Source: HDClipart.com

- Markets still reeling from Fed policymakers rate hike views

- US weekly jobless claims improve

- US dollar continues to grind higher

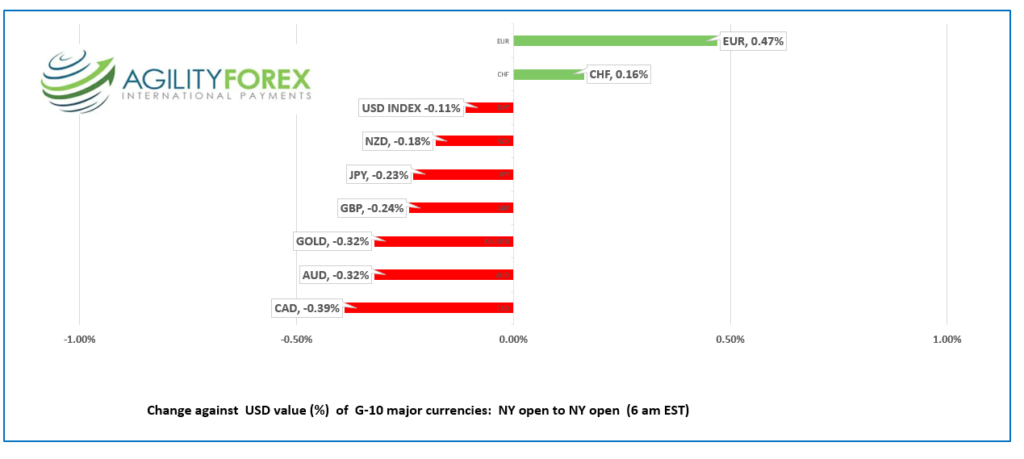

FX at a glance:

Source: IFXA Ltd/RP

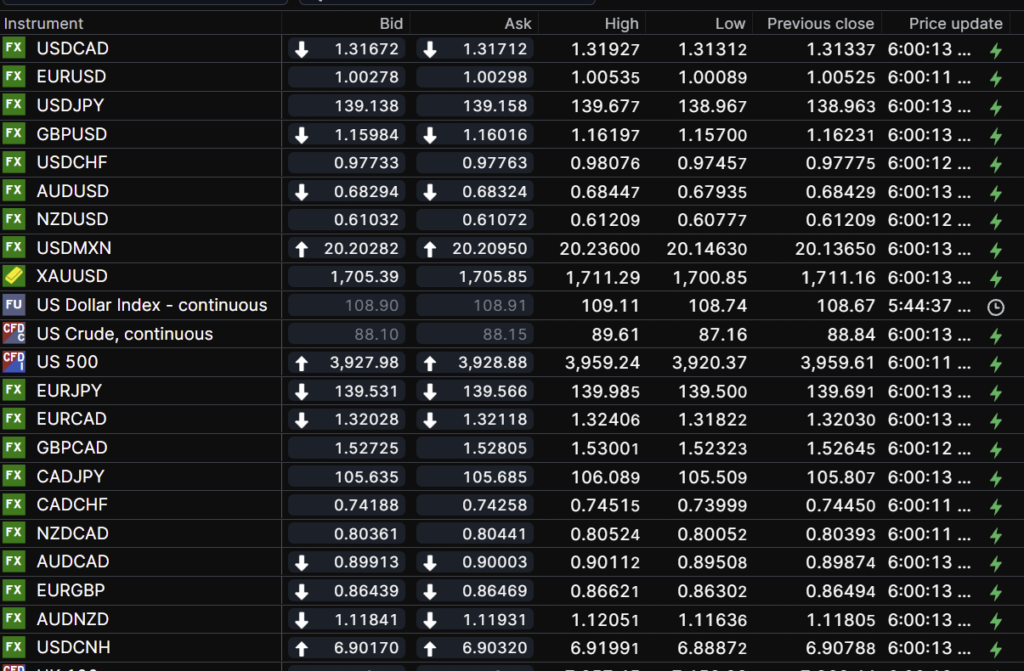

USDCAD Snapshot: open 1.3167-71, overnight range 1.3131-1.3193, close 1.3134

USDCAD rallied hard yesterday and extended the gains overnight despite a rather robust GDP report that gives the Bank of Canada plenty of room to hike interest rates aggressively. The gain was largely due from the lingering impact from re-opening the economy following the pandemic.

Plunging oil prices also underpinned USDCAD. WTI oil continued to slide overnight, falling from $89.61/b to $87.16/b in NY. Prices are suffering from recession fears, and concerns about increased supply following an Iran nuclear deal. However, losses should be limited as Opec is predicting a smaller supply surplus in 2022 and a deficit in 2023. Bollinger bands and RSI’s suggest USDCAD is overbought, on a daily chart.

As usual, USDCAD will move in tandem with S&P 500 moves.

USDCAD Technical outlook

USDCAD moved into a new trading band (1.3000-1.3400) with the decisive breach of resistance at 1.3030 and 1.3070, which should revert to support. The intraday technicals are bullish above 1.3140, looking for a move to 1.3225 then 1.3310.

Keep in mind, that the FX market is still in summer-holiday-mode, and liquidity is poor, which exaggerates prices swings. USDCAD needs to spend a few days above 1.3070 to confirm the upside break. A break below 1.3140 targets 1.3110 then 1.3070.

For today, USDCAD support is at 1.3140 and 1.3110. Resistance is at 1.3190 and 1.3225. Today’s range: 1.3110-1.3190

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

September has arrived, but deeper market liquidity is still missing in action until after Labour Day (Sep. 5). Month-end volatility has waned, but there is still lingering US dollar demand.

Escalating geopolitical tensions are not helping the safe-haven Japanese yen or gold. Gold prices and the Japanese yen are sinking

For now, traders fear higher rates more than China invading Taiwan, Israel bombing Iran’s nuclear site, or Russia and Ukraine risking another Chernobyl-style event.

Taiwan reportedly shot down a Chinese Peoples Liberation Army drone that intruded into its airspace.

Beijing’s pet Global Times editor Hu Xijin wrote an article that “warned Taiwan to never shoot down drones from the mainland and that they probably belonged to civilian hobbyists but added once they’re shot down, there will be an explosion of public opinion and that the PLA is bound to retaliate against a certain target of the Taiwan side.”

There is good news and bad news around the ongoing Iran Nuclear deal. Iran is busily enriching uranium while negotiators try to revive the 2015 deal canceled by Trump. Iran wants a guarantee that future presidents wouldn’t scrap the pact. Meanwhile, Israel is vehemently opposed to Iran’s nuclear plans and has the means to disrupt them.

Global markets continue to reel after yesterday’s comments by Cleveland Fed President (and FOMC voter) Loretta Mester. She predicted fed funds would be over 4.0% in 2023 and staying there for the entire year.

Loretta Mester’s comments sent the US 10-year yield soaring, rising from 3.093% yesterday to 3.219% overnight before slipping to 3.198% in NY.

Asian equity indexes followed Wall Street lower. Australia’s ASX 200 lost 2.02% and Japan’s Nikkei 225 index fell 1.79%. European bourses opened negatively and extended losses throughout the session, led by a 1.43% decline in the UK FTSE 100. WTI oil dropped 2.1% while gold fell 0.75% from Wednesday’s close.

Better than expected weekly jobless claims (actual 232,000 vs previous revised lower result of 237,000) were ignored ahead of Friday’s US employment data.

EURUSD traded in a 1.0003-1.0054 range overnight following yesterday’s higher-than-expected Eurozone inflation data and a slew of bank forecasters predicting 50-75 bps rate hikes next week. Prices churned with a negative bias in Europe, and the single currency is sitting just above the low. Better than expected, German Retail Sales data was ignored.

GBPUSD extended Wednesday’s losses, falling from 1.1620 to 1.1551 in NY trading. The UK media is rife with a doom and gloom economic outlook, which makes sense because that’s what Bank of England officials have been saying.

UK manufacturing PMI fell to 47.3 in August compared to 52.1 in July. The report said “August saw manufacturing production suffer its steepest contraction since May 2020. Companies experienced a sharp reversal in new orders, with demand from domestic and overseas clients contracting sharply.”

USDJPY rallied into nose-bleed territory with prices climbing from 138.28 yesterday to 139.68 in Asia, before drifting down to 139.33 in NY. The ultra-dovish Bank of Japan monetary policy sharply contrasts the latest hawkish Fed outlook, which continued to fuel the rally.

AUDUSD And NZDUSD consolidated yesterday’s losses in narrow ranges, albeit with a negative bias. Both currency pairs suffered from China’s weaker than expected manufacturing PMI report.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

China Snapshot

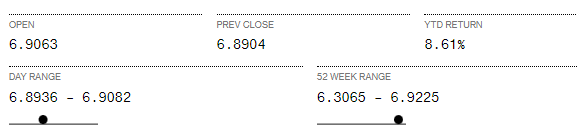

Today’s Bank of China Fix: 6.8821, previous 6.8906

Shanghai Shenzhen CSI 300 fell 0.86% to 4,043.74

Caixin August Manufacturing PMI fell to 49.5 from 50.4 in July. A reading below 50 suggests the economy is contracting.

Taiwan claims it shot down Chinese drone, China denies the event

Chengdu City (population 16.33 million) to conduct mass Covid testing Sep 1-4

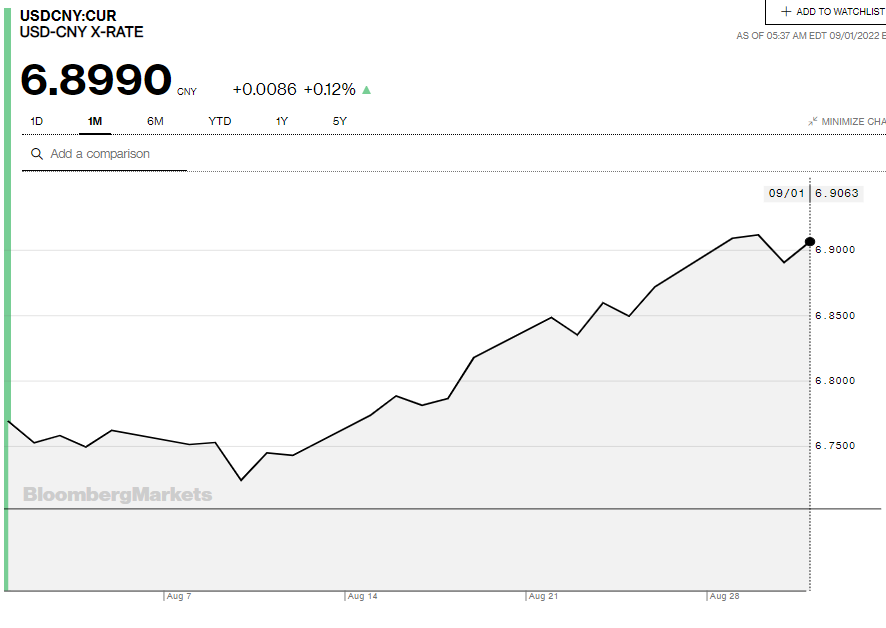

Chart: USDCNY 1 month

Source: Bloomberg