Photo: Hasboro

February 28, 2023

- Canada Q4 GDP growth stalls in Q4 and misses expectations.

- GBPUSD adds to gains from EU/UK Brexit deal

- US dollar lower YTD, except vs JPY and NZD

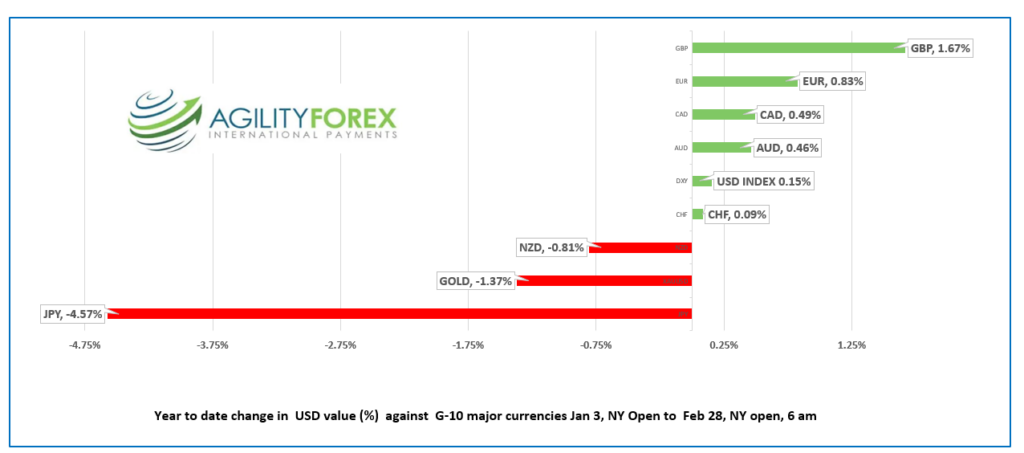

FX at a glance- Year to date

Source: IFXA Ltd/RP

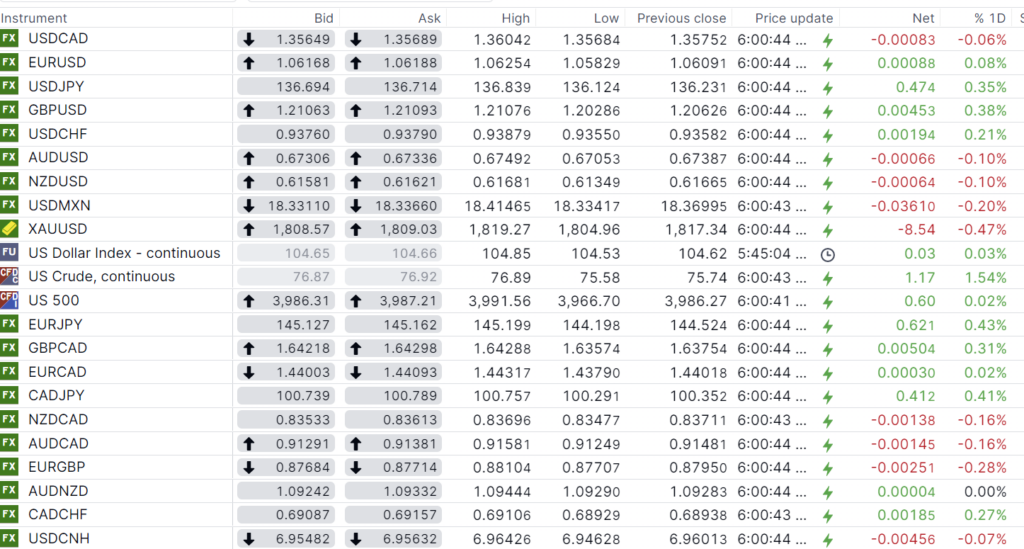

USDCAD Snapshot: open 1.3565-69, overnight range 1.3563-1.3604, close 1.3575

USDCAD attempts to break resistance in the 1.3680-1.3700 zone failed alongside fading risk aversion concerns. Earlier fears of escalating geopolitical tensions stemming from China’s support for Russia have eased or are at least being ignored. In addition, bond traders appear reluctant to drive the US 10-year Treasury yield above 4.00%, which helps to put a floor under the S&P 500.

USDCAD popped from 1.3565 to 1.3585 after Q4 GDP returned mixed results. December GDP fell 0.1% m/m (forecast 0, previous 0.1% m/m), while the quarter over quarter results were a tad better (actual 0% q/q vs forecast -0.2% q/q). On an annualized basis, Q4 GDP was 0% y/y (forecast 1.5%, previous 2.3% y/y).

The reality is that the data is just a bunch of numbers confirming what all Canadians know, and that is economic growth has slowed largely due to the aggressive Bank of Canada rate hikes.

Traders are looking ahead to the US ISM manufacturing data tomorrow and Friday’s nonfarm payrolls report.

WTI oil prices are rangebound inside a $73.00-$80.00 range. Traders expect Russian sanctions to limit the downside and are patiently awaiting a surge in demand from China, which hasn’t happened yet.

USDCAD Technical Outlook

The intraday USDCAD technicals flipped to bearish with the break below the two-week uptrend line at 1.3580, which sets the stager for further losses to 1.3510 then 1.3420. A move above 1.3630 shifts the focus to 1.3700.

The uptrend line from June 2022 remains intact while prices are above 1.3280.

For today, USDCAD support is at 1.3540 and 1.3510. Resistance is at 1.3630 and 1.3660.

Today’s range 1.3550-1.3630.

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

The first two months of 2023 are in the history books (or soon will be) and traders have the same concerns today that they did on January 3. How high will US interest rates rise? Will the Fed cut rates before the end of the year? How long will the war in Ukraine last? Will it escalate? Will the ECB hike rates as aggressively as the Fed? Is this the Last of Us?

Analysts and economists expect the US dollar to retreat in 2023 as US interest rates peak and the major G-10 central banks continue to raise rates. So far, the retreat has been tepid except against the JPY which has lost 4.57%. Part of the reason is that traders may have under-estimated the Fed’s resolve to drive inflation to 2.0%.

US Treasury Secretary Janet Yellen joins the parade of senior politicians and bureaucrats making the trek to Ukraine. She came bearing a gift of $1.25 billion.

Yesterday’s mixed US data, geopolitics and today’s month end portfolio rebalancing flows trapped FX markets in narrow ranges and led to indecisive price action in equity markets.

Asian equity closed with modest gains while European bourses are slightly higher. S&P 500 futures continue to flit either side of unchanged.

EURUSD is at the peak of its 1.0583-1.0638 band, underpinned by firm Spanish and French inflation data. The intraday EURUSD technicals are bullish above 1.0570, looking for further gains to 1.0640. A decisive break above 1.0640 targets 1.0800.

GBPUSD is feeling rather perky following the positive reception to the latest EU/UK Northern Ireland Protocol deal. GBPUSD climbed from 1.2029 to 1.2132. The gains may be fleeting due to the UK’s track record of reneging on EU deals.

USDJPY jumped to 136.90 in NY from an Asia low of 136.12, but eased back to 136.66 despite the US 10-year Treasury yield holding steady at 3.94%. Traders are back-tracking from their view that the BoJ will tighten in the near future after a series of dovish comments from the BoJ Governor and Deputy governor nomination hearings.

AUDUSD is at the top of its 0.6705-0.6749 range. Prices are supported by Australian Retail Sales which were stronger than forecast, rising 1.9% m/m vs the forecast of a 1.5% decline.

Today’s US data includes the Richmond Fed Manufacturing Index, US Consumer Confidence, and the Chicago Fed PMI index.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

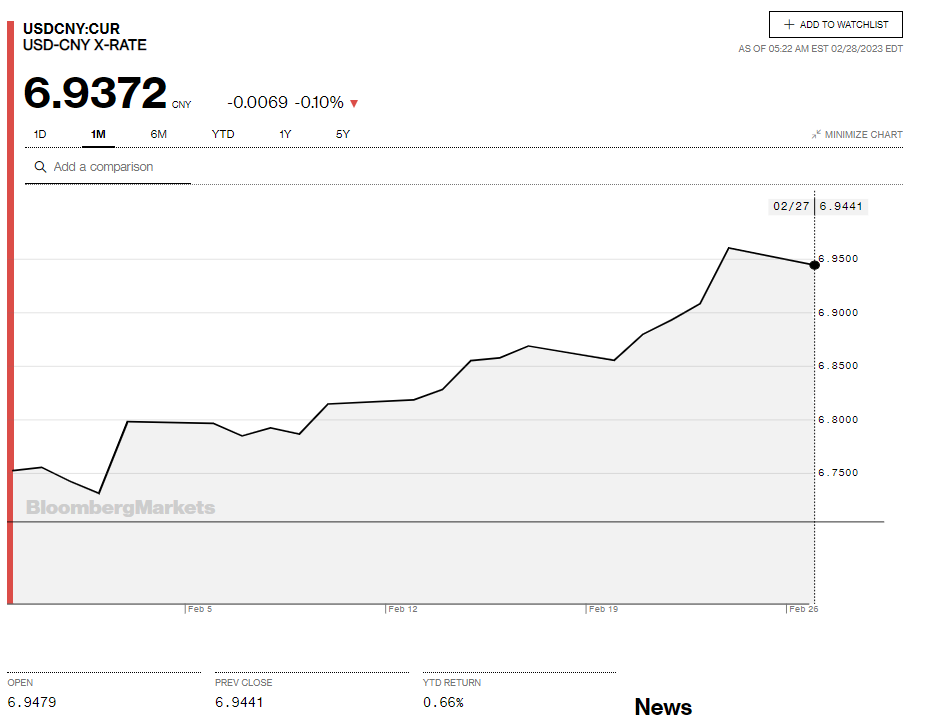

China Snapshot

Bank of China Fix: 6.9519, Previous: 6.9572

Shanghai Shenzhen CSI 300 rose 0.63% to 4069.46.

Chart: USDCNY 1 month

Source: Bloomberg