Photo: Bing AI

October 11, 2023

- Fed officials massaging interest rate expectations.

- Treasury yields drop nearly 10 bps overnight.

- USD opens on the defensive, again.

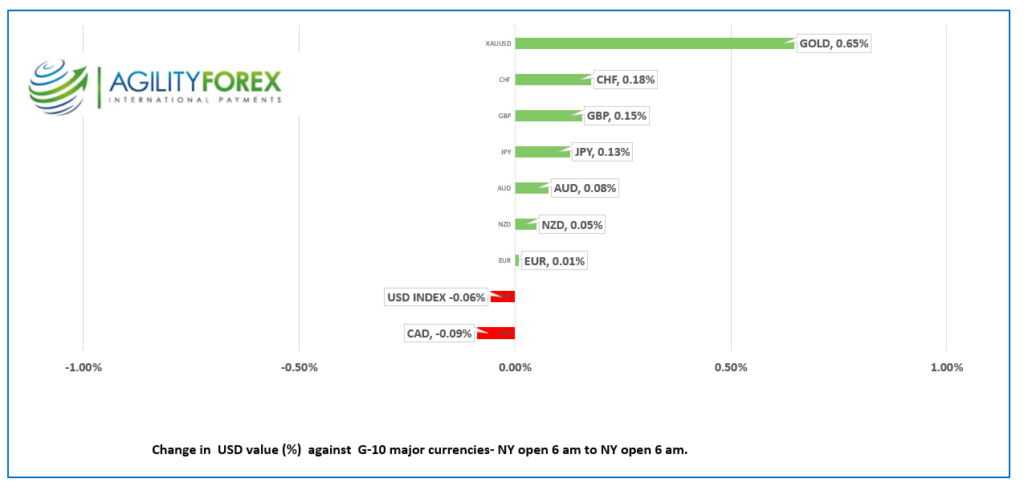

FX at a Glance

Source: IFXA/RP

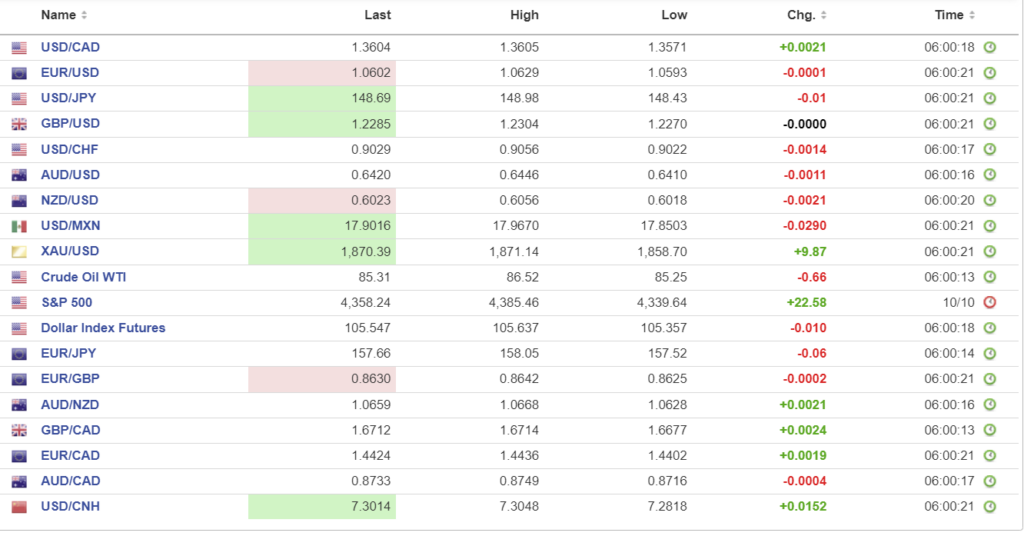

USDCAD Snapshot: open: 1.3602-06, range 1.3571-1.3605, close 1.3582

USDCAD is outside, looking in. The major G-10 currencies managed to record small gains since yesterday’s NY open, except for the Canadian dollar. USDCAD is trading modestly higher even though WTI oil prices are steady around the $85.50 /barrel area.

USDCAD direction is determined by expectations for US rates and the direction of the US dollar which means today’s US Producer Price data could create some sparks. A higher than expected reading would suggest that the inflation fight is far from over and it is premature to talk about US rates peaking.

Canadian Building Permits rose 3.4% m/m in August compared to -3.8% in July.

USDCAD Technicals

The intraday USDCAD technicals are neutral and little changed from Monday as USDCAD consolidates its recent losses. The downtrend is intact while prices are below 1.3630 looking for a break below support in the 1.3540-60 area to extend losses to 1.3490. A break above 1.3630 negates the downtrend and targets 1.3750.

Longer term, the weekly chart shows that USDCAD is in the top half of its 1.3090-1.3890 range that has contained price action since September 2022.

For today, USDCAD support is at 1.357 and 1.3540. Resistance is at 1.3630 and 1.3680. Todays Range 1.3570-1.3640

Chart: USDCAD weekly

Source: Investing.com

G-10 FX recap

Markets are more concerned about the outlook for Fed rates than they are about Hamas terrorists rampaging in and around Israel. The risk-aversion trades that drove the market direction on Monday have almost fully reversed, with traders now fixated on Fed monetary policy.

In what seems to be a coordinated effort to manage interest rate expectations, a slew of Fed officials are suggesting that higher long-term yields might reduce the need for the Fed to increase rates further.

Atlanta Fed President Raphael Bostic mentioned that rates are “sufficiently restrictive” to bring inflation to 2.0%.

San Francisco Fed President Mary Daley suggested that higher bond yields could indicate tightened financial conditions. If that’s the case, she said, “maybe the Fed doesn’t have to do as much.”

Minneapolis Fed President Neel Kashkari stated, “It’s certainly possible that higher long-term yields may do some of the work for us in terms of bringing inflation back down. But if those higher long-term yields have risen because of changed expectations about our actions, then we might need to act in line with those expectations to maintain those yields.”

The FOMC minutes from the September 20 meeting will be closely scrutinised for clues as to where policy makers see the neutral rate after the Fed’s Mary Daly suggested that the neutral rate may be 3.0% rather than 2.5%.

The dovish Fed chatter may be premature. September Producer Prices, seasonally adjusted increased 0.5% m/m which was above the 0.4% forecast but lower than the 0.7% in August. The US dollar rallied marginally on the news.

Asian equity indexes took cues from Wall Street’s positive close, finishing their session with gains across the board. Japan’s Nikkei 225 index gained 0.60%, and Australia’s ASX 200 rose by 0.66%. Meanwhile, European bourses are showing mixed reactions, hovering between flat and negative, while S&P 500 futures have increased by 0.22%. The US 10-year Treasury yield stands at 4.558%, a slight drop from 4.655% at Tuesday’s close.

Gold (XAUUSD) has continued its rally this week. Prices surged from $1810.00 on October 6 to $1874.81 in NY today, propelled by dovish Fed commentary suggesting that US rates might have peaked and by the risk-aversion sentiments following the Hamas terrorist attack. If gold breaks above $1890.00, it could target $1940.00. Conversely, a decline below $1850.00 could hint at further losses towards $1800.00.

Chart 4-hour

Source: Investing.com

EURUSD drifted in a 1.0593-1.0629 range overnight and traded at 1.0600 when NY opened. The gains were driven by broad US dollar weakness and dovish Fed-speak. Prices dropped from the peak after the ECB inflation expectations survey showed consumers were not buying what policymakers were selling. Eurozone consumers expect inflation to remain above the ECB’s 2.0% target for another three years. The August survey showed respondents increasing their inflation forecast to 2.5% from 2.4%.

GBPUSD moved within a 1.2270-1.2304 range as it consolidated recent gains, sparked by a series of dovish comments from numerous Fed officials. GBPUSD is also benefiting from improved risk sentiment after US Treasury yields fell to 3.558% overnight. However, the upside is limited ahead of Thursday’s August GDP and trade data, as well as industrial and manufacturing production reports.

USDJPY traded lower in a 148.43-148.98 range due to the 9 bp drop in the US 10-year Treasury yield to 4.566% overnight.

AUDUSD bounced within a 0.6410-0.6446 range, underpinned by improved risk sentiment and firmer commodity prices. RBA Assistant Governor Chris Kent stated that the bank is in the third phase of monetary policy, in which it assesses the impact of recent hikes.

FX high, low, open

Source: Investing.com

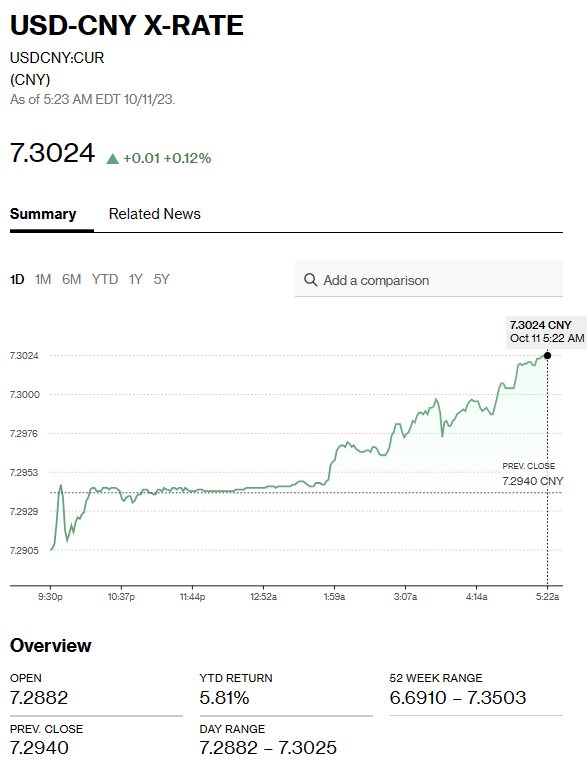

China Snapshot

Bank of China Fix: today 7.1717, expected 7.2842, previous 7.1781.

Shanghai Shenzhen CSI 300 rose 0.28% to 3667.55.

Stocks rise following Tuesday’s report that Beijing will increase its budget deficit and issuing new debt to facilitate new infrastructure spending.

Chart: USDCNY daily

Source: Bloomberg