Source: Wikimedia commons

- China eases Covid restrictions further

- Eurozone Retail Sales, Services PMI data soft

- US dollar recoups some Asia losses in Europe

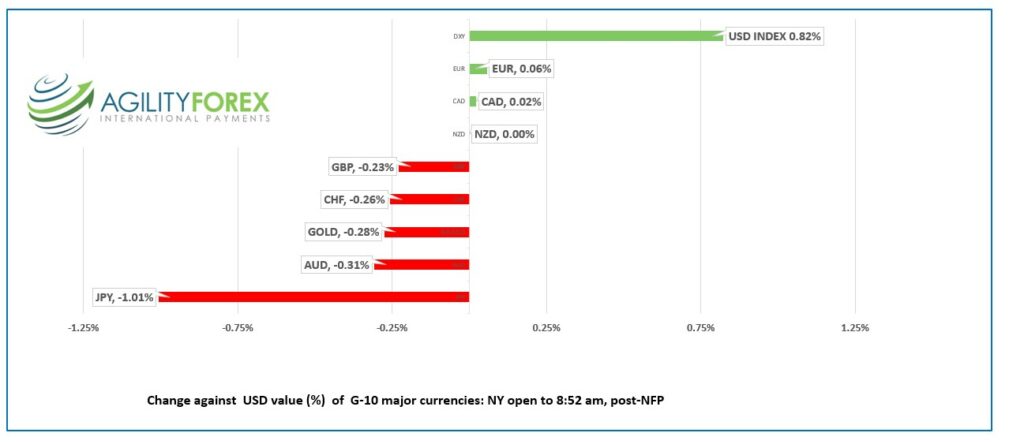

FX at a glance:

Source: IFXA Ltd/RP

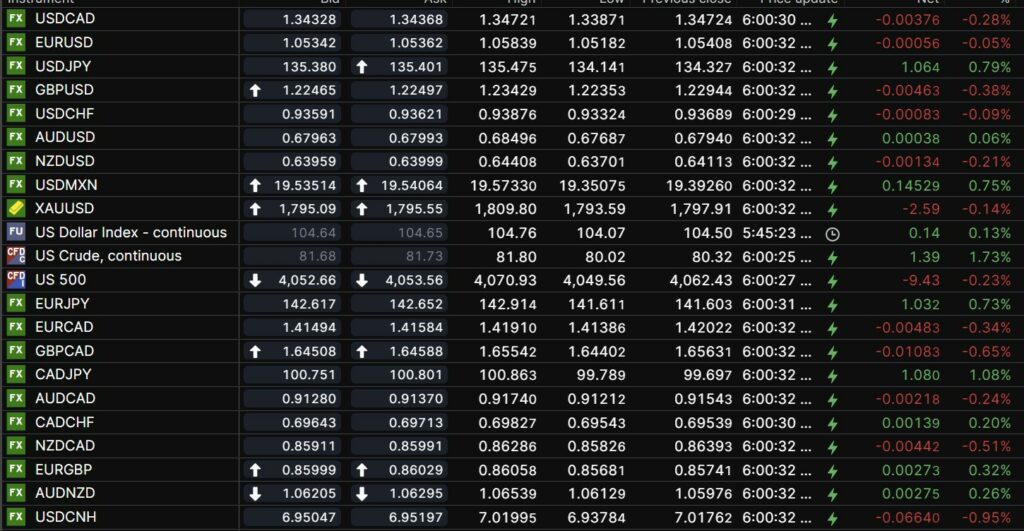

USDCAD Snapshot: open 1.3433-37, overnight range 1.3387-1.3472, close 1.3472

USDCAD opened today, exactly where it opened Friday, then fell further in early NY trading.

Friday’s Canadian employment results were better than expected but overshadowed by the US NFP results. The data didn’t do much to change the rate hike debate. BMO economists expect a 50 bp hike while RBC economists suggest a 25 bp increase is likely. CIBC is on the fence suggesting a good case can be made for either outcome.

WTI oil rose from $80.02/b to $82.36 in early NY, supported by a softer US dollar and hopes for increased demand as China accelerates easing covid restrictions. The November downtrend is intact while prices are below $82.70/b.

USDCAD direction will track broad US dollar sentiment and S&P 500 price action.

USDCAD Technical outlook

The intraday USDCAD technicals are bearish while below the downtrend line from November 29 that comes into play at 1.3460 and Friday’s fall below 1.3430. A decisive break below support in the 1.3390-1.3405 will extend losses to 1.3310.

The August uptrend line on a daily chart comes into play at 1.3310.

For today, USDCAD support is at 1.3390 and 1.3360. Resistance is at 1.3430 and 1.3460

Today’s range 1.3370-1.3440

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

Russia to G-7, “Put that in your cap and smoke it.” (the pipe was in use). The G-7 agreed to a $60/barrel cap for Russian seaborne crude on Friday and Russia responded petulantly. Deputy Prime Minister Alexander Novak said, “we will sell oil and oil products only to countries that work with us, even if we have to lower production.” Chinese and Indian crude buyers rubbed their hands in glee, while tacitly thanking the G-7 for the early Christmas present.

Opec failed to follow-up its October meeting with additional production cuts to shore up prices at the weekend meeting, partly because the cuts didn’t work. All it achieved for the cartel was less money for lower production. They must have been taking economic advice from Turkey President Recep Erdogan.

Rubber chicken circuit delegates and global markets won’t be listening to Fed officials blathering their opinions about the US interest rate outlook. It is the two-week “blackout” period for Fed officials. However, ECB officials are happy to fill the void.

Risk sentiment was positive in Asia after Chinese authorities announced they were accelerating the easing covid restrictions in many large urban areas. The news (and a falling USDCNY) powered the Hong Kong Hang Seng index to a 4.51% gain. Australia’s ASX 200 rose 0.33% while Japan’s Nikkei 225 index climbed 0.15%.

European equity traders were not as enthusiastic and the major bourses are posting small losses, except the UK FTSE which is up 0.29% (as of 6:28 am ET). S&P 500 futures are down 0.20%. The US 10-year Treasury yield is near the bottom of its 3.51%-3.544% overnight range. Gold (XAUSUD) dropped $3.10 to $1794.91.

The US dollar caught a bit of a bid in Europe after the Wall Street Journal suggested that elevated wage pressures could force the Fed to hike by more than 50 bps at next week’s meeting.

EURUSD is consolidating its post-NFP gains in a 1.0518-1.0584 range. Prices retreated from the peak after November Eurozone PMI and Retail Sales were weaker than expected. German Services PMI also disappointed forecasters, but the news shouldn’t have surprised anyone, due to the war and energy crisis. However, the downside got some support from ECB officials. Gabriel Makhlouf said rates would likely rise 50 bps in December and said policymakers “have to be open to moving rates into restrictive territory for a period.” Bank of France President Francois Villeroy also advocated for a 50 bp bump. The intraday EURUSD technicals are bullish above 1.0340.

GBPUSD traded in a 1.2267-1.2343 range overnight, rallying in Asia and retreating in Europe but well above Friday’s post-NFP low of 1.2135. UK Composite data was a tick lower than forecast while Service PMI data was as expected. The intraday GBPUSD technicals are bullish above 1.2220.

USDJPY rallied in a 134.14-135.54 range with the gains occurring following the WSJ article suggesting the possibility of a higher-than-expected Fed rate hike. Prices were also underpinned as safe-have yen trades were unwound following news China was quickening its reopening pace. However, soft Treasury yields limited the topside.

AUDUSD peaked in Asia rising from 0.6769 to 0.6850 following news that China further relaxed its covid restrictions in Shanghai and Shenzhen, then gave back more than half of those gains in Europe to open in NY at 0.6399.

The RBA is expected to announce a 25 bp rate hike tomorrow, taking the OCR rate to 3.10%.

US ISM Services PMI and Factory orders are due.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

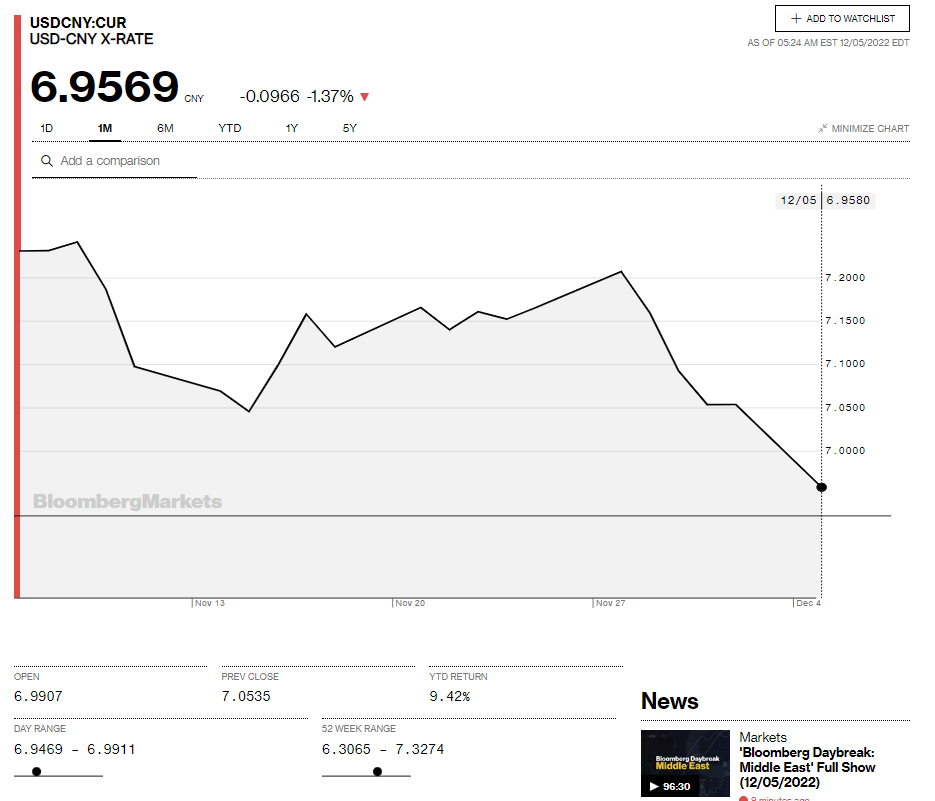

China Snapshot

Today’s Bank of China Fix: 7.0384, previous 7.0542

Shanghai Shenzhen CSI 300 rose 1.96% to 3946.88

Stocks rally after covid restrictions eased and USDCNY fall through support at 7.00

Xi Jinping visits Saudi Arabia this week

Chart: USDCNY 1 month

Source: Bloomberg