August 15, 2024

- US retail sales and weekly jobless mixed bag

- Many European markets closed for a holiday

- US dollar opens mixed to steady compared to Wednesday.

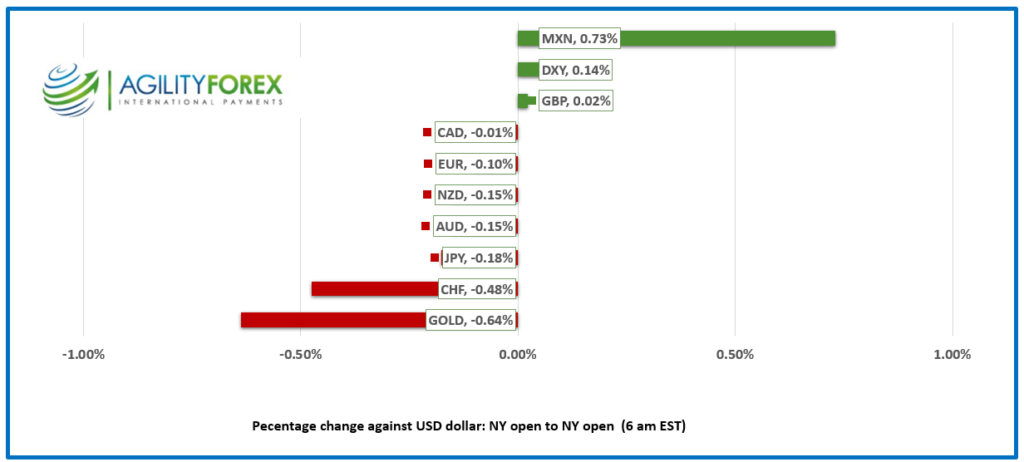

FX at a Glance

Source: IFXA/RP

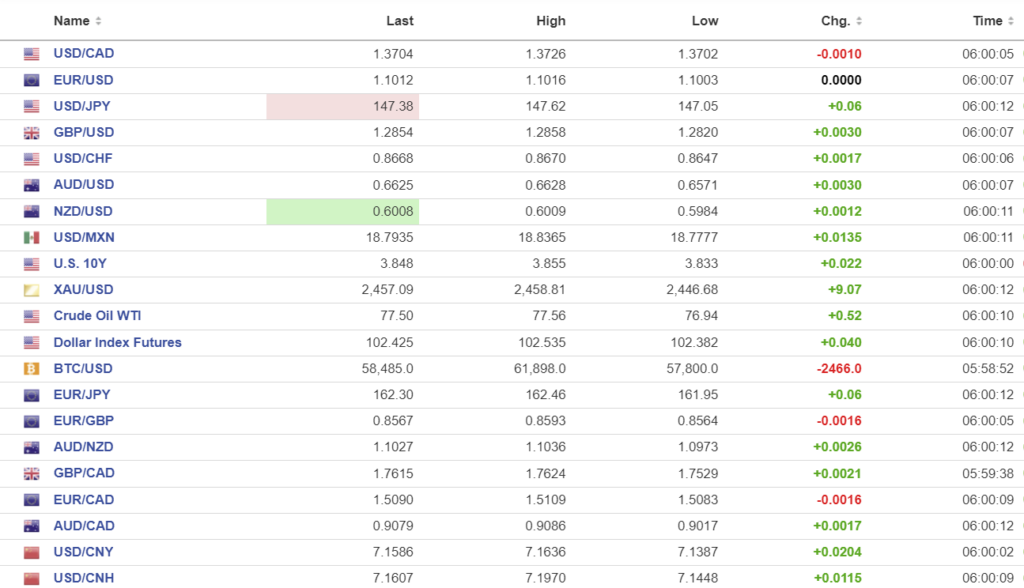

USDCAD open 1.3704, overnight range 1.3698-1.3726, previous close 1.3717

USDCAD is softer with prices tracking broad US dollar sentiment. The prospect of a Fed rate cut in September, which is almost guaranteed at this point should be fully reflected in the current rate. The selling pressure may be stemming from speculative long USDCAD positions being unwound.

Oil prices are steady with WTI trading in a 76.94-77.65 range. The risk of an oil surplus, exacerbated by slowing Chinese demand for crude has trumped concerns of a middle east supply disruption in the event Iran attacks Israel.

Canada wholesale sales dropped 0.6% in June as expected.

USDCAD Technicals

USDCAD technicals are bearish below 1.3730 and looking to chop through support in the 1.3690-00 area to set up a test of 1.3660. A break above 1.3730 suggests further 1.3700-1.3800 range trading.

Longer term, the uptrend line from the beginning of the year comes into play in the 1.3630 area and it is being guarded by the 100-day moving average at 1.3690. The 200 day moving average is at 1.3595

For today, USDCAD support is at 1.3690 and 1.3660. Resistance is at 1.3740 and 1.3770. Today’s Range 1.3680-1.3740

Chart: USDCAD 4 hour

Source: DailyFX

Will they? Won’t they? When will they? The all-consuming debate about when the Fed will finally start lowering interest rates continues unabated. Traders are so bored with the topic that many have abandoned their trading desks for holidays. Even Italians, Germans, and the French took today off in solidarity.

Data Dump

Today’s U.S. weekly jobless claims data rose by 227,000 (forecast 235,000) 7,000 less than last weeks upwardly revised result. Retail Sales rose 1.0% easily beating the forecast of 0.3%. Traders reacted by buying US dollars and boosting the US 10-year yield to 3.92% from 3.85%. The New York Empire Manufacturing Survey and the Philadelphia Fed Manufacturing Survey were both negative. The market reaction is just noise as the data will be long forgotten by the time the September FONC rolls around and the current focus is on next week’s Jackson Hole Symposium, hoping Fed Chair Powell drops a policy bombshell.

Equities

Asian equity indexes closed with gains, with Japan’s Topix rising 0.73%. European bourses are higher, except for the French CAC 40, which is flirting with the flat line. S&P 500 futures are nearly surged 0.73% after the US data and the 10-year Treasury yield rallied to 3.94% from 3.845%.

EURUSD

EURUSD is drifting in a 1.1003-1.1016 range, then dropped to 1.0962 after the US data. Traders are hoping that U.S. interest rates will drop faster than those in the Eurozone which has put a floor under the single currency. Norges Bank added fuel to that fire today by leaving rates unchanged at 4.5%, insisting that policy needs to stay restrictive to tame inflation.

GBPUSD

GBPUSD traded in a 1.2814-1.2861 range, with the low hit in Asia and the high following some robust economic data. Q2 GDP rose 0.6% q/q, while Manufacturing and Industrial Production beat expectations. Today’s data keeps the Bank of England on track for a rate cut in November, if ING analysts are to be believed.

USDJPY

USDJPY moved sideways in a 147.05-147.62 range then pooped to 148.79 post- US data after the US 10-year Treasury yield surged to 3.93 from 3.85%. Domestic data didn’t offer the yen much support either, with Industrial Production falling 4.2% m/m in June.

AUDUSD and NZDUSD

AUDUSD rallied from 0.6571 to 0.6631, supported by a stellar employment report. Australia added 58,200 jobs in July, including 60,000 full-time positions. Those numbers should keep Australian interest rates firmly elevated.

NZDUSD traded in a 0.5984-0.6012 range, with the topside capped by AUDNZD demand and lingering fallout from yesterday’s RNBZ rate cut.

USDMXN

USDMXN consolidated Wednesday’s losses in an 18.7777-18.8390 range overnight then dropped to 18.7268 after the US data.

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1399 vs exp. 7.1461 (prev. 7.1415).

Shanghai Shenzhen CSI 300 rose 0.99% to 3341.95

July Industrial Production (actual 5.1% vs forecast 5.2%, previous 5.3%). Retail Sales 2.7%, forecast 2.6%, previous 2.0%

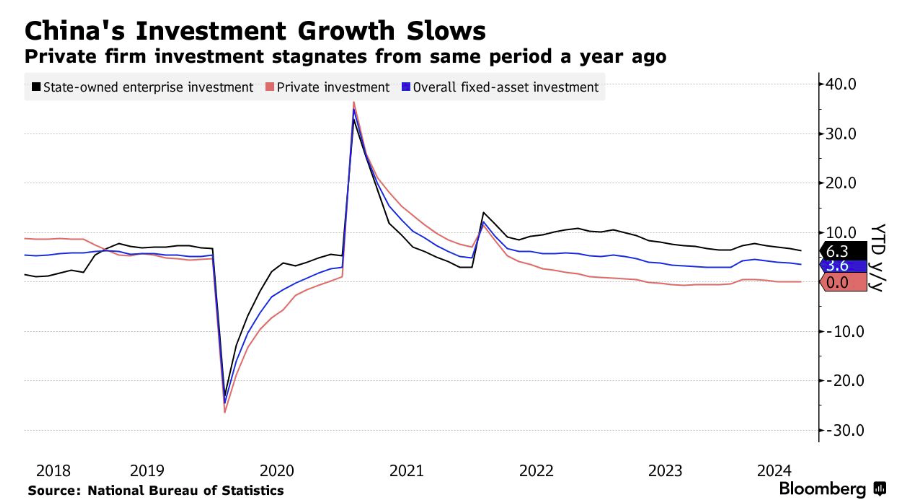

The Chinese data suggests the domestic economy continues to weaken and needs further fiscal stimulus. The rise in Retail Sales was due to seasonal factors and fixed asset investment continues to slow.

Source: Bloomberg.

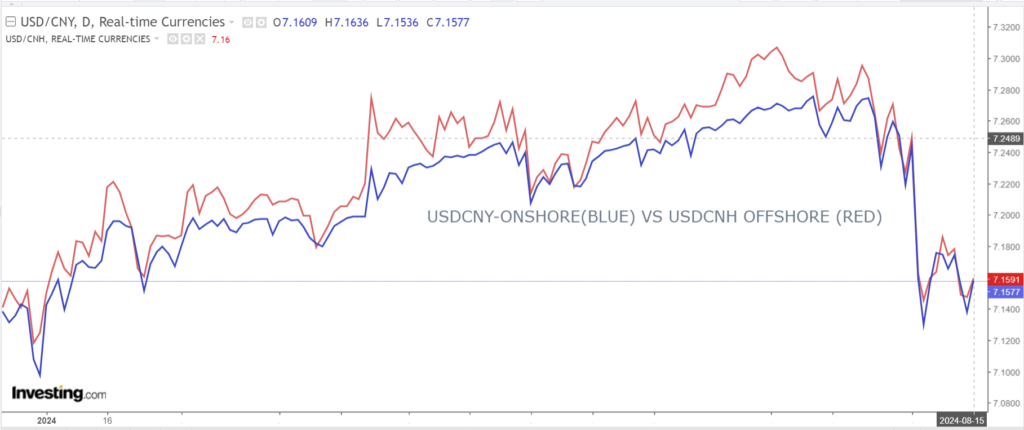

Chart: USDCNY and USDCNH

Source: Investing.com