Image by DALL-E

November 29, 2023

- Fed officials changing their tune.

- RBNZ delivers hawkish hold.

- US dollar trading defensively.

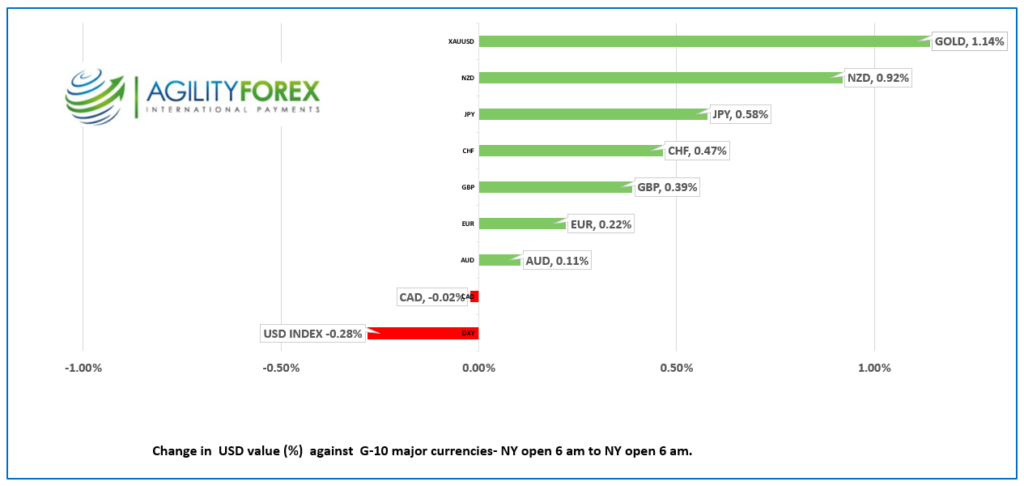

FX at a Glance

Source: I

USDCAD Snapshot: open 1.3583-87, overnight range 1.3541-1.3594, close 1.3575

USDCAD was unable to break below support in the 1.3540 area but continues to trade with a bearish bias thanks to a dovish Fed monetary policy outlook gaining traction. In addition, the steep slide in the US 10-yeear Treasury yield from 4.92% on October 31 to 4.253% overnight has narrowed the spread with 10 year Canadian government bonds, which also undermined USDCAD.

WTI oil prices are directionless inside a $76.37-$77.77/b range. There are rumors that the November 30 Opec meeting may get delayed which suggests the Saudi plan for more production cuts is not being received very warmly. In 2020, an Opec spat led to WTI trading below $0.00 for a brief moment in April.

USDCAD may be seeing month end selling pressures due to the 8.8% MTD gain in the S&P 500.

USDCAD Technicals:

The intraday USDCAD are bearish and in a week-long downtrend channel between 1.3610 on the top and 1.3495 on the bottom. A break above 1.3610 would extend gains to 1.3650 while decisive break below 1.3540 puts 1.3410 in play.

The longer term view turned bearish with the break below 1.3580, which snapped the uptrend line from July 14 and hangs aa target on support at 1.3410. Fibonacci retracement analysis suggests that the break below the 1.3596 level (61.8% retracement of July-November range) puts 1.3505 in play ( the 50% Fibo level).

For today, USDCAD support at 1.3510 and 1.3450. Resistance is at 1.3590-1.3630. Today’s range 1.3510-1.3590

Chart: USDCAD daily

Source: Investing.com

G-10 FX recap

The Federal Reserve’s haberdashery is doing a booming business. Policymakers are swapping “hawkish” black lids for “dovish” white Stetsons. A posse of policymakers have injected a bearish bias into comments and speeches since the November 1 FOMC meeting. The latest was noted hawk Christopher Waller, who said, “I am increasingly confident that policy is currently well positioned to slow the economy and get inflation back to 2%.” He went on to say that if the decline in inflation continues “for several more months, we could start lowering the policy rate.”

It is also month-end and portfolio rebalancing flows are doing their bit to boost FX volatility as the steep equity gains in November imply US dollar selling.

US preliminary Q3 GDP rose 5.2% y/y, easily beating the forecast (5.0%) and adding further support to the “soft-landing” argument. Wholesale Inventories fell 0.2% compared to estimates for a 0.1% increase. FX traders mostly ignored the data.

EURUSD rallied then retreated in a 1.0969-1.1018 range. German CPI fell from 3.8% in October to 3.2% y/y while Eurozone inflation fell to 2.3%. That’s good news for borrowers as it suggests the ECB may soon be cutting interest rates.

GBPUSD bounced in a 1.2674-1.2733 range with prices underpinned by hawkish comments by Bank of England officials suggesting UK rates need to stay high for longer. In addition, month-end portfolio flows are injecting additional volatility into trading. UK travelers flying through Heathrow are hoping that Saudi Arabia’s purchase of 10% of the airport won’t lead to the ban of alcohol and segregation of women and men.

USDJPY is suffering from the Treasury yield blues. The US 10-year Treasury yield closed at 4.336% yesterday then dropped to 4.253% overnight, knocking USDJPY down from its NY close of 147.47 to 146.68 in Asia. Comments from BoJ board member Seiji Adachi, who reiterated a dovish rate outlook, sparked a retracement of all the losses in Europe.

AUDUSD is at its session low after trading in a 0.6619-0.6677 range overnight. Prices were pressured by sales of AUDNZD after Australia’s October inflation rate fell more than forecast (Actual 4.9% y/y vs. forecast 5.2% and September’s 5.5%). Those results reduced the risk that the RBA would hike rates while the RBNZ left the rate-hiking door ajar.

NZDUSD rallied yesterday to close at 0.6138, then climbed further, reaching 0.6209 in the aftermath of the “hawkish-hold” by the RBNZ. The central bank left the overnight cash rate (OCR) unchanged at 5.5% but expressed concern about inflation and warned, “If inflationary pressures were to be stronger than anticipated, the OCR would likely need to increase further.” Prices retreated to 0.6149 with broad US dollar gains against the majors.

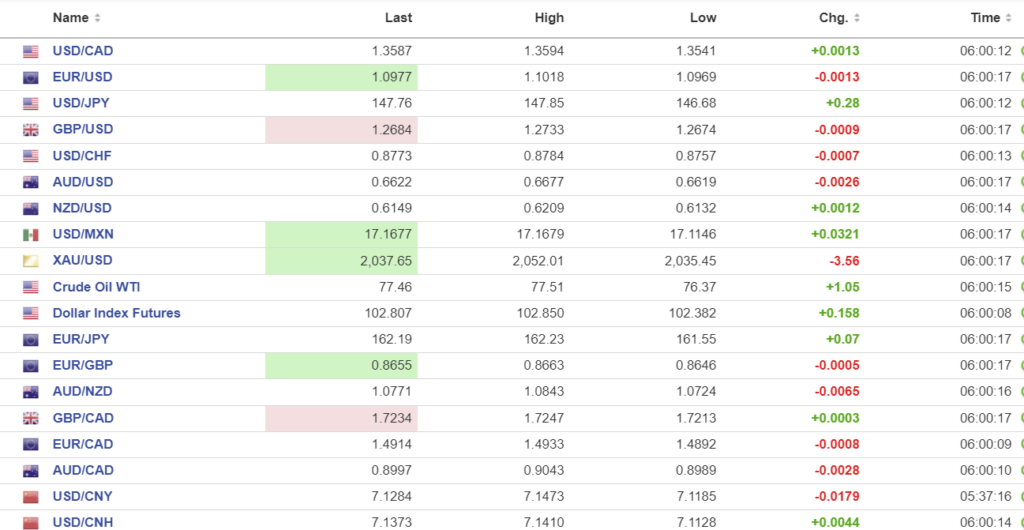

FX high, low, open (as of 6:28 am ET)

Source: Investing.com

China Snapshot

PBoC fix: today 7.1031, expected 7.1340, previous 7.1132.

Shanghai Shenzhen CSI 300 fell 0.86 % to 3488.31.

Chart: USDCNY (onshore) vs USDCNH (offshore)

Source: Investing.com