February 22, 2024

- Hot weekly jobless claims report gives US dollar support.

- FOMC minutes highlight policymaker apprehension.

- US dollar gives back some of its overnight gains, post data.

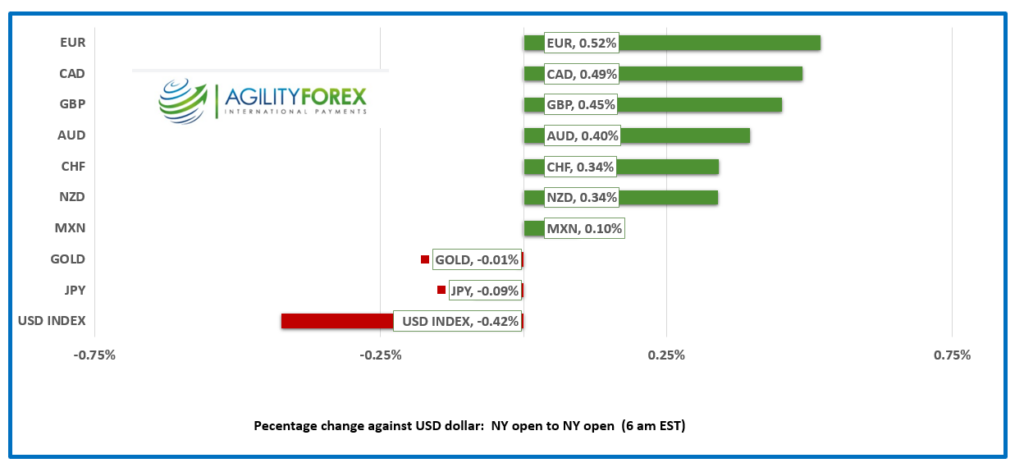

Source: IFXA/RP

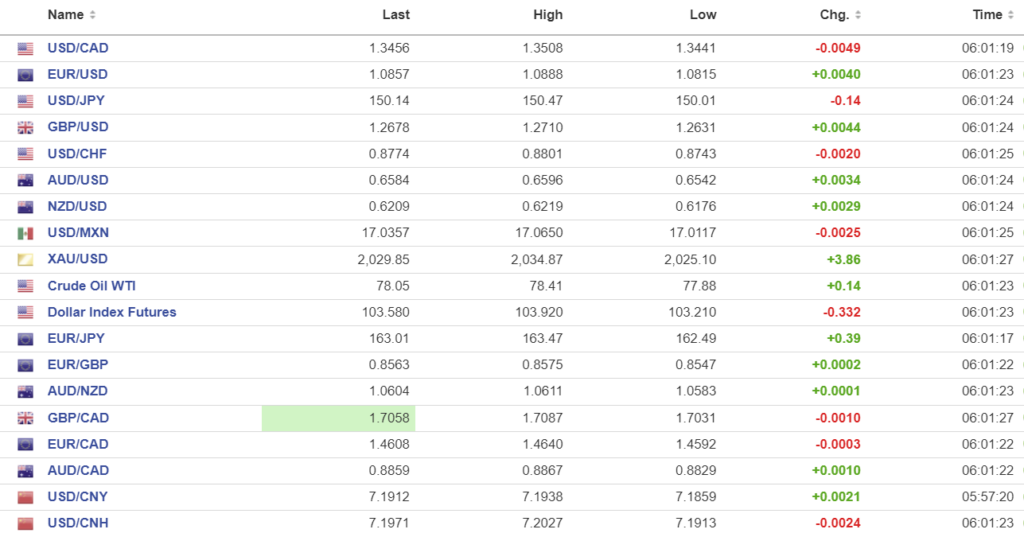

USDCAD Snapshot: open 1.3454-58, overnight range 1.3441-1.3508, close 1.3504.

USDCAD retreated on the back of broad-based US dollar selling due to a sharp improvement in risk sentiment. That changed after the weekly US jobless claims data was hotter than expected. Claims fell 11,000 to 201,000 for the week ending February 16.

Canada December Retail Sales were a non event with the results close to expectations. (Actual 0.9% vs forecast 0.8%, ex-autos actual 0.6% vs forecast 0.7%). The results are old news and won’t have much impact on the BoC monetary policy meeting on March 6.

Oil prices traded lower in a $77.59- $78.41/b range overnight. The API weekly oil inventory data showed a 7.16 million barrel increase in US stocks which put a damper on gains.

USDCAD Technicals

The USDCAD technicals turned bearish with the move below the January uptrend line at 1.3470. That sets the stage for further losses to 1.3360. A bounce above 1.3540 would negate the downside pressure. Fibonacci retracement analysis of the January February range suggests there is support at 1.3430 (38.2% Fibonacci level).

For today, USDCAD support is at 1.3440 and 1.3380. Resistance is at 1.3510 and 1.3540. Today’s range is 1.3440-1.3520

Chart: USDCAD 4 hour

Source: Investing.com

G-10 FX recap

The FOMC have reimagined a Clash tune and are singing “Should I stay, or should I cut?” The FOMC caught a lot of flak for delaying its response to rising inflation after the pandemic, and now they are afraid to react to falling inflation in case they are wrong again. The data-dependent Fed does not trust the data. “Participants generally noted that they did not expect it would be appropriate to reduce the target range for the federal funds rate until they had gained greater confidence that inflation was moving sustainably toward 2 percent.”

The minutes did not have much of an impact on trading, but Nvidia’s quarterly earnings sure did. The graphics processing, semiconductor manufacturing company turned AI vanguard reported profits of about $12.3 billion in the three months ending January 28, a massive gain compared to the $1.2 billion earned a year earlier. Its stock soared over 9.0% in after-hours trading and sparked equity index gains around the world.

Asian equity indexes closed with gains led by a 2.19% rally in Japan’s Nikkei 225 index. A 1.42% gain in the German Dax index is leading European bourses higher, and SP 500 futures are up 1.28%.

EURUSD rallied from 1.0815 to 1.0888 after the release of February PMI data, which suggests there is some hope that the Eurozone economy may be attempting to recover. An economist at Hamburg Commercial Bank wrote, “The latest HCOB PMI figures are likely to disappoint the ECB. Output prices have increased at a faster pace for the fourth month in a row. This is entirely due to the labour-intensive services sector, which continues to struggle with rising wages.”

GBPUSD churned inside a 1.2631-1.2710 range and is sitting at 1.2670 in early NY. Today’s UK PMI data has something for hawks and doves. Services PMI was unchanged at 54.3, Manufacturing PMI was 47.1, a tick better than the 47.0 in January, while Composite PMI came in at 48.9 (January 47.9). The Chief Business Economist wrote, “With growth accelerating and prices on the rise again, February’s data mean policymakers are increasingly likely to err on the side of caution when considering the appropriateness of cutting interest rates.”

USDJPY was steady in a 150.01-150.47 range and failed to participate in the latest risk-seeking US dollar sell-off. The jump in the US 10-year Treasury yield from 4.256% to 4.323% at yesterday’s close seemed to carry more weight than the news that the Nikkei 225 index broke above its 1989 peak. Japan is closed tomorrow.

AUDUSD rallied yesterday afternoon and extended gains in a 0.6542-0.6596 range overnight. The gains were supported by rebounding Chinese stock markets and an improved risk sentiment tone. The intraday technicals are bullish, but 200-day moving average resistance at 0.6590 may slow gains.

USDMXN traded with a bit of a bid in a 17.0117-17.0650 range with today’s data having little impact so far. Mexican Q4 GDP rose 0.1% q/q as expected (previous 1.1% in Q3), but the year-over-year number (at 2.5%) topped the forecast of 2.4% but is still well below the 3.3% seen previously. The good news is that first-half month inflation fell 0.1% (forecast + 0.15% and previous 0.49%), while first-half month Core inflation was 0.24% (forecast 0.28%, previous 0.25%)

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

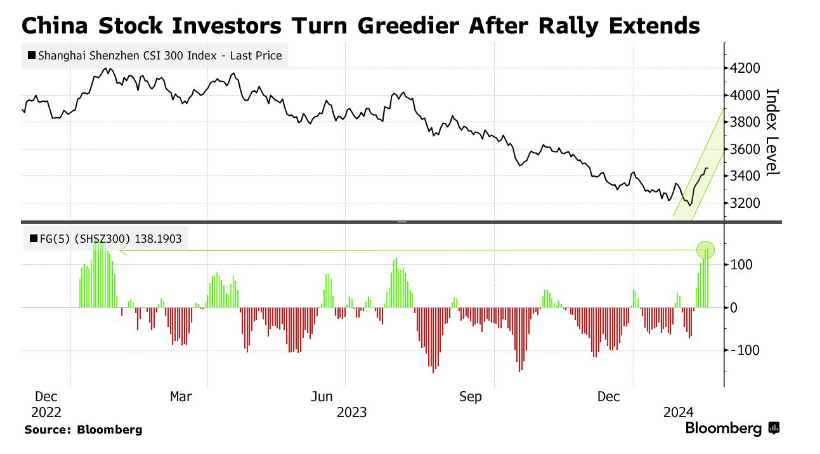

China Snapshot

PBoC fix: closed 7.1018, expected 7.1854, Monday 7.1030

Shanghai Shenzhen CSI 300 rose 0.86% to 3486.67.

China’s so-called Fear and Greed index jumped to it highest level since January due to government stimulus measures, a increased supervision of short selling by quant funds and a ban on selling equities at market open or market close.

Source: Bloomberg

Chart: USDCNY daily and USDCNH

Source: Bloomberg