Photo: BingAI

July 6, 2023

- Markets reacting to prospect of more Fed rate hikes.

- US ADP, soars , Challenger job cuts fall but jobless claims rise.

- USD gains modestly, safe-haven currencies outperform, GBP the outlier.

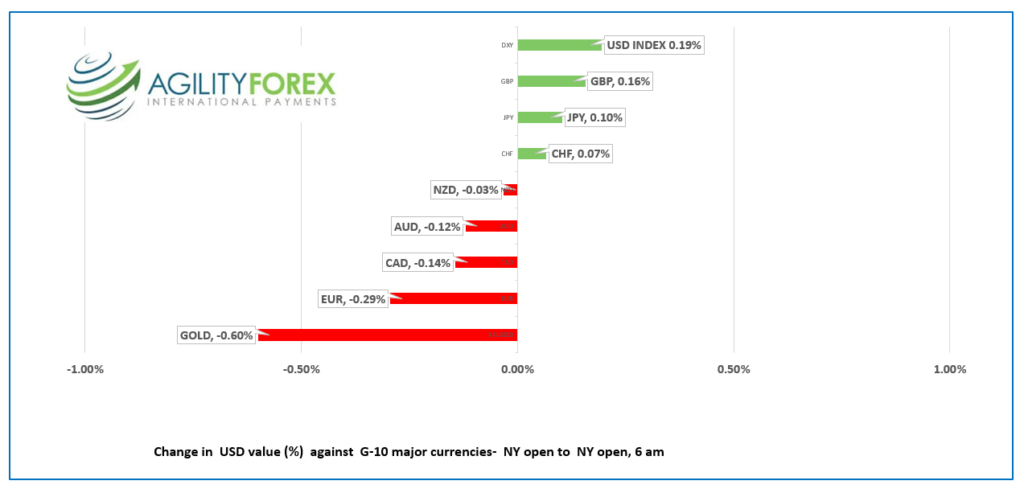

FX at a glance:

Source: IFXA Ltd

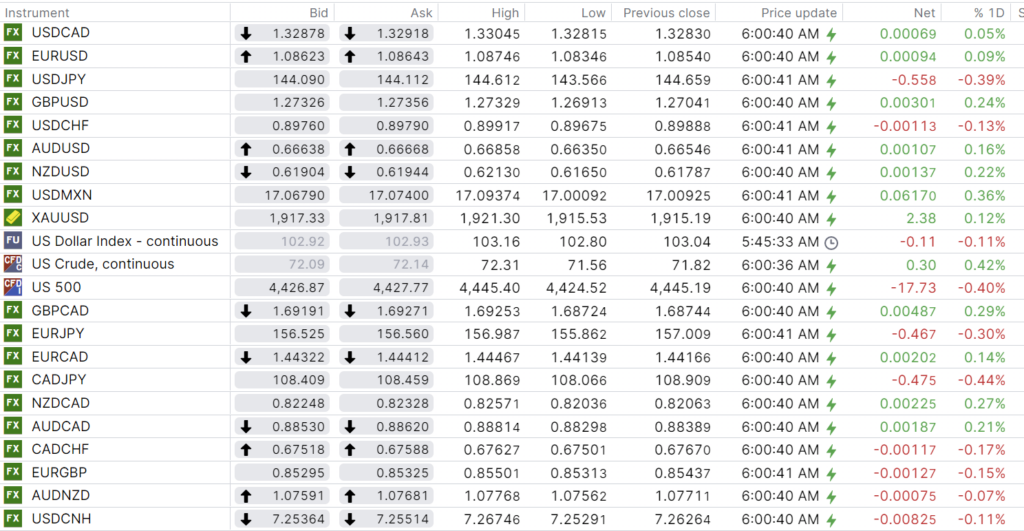

USDCAD Snapshot: open 1.3288-92, overnight range 1.3282-1.3321, close 1.3283

USDCAD is consolidating yesterday’s gains and has a bullish bias rising above 1.3300 in the wake of the surprisingly strong ADP employment report.

The Bank of Canada is clearly out of step with the Fed, hiking when the Fed pauses and now it looks like it will pause while the Fed increases rates on July 22. The odds for a 25 bp hike increased from 86.7% pre-data to 93.6% after todays data.

BoC officials claim they are “data-dependent” which suggests Fridays Canadian employment report could have a material impact on the banks July 12 monetary policy decision. So far, most expect the BoC to leave rates unchanged.

USDCAD gains may be hampered by rising oil prices. WTI rose to $72.31 from $71.58 overnight due to the lingering impact of Saudi and Russian oil production. However, the dampening effect of higher interest rates on global demand is a drag on prices.

Canada’s trade surplus turned to a deficit of $3.44 billion in May due to a 3.8% drop in exports, mainly due to energy.

USDCAD Technical Outlook

The USDCAD technicals are bullish and in a minor uptrend channel between 1.3230 and 1.3380. The break of the June downtrend line that occurred with the move above 1.3190 on June 27 has shifted the focus to 1.3400. However, Fibonacci retracement analysis of the June range suggests that the current rally is merely a correction unless prices break above 1.3320 (38.2% Fibonacci retracement). If that happens 1.3440 is the target. A break below 1.3220 negates the rally.

For today, USDCAD support is at 1.3270 and 1.3230. Resistance is at 1.3330 and 1.3370

Today’s range 1.3280-1.3360

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap

Risk sentiment turned mildly negative following the release of the FOMC minutes. The minutes revealed that policymakers were more united than the market thought and anticipated further rate hikes this year.

The decision to leave rates unchanged on June 14 was not a slam dunk. Those with votes were 100% in agreement, but many, if not most, non-voters wanted to raise rates.

That sentiment was reinforced by NY Fed President John Williams, who said, “…we don’t think we’re done based on what we know.”

Today’s US data almost guarantees a rate hike in July.

ADP employment surged in June, adding 497,000 new jobs compared to the forecast for a gain of 228,000. However, the results should be taken with a grain of salt. ADP Chief Economist Nela Richardson said, “Consumer-facing service industries had a strong June, aligning to push job creation higher than expected. But wage growth continues to ebb in these same industries, and hiring likely is cresting after a late-cycle surge.”

Weekly jobless claims increased by 12,000 to 248,000 compared to 236,000 last week.

Traders will also be paying close attention to the ISM services data (forecast 51 vs 50.3 previously).

Wall Street closed with modest losses, while the major Asian equity indexes suffered far worse. The Nikkei dropped 1.70%, and Australia’s ASX 200 fell 1.24%. Hong Kong’s Hang Seng index was hammered, losing 3.02%, partly because Goldman Sachs downgraded some banks, including Agricultural Bank of China.

European bourses are deeply in the red, led by a 2.22% drop in the French CAC 40 index. S&P 500 futures have lost 0.86%.

Most of the negative equity sentiment was driven by the sharp rise in the US 10-year Treasury yield, which climbed from 3.845% yesterday to 3.984% in NY today.

EURUSD is steady in a 1.0834-1.0889 band after finding the floor in Asia, then climbing steadily into the NY session. The single currency got a lift after German Factory orders rose more than expected (actual 6.4% m/m, April -0.4%). A EURUSD move above 1.0900 puts 1.1020 in play.

GBPUSD has a bid and climbed in a 1.2691-1.2772 band. The rally stalled after today’s US data, but prices are underpinned by expectations for about 125 bps of BoE rate hikes. GBPUSD technicals are bullish above 1.2650.

USDJPY chopped about in a 143.56-144.61 range overnight and then bounced between 143.61 and 144.32 following today’s US data. Renewed safe-haven demand for yen sparked by the risk of higher global interest rates more than offset the rise in the 10-year US Treasury yield.

AUDUSD churned inside a 0.6635-0.6686 band and revisited the session following the ADP data. Australia’s trade surplus widened to AUD 11.791 million from AUD 11.158.

FX open, high, low, previous close as of 6:00 am ET

Source: Bloomberg

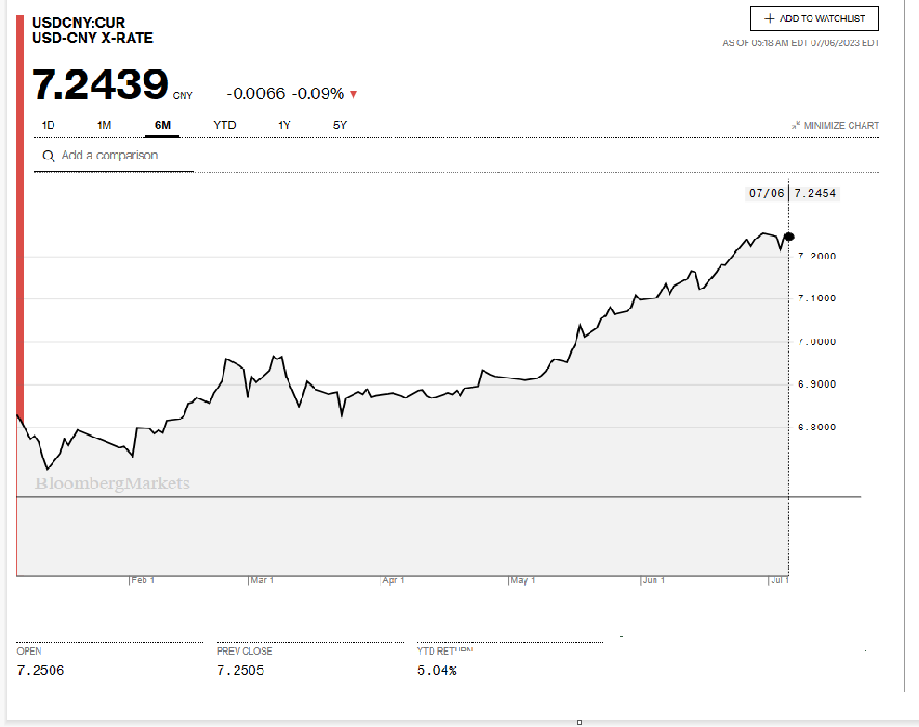

China Snapshot

Bank of China Fix: 7.2098, Previous 7.1968

Shanghai Shenzhen CSI 300 fell 0.77% to 3842.75.

Chart: USDCNY 6 month

Source: Bloomberg