Image generated by Open AI’s DALL-E

November 10, 2023

- UK avoids a recession-Q3 GDP 0% q/q.

- US 10-year Treasury yields rise by 15.5 bps after Powell’s speech.

- US dollar consolidating Thursday’s gains-AUD underperforms.

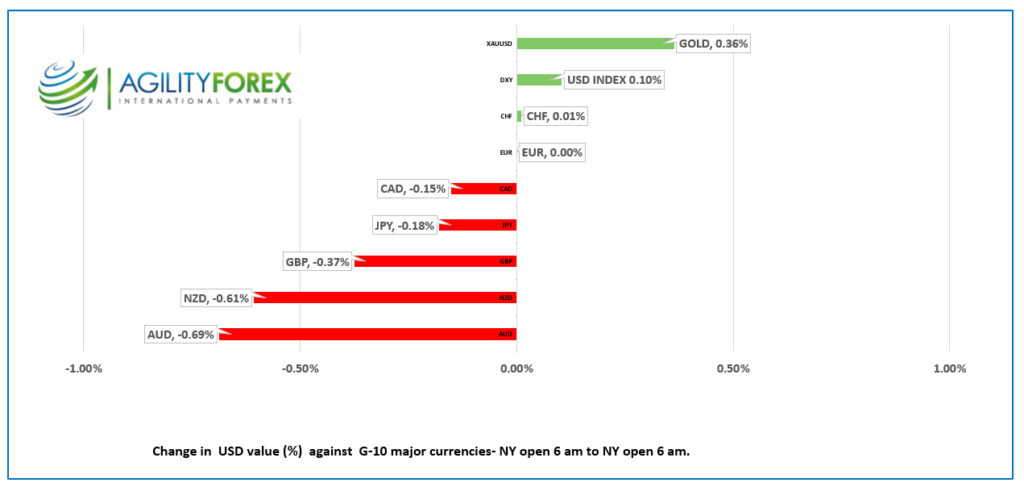

FX at a Glance

Source: IFXA/RP

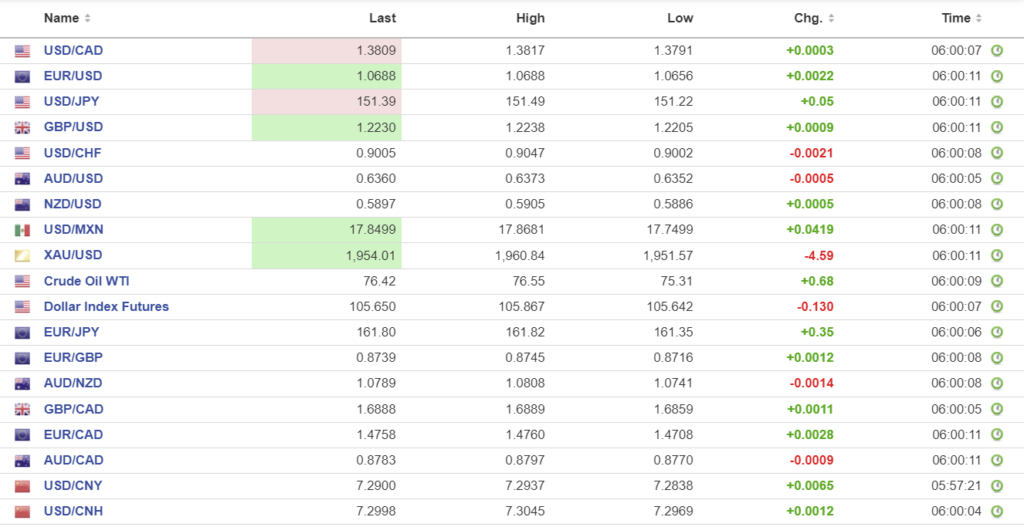

USDCAD Snapshot: open 1.3807-11, overnight range 1.3791-1.3821, close 1.3806

USDCAD is having a good week. It found a bottom at 1.3630 on Monday, and then it climbed steadily throughout the week to 1.3821 today. The rally nearly fully erases the losses that occurred after last Friday’s nonfarm payrolls report was weaker than expected. Back then, the story was US interest rates have peaked, and that the next move is a rate cut. Mr. Powell disabused that notion yesterday.

BoC Deputy Governor Carolyn Rogers delivered a somewhat hawkish outlook for Canadian rates yesterday, in a speech in Vancouver. She basically proclaimed that the era of low rates is over, in case Canadians were unaware of that fact after 475 bps of rate hikes since March 2022.

She went on to say that geopolitical risks, underscored by tensions in regions like Ukraine and Israel/Gaza, threaten to escalate global energy costs and disrupt supply chains, influencing inflation, and nudging rates upwards.

WTI oil prices are helping to support USDCAD. WTI traded in a $75.31-$76.66/barrel range due to fears of slower global growth.

Even so, it is the outlook for US rates that is moving USDCAD, and Fed Chair Powell tried to crush hopes for a new easing cycle occurring any time soon.

USDCAD Technicals:

The intraday technicals are unchanged from Thursday. They are bullish while prices are above 1.3770, looking for a break above 1.3830 to extend gains to 1.3870. A decisive break above 1.3830 risks further gains to 1.4020.

Longer-term, the uptrend that began in June 2021 continues to guide prices higher, and it is intact while USDCAD is above 1.3210 on a monthly chart. A break above 1.4020 would target 1.4170, then 1.4300.

For today, USDCAD support at 1.3770 and 1.3730. Resistance at 1.3830 and 1.3870. Today’s expected trading range is 1.3770-1.3870.

Chart: USDCAD 4 hour

Source: Investing.com

G-10 FX recap

If Mark Twain was a Fed watcher, he may have said “The reports that interest rates have peaked are greatly exaggerated,” after he heard Fed Chair Jerome Powell’s opening remarks at the IMF’s research conference in Washington.

Mr. Powell did a high-wire high-step, balancing hawkish inflation concerns with dovish rate cut preferences, while hinting at potential U.S. rate increases.

He spoke of concerns about a tight labor market risking wage-push inflation, while robust GDP growth in Q3 could help keep inflation at elevated levels. It wasn’t all bad. Mr. Powell said that as the impact from the pandemic wanes, a shift from goods to services and improvements in labor supply could reduce wage pressures.

Nevertheless, he did warn that the FOMC isn’t sure if the current policy is restrictive enough to reduce inflation to 2% and so he is ready to tighten further if necessary.

That was all traders wanted to hear. The US dollar caught a bid, Wall Street retreated, and the US Treasury yields soared.

Asian equity markets closed with losses, led by a 0.74% drop in Australia’s ASX 200. European bourses are lower with the French CAC 40 down 1.10% and the UK FTSE 100 down 1.29%. S&P 500 futures are flat. The US 10-year Treasury yield rallied from 4.475% pre-Powell to 4.63%, by the close and opened at 4.644%.

The sharp jump in US Treasury yields fueled US dollar gains across the board.

EURUSD traded in a 1.0656-1.0689 range and opened where it opened yesterday. ECB President Christine Lagarde speaks and is expected to push back against speculation that rates will be cut as early as April 2024. EURUSD technicals are bearish below 1.0750.

GBPUSD is in the middle of its 1.2205-1.2238 overnight range, as it consolidates its losses after Powell’s speech. The currency got a little support after GDP data showed the economy avoided a technical recession in Q3. (GDP actual 0.0% q/q vs forecast -0.1%, 0.6% y/y vs forecast 0.5%). Even so, the Bank of England doesn’t not expect any growth in 2024 which will limit GBPUSD gains.

USDJPY traded with a bullish bias in a 151.22-151.49 range supported by divergent monetary policy outlooks between the BoJ and the Fed. BoJ Governor Ueda prefers to err on the side of leaving rates too low in a rising inflation environment while the Fed Chair Powell will hike rates if inflation remains sticky. Traders are daring the BoJ to intervene.

AUDUSD consolidated its losses following Powell’s comments and traded in a narrow 0.6352-0.6373 range overnight. Prices were weighed down by broad US dollar demand and concerns that the RBA may be on hold while the Fed may hike rates again.

US weekly jobless claims are expected to be 218,000, compared to 217,000 last week.

The preliminary Michigan Consumer Sentiment Index for November is expected close to unchanged at 63.7 (previously 67.8).

FX high, low, open

Source: Investing.com

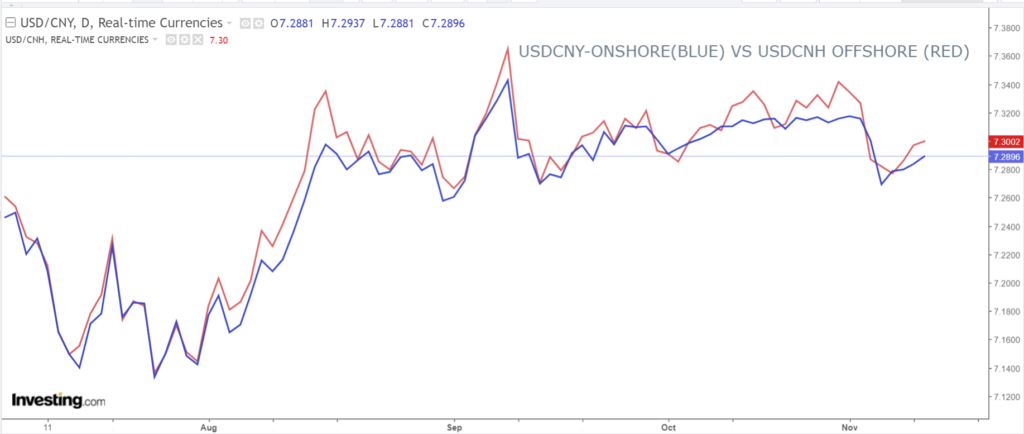

China Snapshot

PBoC fix: today 7.1771, expected 7.2963, previous 7.1772.

Shanghai Shenzhen CSI 300 fell 0.73% to 3586.49.

Chart: USDCNY (onshore) vs USDCNH (offshore) 3 months

Source: Investing.com