Source: Wikimedia commons

- Bank of Japan leaves monetary unchanged and intervenes in FX to sell USDJPY

- Global equity indexes retreat while USDX soars to 111.58, before dropping

- US dollar adds to gains, JPY modestly outperforms

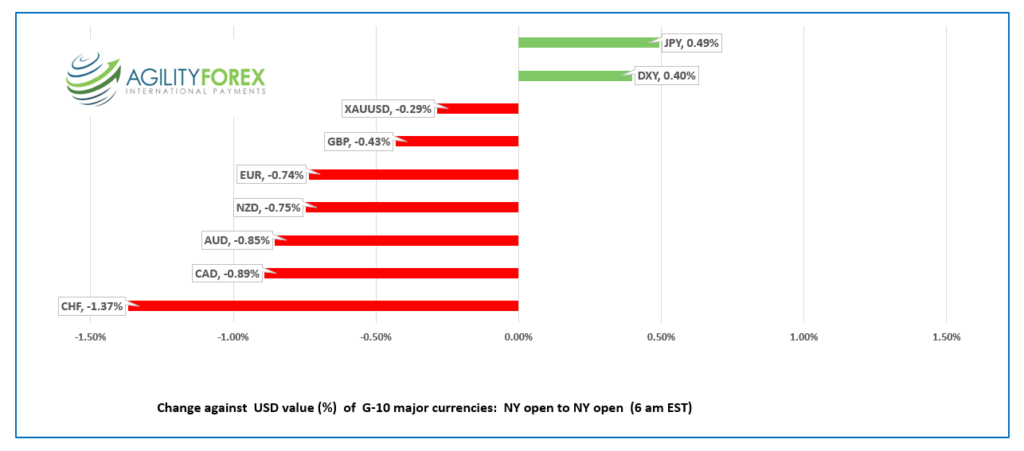

FX at a glance:

Source: IFXA Ltd/RP

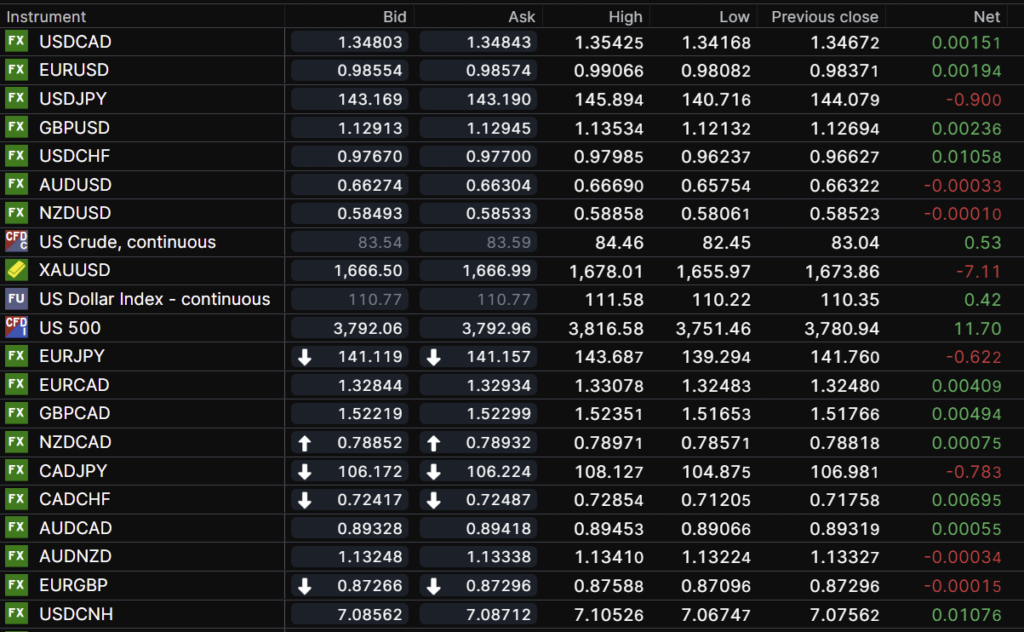

USDCAD Snapshot: open 1.3480-84 overnight range 1.3417-1.3543, close 1.3467

It’s the first day of fall or it will be a 9:04 pm ET. Investors have raked leaves and set them ablaze using Loonies as kindling.

USDCAD soared to 1.3542 in early European trading against a backdrop of Russian nuclear threats, and the prospect of another 125 bps in Fed rate hikes this year. Misery loves company, and the Canadian dollar is no exception. The other G-10 majors suffered a similar fate against the US dollar.

Yesterday’s suggestion to sell USDCAD in the 1.3380-90 area with a stop at 1.3440 was dead wrong and reinforced the adage “don’t fight the Fed.”

The outlook is rosy for USDCAD bulls. The breach of major resistance in the 1.3000 area followed by the break above 1.3200 targets 1.3860, the May 2020 support zone. USDCAD is underpinned as additional Federal government stimulus is largely offsetting the inflation fighting benefit of Bank of Canada rate increases. Further USDCAD support stems from global recession worries which are depressing commodity prices.

The next Bank of Canada meeting is over a month away, leaving USDCAD direction determined by global risk sentiment as measured by S&P 500 price action.

The Canadian economic data calendar includes the New Housing Price Index.

USDCAD Technical outlook

The intraday USDCAD are bullish above 1.3405, looking for a retest of the overnight 1.3543 peak which if broken, targets 1.3640. A move below 1.3405 suggests a further drop to 1.3320.

The break above 1.3200 blew the lid off the level that contained USDCAD gains since November 2020 and should now act as support. The break above 1.3440 targets 1.3660.

For today, USDCAD support is at 1.3440 and 1.3410. Resistance is at 1.3540 and 1.3590. Today’s range: 1.3420-1.3520

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

“Interest rates, inflation, and the third world war.”

Colin James sang similar lyrics in 1988. That year fed funds averaged 7.57%, inflation was 4.14%, and Russian politics were roiling markets-but in a good way.

Today, Fed funds are 3.25%, US inflation is 8.3%, and Russia is threatening nuclear war.

Fed Chair Powell and the FOMC dashed any hopes for a pivot in 2023. They hiked rates by 75 bps for the third move in a row. That was expected but the updated dot-plot forecast projecting another 125 bps in rate increases this year, with more to follow in 2023, was a bit of a surprise.

In addition, they raised their inflation estimates and only expect a small increase in the unemployment rate in 2023.

Deputy Chair of the Russian Security Council Chair and former president Dimitri Medvedev said that the Ukraine territories of Donetsk and Luhansk will be accepted back into Russia. He then said “Russian weapons, including strategic nuclear weapons and weapons based on new principles, could be used for such protection.”

US rate hike fears and Russian aggression fueled demand for US dollars and knocked equity markets lower.

The major Asian equity indexes closed with losses. The Nikkei 225 lost 0.58%, while Australia’s ASX 200 was closed for a National Day of Mourning for the Queen. European bourses are trading in negative territory, led by a 0.66% drop in the French CAC index. S&P 500 and DJIA futures are flitting around unchanged.

EURUSD is attempting to recoup yesterday’s losses. Prices hit 0.9813 in Asia then drifted higher, reaching 0.9907 just before NY opened.

Norway’s Norges Bank raised its benchmark rate by 0.50% to 2.25% due to rising inflation, while the Swiss National Bank (SNB) hiked 0.75 bp, taking the overnight rate to 0.50%, the first time it’s been in positive territory since 2015.

Those rate hikes didn’t help EURUSD, which is under pressure from Russia’s war in Ukraine.

GBPUSD plunged from 1.1363 to 1.1213 before bouncing to 1.1300 in the wake of the Bank of England’s 0.50% rate hike. The UK benchmark rate is now 2.25% with the increase designed to fight inflation.

Traders were not impressed. They expected a more aggressive response and took their frustrations out on the currency.

USDJPY traded wildly in a 140.72-145.89 range before settling at 142.78 in NY trading, thanks to Bank of Japan intervening in FX markets for the first time since 1998. Policymakers are concerned about the steep fall in the yen, while ignoring the fact the drop is because of its yield curve control policies. Capping Japan Government Bond yields at 0.25% while US rates are soaring is a recipe for a weak yen. BoJ officials do not see it that way and insist they need a stimulative monetary policy which is why they left it unchanged.

AUDUSD traded in a 0.6575-0.6669 range with price action dictated by broad US dollar moves. NZDUSD trade in a similar fashion.

US weekly jobless claims rose 216,750, close enough to the 218,000 forecast to be a non-factor.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

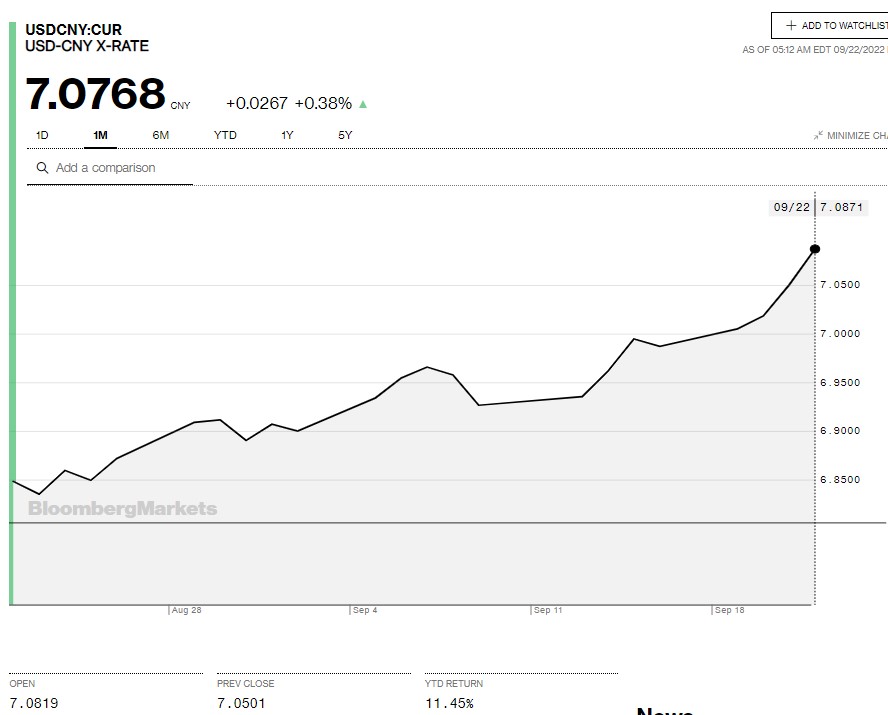

China Snapshot

Today’s Bank of China Fix: 6.9798, previous 6.9536

Shanghai Shenzhen CSI 300 fell 0.88% to 3,869.34

.Chart: USDCNY 1 month

Source: Bloomberg