Image by DALL-E

December 14, 2023

- FOMC predicts 75 bps of rate cuts in 2024.

- US 10-year Treasury yield falls to 3.95%.

- US dollar plummets and is still looking for a bottom.

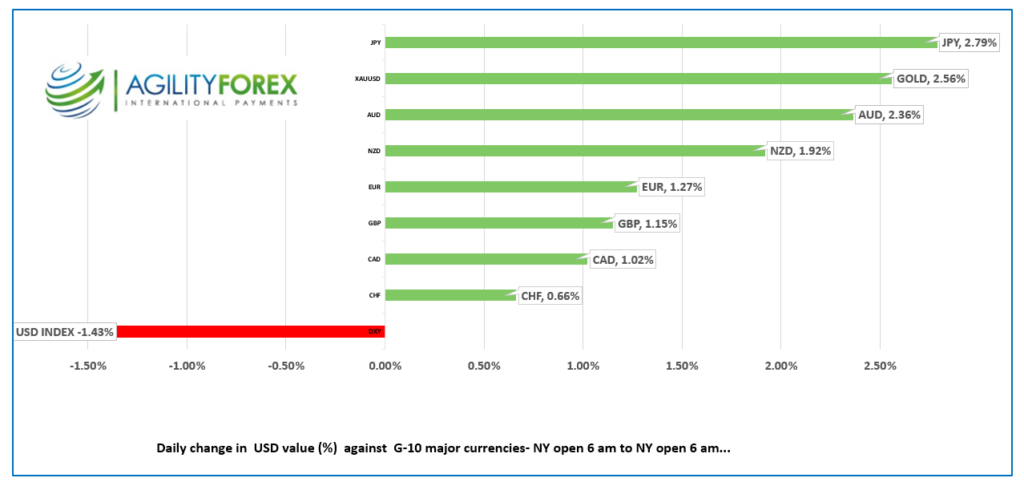

FX at a glance

Source: IFXA/RP

USDCAD Snapshot: open 1.3451-55, overnight range 1.3426-1.3521, close 1.3519

The Fed did what the Bank of Canada didn’t. The FOMC projected 75 bps of rate cuts in 2024, while BoC officials were mute on the subject. That was enough to see a 12.2 bp drop in the spread between the Canadian and US 10-year yield, which weighed on USDCAD. However, the biggest driver of USDCAD down from yesterday’s 1.3609 peak to the early NY low of 1.3449 was broad-based US dollar selling against the majors.

The soft US dollar underpinned WTI oil prices, but the gains were minor. WTI rose from $69.55/b to $70.90/b. Prices also got a lift from yesterday’s EIA weekly crude inventories data, which showed a 4.2 million barrel drop in stocks.

USDCAD trading will be dictated by the FX reaction to both the ECB and BoE rate decisions, along with the lingering fallout from the FOMC meeting. The year is rapidly approaching its finale, which means liquidity will evaporate.

Canada’s October Manufacturing Sales are expected to have fallen 2.7% m/m compared to 0.4% in September.

USDCAD Technicals:

The intraday and medium term USDCAD technicals turned bearish with the break below support at 1.3550 on an hourly chart (which has reverted to resistance) and the breach of the July uptrend line when prices moved below 1.3510, which is also the 200 day moving average. However

Longer term, USDCAD is in a downtrend channel between 1.3590 on the top and 1.3392 on the bottom.

For today, USDCAD support at 1.3410 and 1.3380. Resistance is at 1.3480 and 1.3510. Today’s range 1.3410-1.3490.

Chart: USDCAD daily

Source: Daily FX

G-10 FX recap

The Fed pivoted. Analysts and economists have been anticipating this moment since at least September, if not earlier, and based on that rationale, the market reaction is a bit of a head-scratcher. What? Did no one think a pivot would happen in December? The reaction wasn’t so much because of the dot-plot projections suggesting 75 bps in rate cuts in 2024, but because of the magnitude of the rate cuts. The September SEP had one more rate hike baked in, while yesterday’s SEP shows a 100 bp reversal (5.75-4.75%). That certainly put the ram in the rama lama ding-dong.

US Treasury yields and the US dollar plunged, Wall Street soared, and gold led a commodity market rally. The party continued overnight and into an event-laden European session. The Bank of England (BoE), Swiss National Bank (SNB), and European Central Bank (ECB) monetary policy meetings are today. Norway’s Norges Bank surprised markets with a 25 bp rate, taking the overnight rate to 4.5% due to inflation concerns. The SNB left its rates unchanged as well.

Asian equities closed mixed. Japan’s Nikkei 225 index fell 0.73% due to the sharp yen rally, while Australia’s ASX gained 1.65%. European bourses are all posting meaningful gains, led by a 2.24% jump in the UK FTSE 100 index. S&P 500 futures are a little tame, rising just 0.24%. The US 10-year Treasury yield dropped to 3.95% after closing at 4.026% yesterday.

EURUSD traded firmer in a 1.0872-1.0940 range, adding to yesterday’s post-FOMC rally. Prices inched lower following the ECB Statement that it would leave interest rates unchanged. The statement noted, “Based on its current assessment, the Governing Council considers that the key ECB interest rates are at levels that, maintained for a sufficiently long duration, will make a substantial contribution to this goal.”

GBPUSD rallied from yesterday’s low of 1.2502 to 1.2725 after the BoE left rates unchanged at 5.25% in another 6-3 split decision. Traders were disappointed by the comment “Monetary policy will need to be sufficiently restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium term, in line with the Committee’s remit.” No early rate cuts for the UK. Prices retreated to 1.2685.

USDJPY plunged with the falling US interest rate outlook, dropping from a pre-FOMC level of 145.30 to 140.97 in Asia, before inching up to 141.38 in NY. Plunging Treasury yields and the soft US dollar fueled the losses.

AUDUSD rallied inside a 0.6654-0.6728 range with prices getting an added lift after the employment report showed Australia gained 61,500 jobs in November (forecast 11,000). The results could encourage the RBA to raise interest rates again if inflation remains elevated.

Today’s US data showed weekly jobless claims falling by 19,000 to 202,000 while retail sales rose by 0.3% m/m (previous -0.2%).

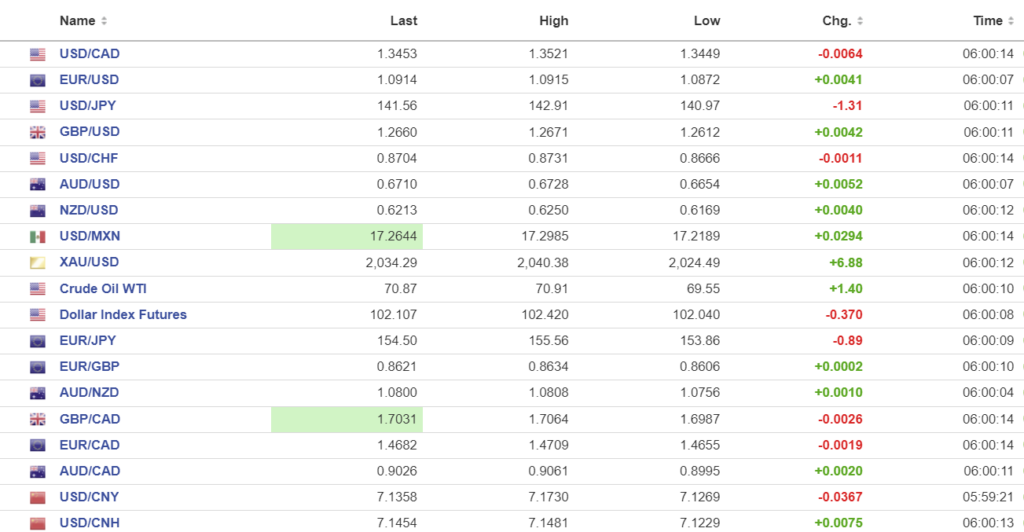

FX high, low, open (as of 6:28 am ET)

Source: Investing.com

China Snapshot

PBoC fix: today 7.1090, expected 7.1566, previous 7.1126.

Shanghai Shenzhen CSI 300 fell 0.52% to 3351.96.

China’s ruling party ended its annual economic work conference with what sounded like a rehashed statement that didn’t offer any major stimulus announcements or priorities.

China’s Canadian embassy said China condemns Canada’s support for Philippines. A spokesman said “The South China Sea is the common home of countries in the region and should not become a hunting ground for Canada, the United States and other countries to pursue their geopolitical interests.” He forgot to add, “It is our exclusive hunting ground.”

Chart: USDCNY and USDCNH

Source: Investing.com