Picture: Needpix.com

October 23, 2020

USDCAD open (6:00 am ET) 1.3111-15, Overnight Range 1.3111-1.3156

- Composite PMI data suggests Eurozone flirting with recession

- Trump/Biden debate a yawner for markets (and viewers)

- Brexit trade talks continue

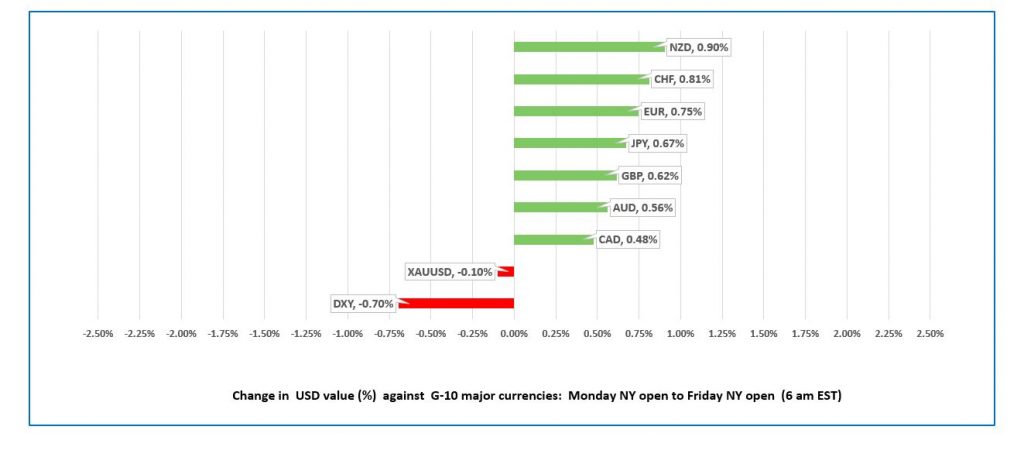

FX Ranges at a Glance -Monday open to Friday open

Source: IFXA Ltd/RP

FX Recap and Outlook: The US dollar is poised to finish the week on a losing note. NZD led the G-10 major higher, rising 0.90%, while CAD came last with a 0.48% gain.

The Trump/Biden debate did not provide much entertainment for markets, and probably viewers for that matter, as the moderator had a mute button. FiveThirtyEight polls show Biden with a six or seven-point lead. On October 23, 2016, Hillary had a 12 point lead.

Asia equity markets closed on a mixed note. Japan’s Nikkei 225 and the Hong Kong Hang Seng finished higher while China’s Shanghai Shenzhen CSI 300 closed down 1.25%. European bourses are in the green except for the UK FTSE100, and US equity futures point to a positive open on Wall Street.

The US reported a record 73,686 new coronavirus cases yesterday, and new cases continue to rise in Europe and the UK. FX markets have COVID-19 fatigue, as it was a mild risk-on environment overnight.

EURUSD was steady in Asia and perky in Europe, rising from an overnight low of 1.1788 to 1.1853.

Trader’s cherry-picked PMI data, ignoring soft Euro-area Composite, and Services PMI in favour of higher Manufacturing PMI. Weak German Services PMI was more than offset by better than expected Composite and Manufacturing data. The intraday EURUSD technicals are bullish above 1.1805, looking for a break above 1.1880 to extend gains to 1.1940.

GBPUSD was steady. GBPUSD rallied from 1.2914 on Monday to 1.3177 Wednesday, and traders were content to consolidate those gains in a 1.3052-1.3112 range overnight. Trader’s are awaiting fresh developments from the ongoing EU/UK Brexit talks and were content to ignore robust September Retail Sales data.

USDJPY dropped from 104.93 to 104.56, in part because of bearish technicals after the currency pair failed to break above 105.00 yesterday. USDJPY suffered from broad US dollar weakness. CPI slipped to 0% y/y from 0.2% y/y in August.

AUDUSD and NZDUSD held on to this week’s gains. Traders appeared to have come to terms with the dovish bias of both the RBA and RBNZ and were content to sell US dollars along with the other majors. Better than expected Australia PMI data underpinned AUDUSD.

USDCAD finally joined in the broad US dollar retreat. Its performance lagged that of AUDUSD and NZDUSD, which is a tad surprising as the RBA and RBNZ are actively hinting at negative interest rates in the near future.

Negative rates are on the Bank of Canada’s agenda (yet), but we will learn more at next week’s BoC monetary policy meeting.

The Canadian economic calendar is bare, and the US data will be ignored.

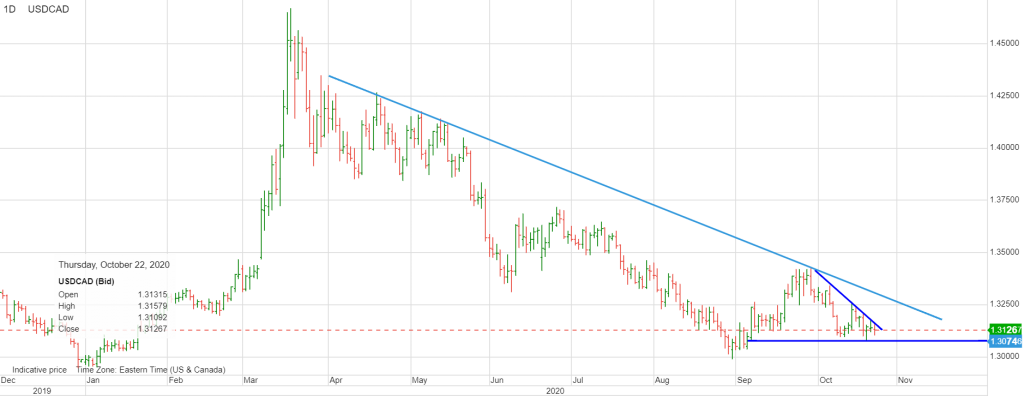

USDCAD Technicals: The intraday technicals are bearish. The downtrend line from April is intact while prices are below 1.3320. That level is guarded by resistance at 1.3180 representing another downtrend from the end of September. For today, USDCAD support is at 1.3110 and 1.3080. Resistance is at 1.3170 and 1.3220. Today’s Range 1.3080-1.3170

Chart: USDCAD daily

Source: Saxo Bank

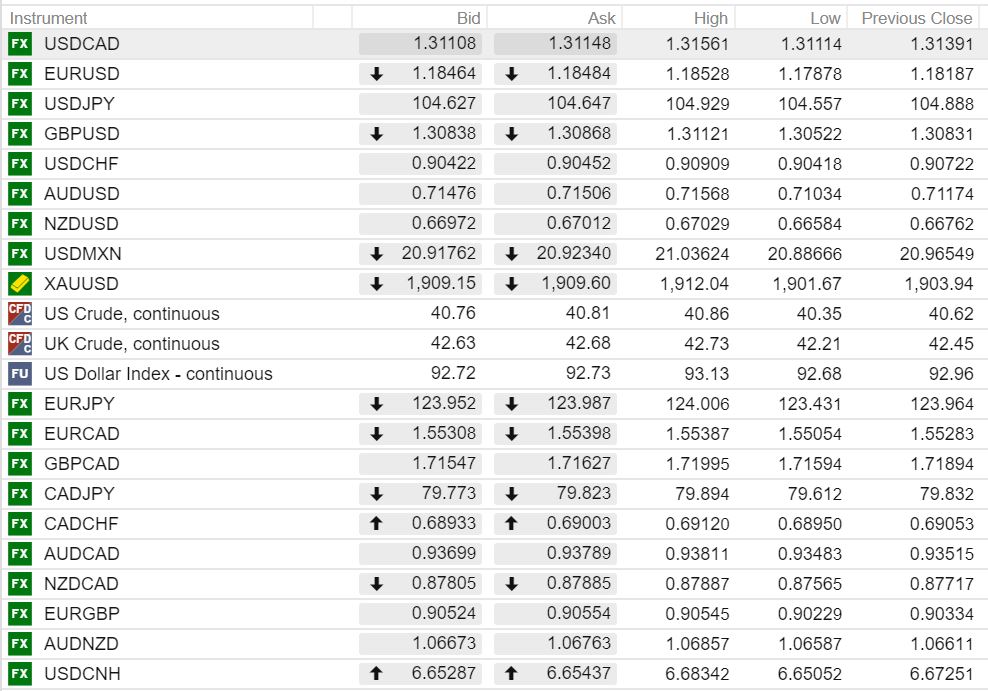

FX open (6:00 am EDT) High, Low, and previous close

Source: Saxo Bank