Photo: HDclipart.com

- Big week for US corporate earnings reports

- German IFO data suggest Germany is already in a recession

- US dollar retreats as equity indexes rise and Treasury yields slide.

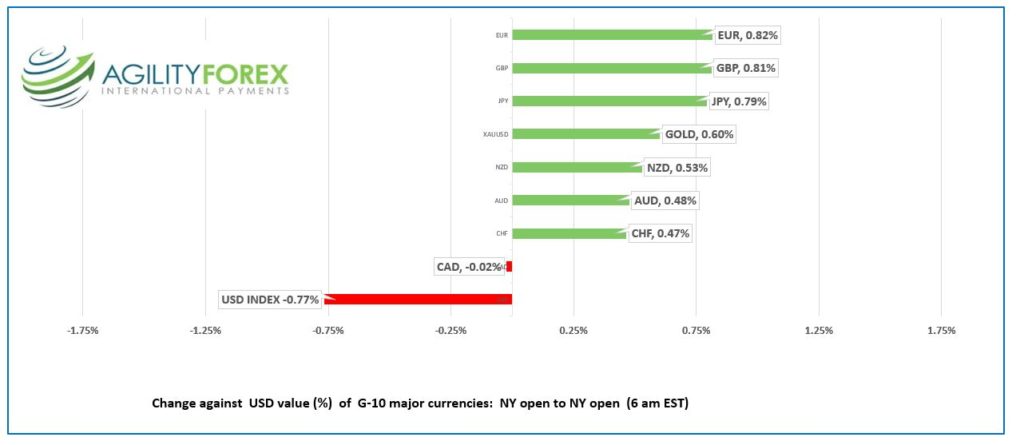

FX at a glance:

Source: IFXA Ltd/RP

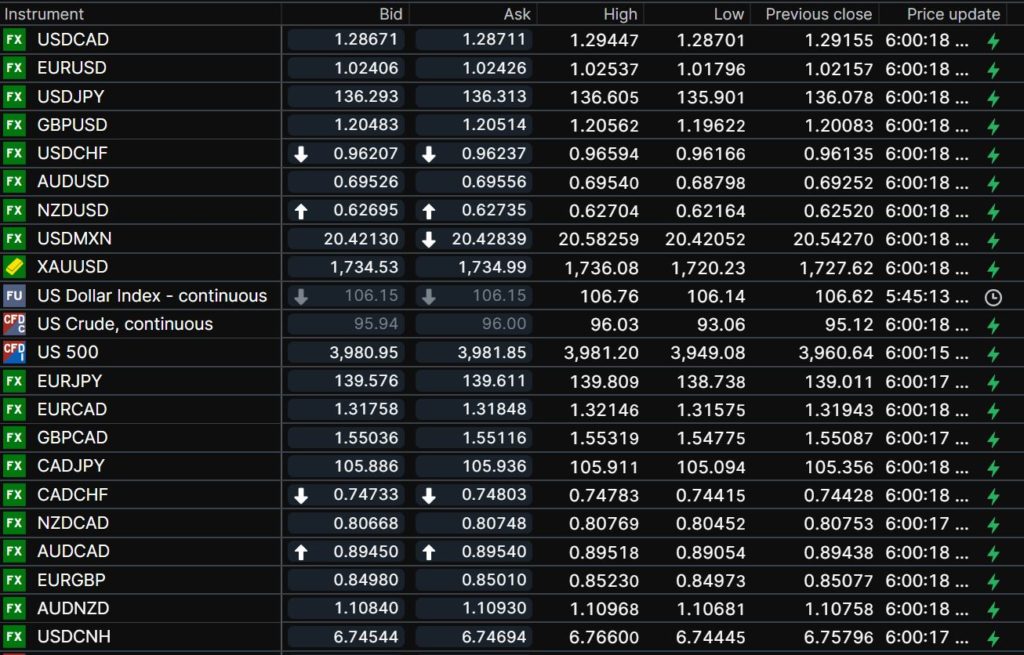

USDCAD Snapshot: open 1.2868-71, overnight range 1.2851-1.2945, close 1.2916

USDCAD is a follower, not a leader. It climbed in Asia, the dropped from the European open and continued to slide in early NY trading, reaching the bottom after Chicago Fed National Activity Index was weaker than expected.

USDCAD direction is determined by the consensus view of anticipated Fed actions. Policymakers stomped all over speculation of a 1.0% rate hike earlier this month and the debate is whether US rates rise 0.75% or just 0.50%. JPMorgan economists suggest that US rates will peak by year while Morgan Stanley thinks inflation will keep the Fed hiking a lot longer.

WTI oil dropped to $93.06/barrel in Europe then rallied to $96.03/b before easing to $95.82 in NY. Oil prices are depressed due to fears slowing economic growth in China will reduce demand.

USDCAD technical outlook

USDCAD technicals are neutral inside the 1.2820-1.3150 range that has contained price action since June 13. The intraday technicals are bearish below 1.2950, looking for a break below 1.2820 to extend losses to 1.2680. A move above 1.2950 shifts the focus to 1.3050. Meanwhile the uptrend line from April 2021 is intact above 1.2540.

For today, USDCAD support is at 1.2840 and 1.2810. Resistance is at 1.2910 and 1.2940. Today’s Range 1.2840-1.2910

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

The week started with a mild risk positive tone. European equity indexes and S&P 500 futures are higher, the US 10-year Treasury yield is steady at 2.80%, and the chatter is that inflation may be topping while US rates peak by Christmas. It’s also the summer. Maybe senior traders, economists etc. are vacationing, leaving the “B”-Team to make the predictions.

Russian and Ukraine had a deal to open Odesa ports for grain shipments. Perhaps the Russia missile attack on the port was not aggression but merely an attempt to load the grain using missiles.

Traders are looking ahead to Wednesday’s FOMC meeting. The consensus is for a 0.75% rate hike while the debate is about whether future rate hikes will be smaller and fed funds to peak by Christmas. That view is weighing on the US dollar.

The odds for just 75 bp increased improved after the Chicago Fed National Activity Index fell 0.19%, worse than the -0.03% dip expected. However, the results were unchanged from the previous month, which the report said “points to steady economic growth.”

Asia equity markets closed lower, while European bourses are trading in positive territory, led by a 0.46% rise in the German Dax index.

It’s a big week for US earnings reports, which will keep Wall Street busy, and S&P 500 futures are 0.30% firmer in anticipation of good results. WTI oil prices are a tad higher than Friday’s closing level, and gold trades at $1730.70.

EURUSD traded in a 1.0180-1.0257 range after German Ifo Survey . Prices recovered from a post-data dip .

The IFO wrote: Sentiment in German business has cooled significantly. The ifo Business Climate Index fell to 88.6points in July, down from 92.2 points1 in June, to reach its lowest value since June 2020. Companies are expecting business to become much more difficult in the coming months. They were also less satisfied with their current situation. Higher energy prices and the threat of a gas shortage are weighing on the economy.

ECP President Christine Lagarde said the ECB would raise rates for as long as needed to bring inflation back to target. Bundesbank President Joachim Nagel said future rate hikes are data dependent. EURUSD technicals are bullish above 1.0130, looking for a break above 1.0280 to extend gains to 1.0370.

GBPUSD rallied due to improved risk sentiment rising from 1.1962to 1.2081. The gains are occurring in thin summer markets and the bounce may just be of the dead cat variety as UK recession and political uncertainty risks weigh on the currency. GBPUSD is in a downtrend below 1.2250.

USDJPY traded in a 135.90-136.60 band after touching 135.58 Friday. The gains are occurring after the 10-year Treasury yield climbed from its Friday low and is now sitting at 2.83% in NY. The BoJ minutes from the July 17 meeting are due tomorrow.

AUDUSD and NZDUSD are rallying on the back of improved risk sentiment. AUDUSD climbed from 0.6880 to 0.6964 while NZDUSD rallied to 0.6268 from 0.6216.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

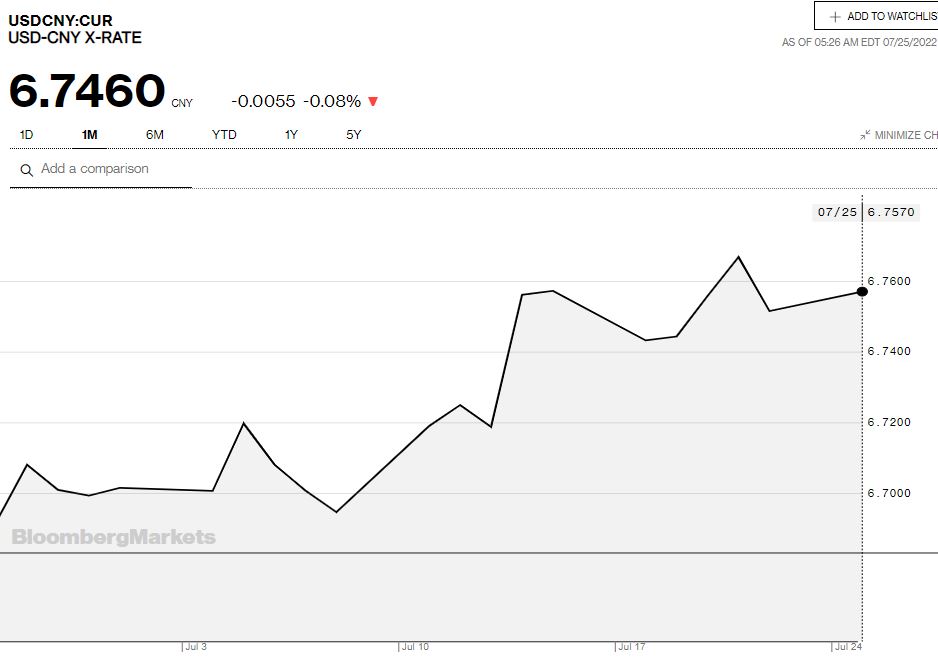

China Snapshot

Today’s Bank of China Fix 6.7543, previous 6.7522

Shanghai Shenzhen CSI 300 fell 0.60% to 4,212.64

Stocks fall due to outside economists downgrading China’s GDP growth. Goldman Sachs lowered MSCI China eps to 0 from 4.0%

China reportedly threatening military response if House Speaker Nancy Pelosi visits Taiwan

Chart: USDCNY 1 month