Photo: Bing AI

September 22, 2023

- US 10-year Treasury yield retreats from 4.50%

- Canada Retail Sales ex-autos surge.

- US dollar consolidating gains.

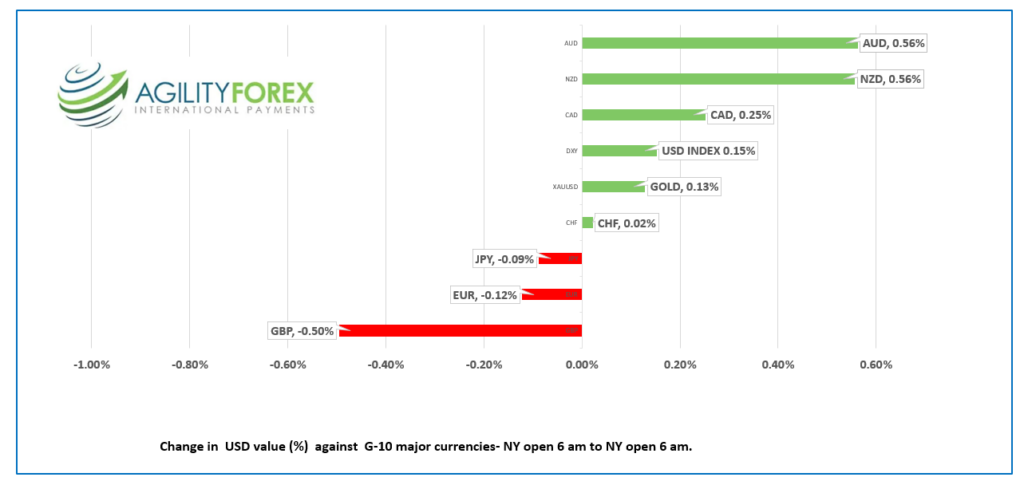

FX at a Glance

Source: IFXA/RP

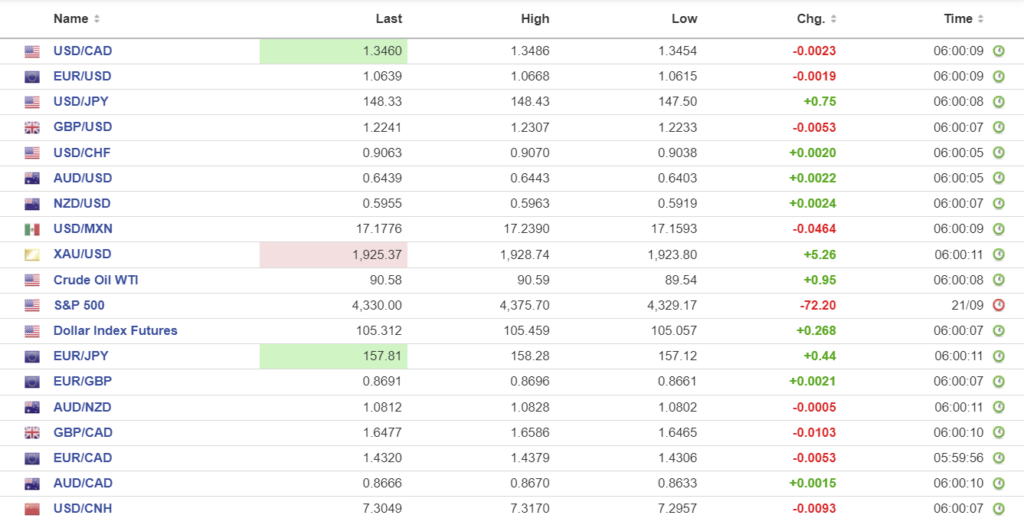

USDCAD Snapshot: open: 1.3460-64, overnight range: 1.3454-1.3486, close 1.3484.

USDCAD retreated from yesterday’s 1.3525 peak and is probing support in the 1.3430 area mainly due to higher commodity prices.

Canada retail sales rose 0.3% m/m in July, missing the forecast for a 0.4% gain but better than June’s 1.1% drop. However, Retail Sales, ex-autos rose 1.0%, which was double the forecast. The results may have been better but Statistics Canada reported that 17% of Canadian retailers had business activities affected by the BC port strike.

Oil prices recovered yesterday’s losses and WTI is near the top of its $89.54/b-$90.80/b range with traders once again focusing on reduced supply and rising demand. Analysts are hurriedly revising forecasts for $100.00/barrel supported by falling US crude inventories.

USDCAD support from the US 10-year Treasury yield at 4.462% is weighing on the S&P 500 index and resistance from rising crude prices suggests a USDCAD trading range of 1.3380-1.3550 until the BoC meeting in October.

USDCAD Technicals

The intraday USDCAD technical are bearish while trading below 1.3505 and looking for a break of 1.3430 to extend losses to 1.3390. A break above 1.3505 turns the technicals bullish and shifts the focus to 1.3600.

The uptrend line from July is intact above 1.3390 and the RSI studies on the daily chart suggest USDCAD is approaching oversold territory.

For today, USDCAD support is at 1.3430 and 1.3390. Resistance is at 1.3505 and 1.3550. Today’s range 1.3420-1.3510.

Chart: USDCAD daily

Source: Investing.com

G-10 FX recap

For people of a certain vintage, the seasons began on September 21. No longer. Just as 1 + 1 no longer equals 2 according to some uber-woke school boards, Autumn can begin any day between September 21 and September 24.

This year, traders are face-planting into the first day of fall (September 23) as they wrap their heads around the concept of interest rates remaining elevated for a long, long time and the increased risk of a US recession. Bond traders are getting the message. They drove the US 10-year yield from a low of 3.27% in April to 4.50% yesterday and over 40 bps since the beginning of the month.

EURUSD bounced around in a 1.0615-1.0668 range with the top and bottom levels seen around the release of German and Eurozone PMI data. The good news was that Composite PMI ticked up to 47.1, but the bad news was it is still in contraction territory and warns of negative GDP in the second half of the year. The EURUSD downtrend channel from July 19 is intact while prices are below 1.0780 and looking for a drop to 1.0520.

GBPUSD traded in a 1.2233-1.2307 range overnight and is the worst-performing major G-10 currency since yesterday’s NY open. The currency is reeling after the split decision which saw five members vote to leave rates unchanged and four members vote for a rate hike. GBPUSD is under pressure as traders believe yesterday’s decision signaled UK rates have peaked at 5.25%. UK data was mixed. Retail Sales rose 0.4% m/m in August while September Services PMI slipped to 47.2 from 49.5 previously. GBPUSD technicals are bearish below 1.2350 and targeting 1.2100.

USDJPY rallied after the Bank of Japan left interest rates unchanged and delivered its usual dovish outlook. Governor Ueda defended the decision, saying, “We have yet to foresee inflation stably and sustainably achieve our price target. That’s why we must patiently maintain ultra-loose monetary policy.” USDJPY gains were also fueled by US 10-year Treasury yields flirting with 4.50%. Japanese Core-CPI was unchanged at 4.3%, while Services PMI ticked down to 53.3 from 54.3.

AUDUSD grinded out gains due to end-of-week profit-taking and got an added boost after the Australian government posted its first budget surplus since 2008 (AUD 22 billion). Australian PMI data was mostly positive. Composite and Services PMI rose into expansion territory, while Manufacturing PMI was a tad softer at 48.2 (previous 49.6).

FX high, low, open

Source: Investing.com

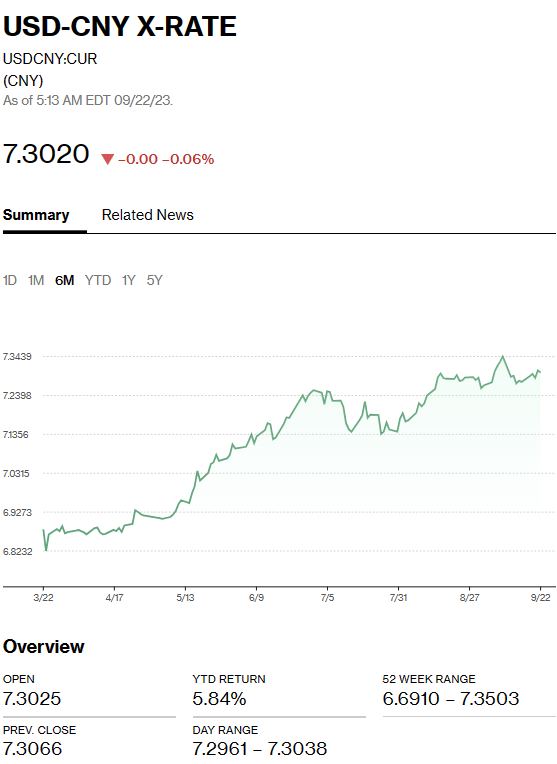

China Snapshot

Bank of China Fix: today 7.1729, expected 7.3009, previous 7.1730

Shanghai Shenzhen CSI 300 rise 1.81% to 3738.93.

Chart: USDCNY 1 month

Source: Bloomberg