated by thin summer markets.

The reality is that Europe is still a basket case thanks to the Russia/Ukraine war and looming recession risks. The downtrend from February is intact below 1.0410.

GBPUSD mirrored EURUSD moves, rallying post-CPI and triggering stop losses on the move through resistance at 1.2180. GBPUSD consolidated the gains in a 1.2184-1.2244 range overnight. GBPUSD gains are limited to recessions risks, striking unions, and political uncertainty. Traders are looking ahead to Friday’s data dump, which includes Manufacturing Production, Industrial Production, and GDP (forecast 2.8% y/y)

USDJPY plunged in tandem with the drop in US Treasury yields and is trading near the bottom of its overnight 132.44-1.3331 range.

AUDUSD extended yesterday’s gains and trade in a 0.7065-0.7108 range, with prices supported by lower Consumer Inflation expectations data.

NZDUSD traded in a 0.6386-0.6428, underpinned by firmer commodity prices and broad US dollar weakness.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

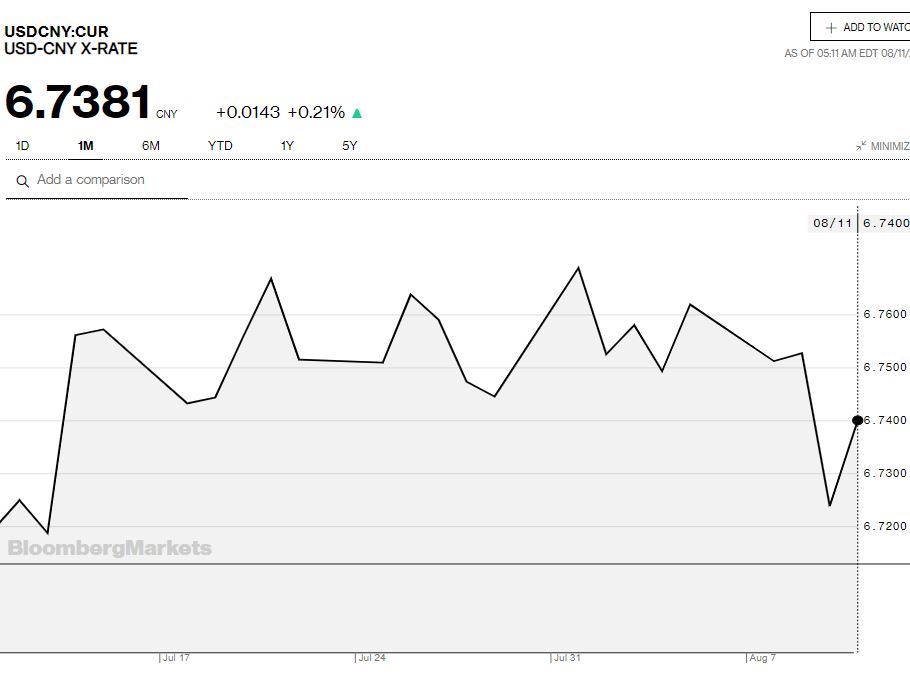

China Snapshot

Today’s Bank of China Fix: 6.7324, previous 6.7612

Shanghai Shenzhen CSI 300 rise 2.04% to 4,193.54

PboC forecasts inflation around 3.0% for 2022.

Rumours of a 15% increase in the average price of Apple iPhone 14, powered Apple parts suppliers higher, and positive sentiment leaked into other tech stocks.

Chinese property developers financial woes remain a concern

Chart: USDCNY 1 month

Source: Bloomberg