Source: HDClipartall.com

- US 10-year Treasury yield sitting at 3.539%

- Canada Inflation cools

- US dollar drifts lower ahead of Wednesday’s FOMC meeting

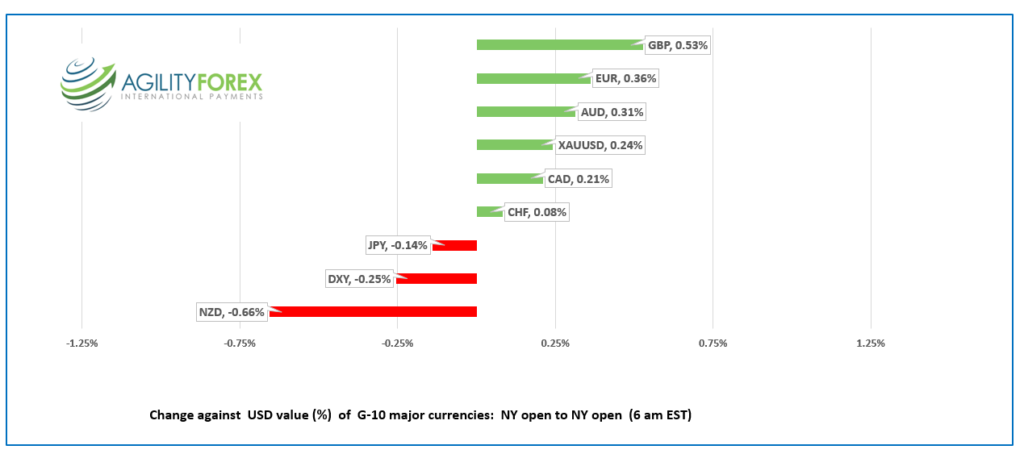

FX at a glance:

Source: IFXA Ltd/RP

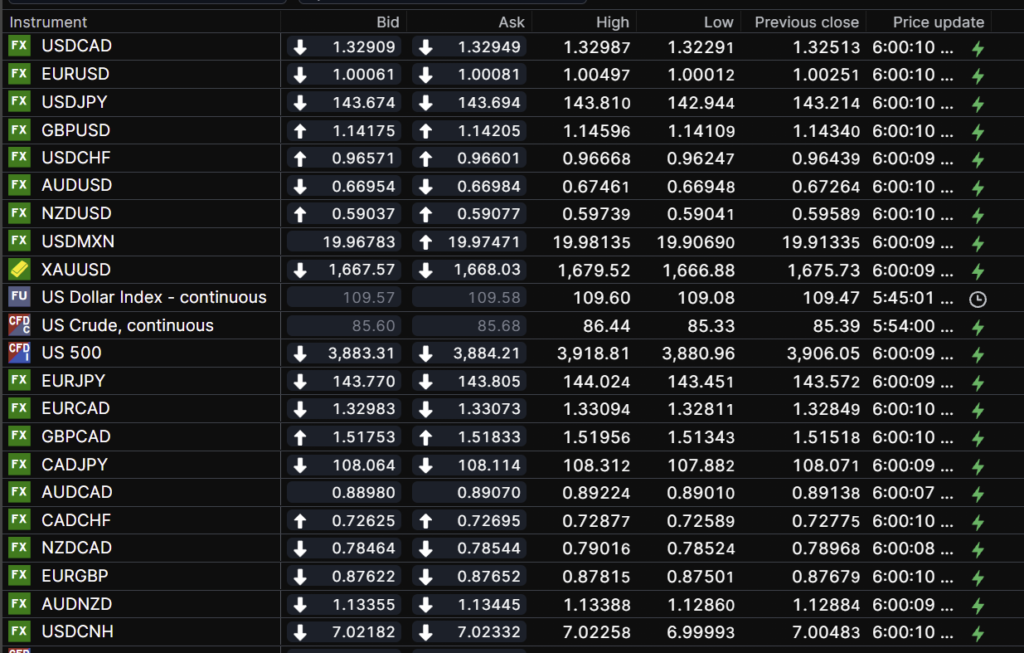

USDCAD Snapshot: open 1.3291-95, overnight range 1.32229-1.3313, close 1.3251

USDCAD had a choppy overnight session, extending Monday’s losses early in the Asian session, then consolidating in a 1.3230-1.3260 range until mid-morning in Europe. USDCAD then surged to 1.3299, coinciding with S&P 500 futures erasing all its overnights and falling into losing territory. Prices climbed to 1.3313 following the Canadian inflation data.

The price action is merely noise ahead of Wednesday afternoon’s FOMC decision.

Statistics Canada reports that “Canada CPI rose 7.0% on a year-over-year basis, down from a 7.6% gain in July. This was the second consecutive slowdown in the year-over-year price growth and was largely driven by lower gasoline prices in August compared with July. On a monthly basis, the CPI fell 0.3% in August, the largest monthly decline since the early months of the COVID-19 pandemic. On a seasonally adjusted monthly basis, the CPI was up 0.1%, the smallest gain since December 2020.”

The results may allow the BoC to raise interest rates at a slower pace, which may also boost USDCAD if the FOMC monetary policy is hawkish.

Late this afternoon, Bank of Canada Deputy Governor Paul Beaudry will entertain a University of Waterloo audience with a speech titled “Pandemic macroeconomics: What we’ve learned, and what may lie ahead.” His remarks are unlikely to have any impact on USDCAD trading.

USDCAD Technical outlook

The intraday USDCAD are bullish above 1.3230 which guards the September 13 uptrend line at 1.3205 and the mid-August uptrend line at 1.3060. A topside breach of 1.3330 will extend gains to 1.3380 then 1.3430. Fibonacci Retracement analysis suggests a move below 1.3105 (38.3% retracement of the August 11-September 19 range will extend losses to 1.2955 (61.8% level).

For today, USDCAD support is at 1.3230 and 1.3180. Resistance is at 1.3310 and 1.3370. Today’s range: 1.3210-1.3310

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

Global markets are unsettled mainly due to caution ahead of tomorrow’s FOMC meeting. Traders expect another 75 bp rate hike and a hawkish statement.

Bond Traders certainly think so. The US 10-year Treasury yield has surged to 3.539% today from 3.42% Monday.

That action knocked Wall Street lower yesterday, with S&P 500 futures extending losses overnight.

The Australian ASX 200 closed 1.29% higher after RBA minutes confirmed dovish guidance, and Japan’s Nikkei 225 rose 0.44%. European bourses are trading lower due to German PPI data and a rate hike in Sweden.

Sweden’s Riksbank surprised markets with a 100 bp rate hike, which took the benchmark policy rate to 1.75% from 0.75%. Policymakers expect rates to rise to 2.5% in 2023 and stay there until the third quarter of 2025.

EURUSD traded in a 1.0001-1.0050 range, rallying in Asia and then retreating in Europe. The rally was halted after the German August PPI index rose 7.9% m/m, and 45.8% y/y, highlighting the impact of the Eurozone energy crisis. The Riksbank rate hike didn’t offer much in the way of support, nor did comments from ECB policymaker Madis Muller.

The Estonian Central Bank president said, “sufficiently robust and decisive” action is needed to address soaring inflation.

GBPUSD bounced in a 1.1411-1.1460 range and is trading in the middle of that range in early NY.

Expectations for a hawkish FOMC outcome cap gains. GBPUSD is seeing a bit of support from hopes that the Bank of England will aggressively hike its benchmark rate at Thursday’s monetary policy meeting.

USDJPY traded with a bid in a 142.94-144.02 range, underpinned by higher US Treasury yields. Japanese inflation rose 3.0% y/y in August but was a non-issue as the BoJ remains content to leave monetary policy unchanged.

AUDUSD traded with a negative bias in a 0.6698-0.6745 range as downside pressure was exacerbated by the release of the RBA minutes. The minutes reaffirmed policymakers desire to slow the pace of rate increases.

NZDUSD fell from 0.5974 to 0.5908 due to broad US dollar strength and AUDNZD demand. AUDNZD surged to a six-year peak reaching 1.1334 in NY, partly because Australia’s current account surplus is widening while New Zealand’s current account is posting a deficit.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

China Snapshot

Today’s Bank of China Fix: 6.9468, previous 6.9396

Shanghai Shenzhen CSI 300 rose 0.12% to 3,932.84

PboC levees 1 and 5 year Loan Prime Rate unchanged, as expected

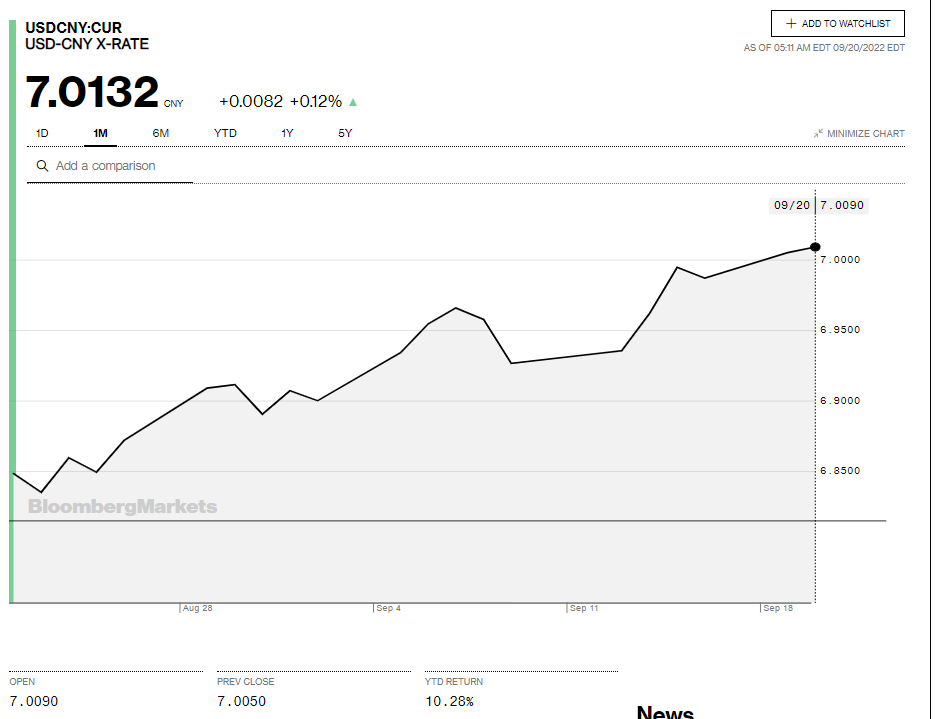

.Chart: USDCNY 1 month

Source: Bloomberg