Photo: Wikimedia

- Commodity currency bloc slumps with falling commodity prices

- US Retail Sales tops forecasts, rising 1.0% m/m

- US dollar maintains bullish bias; consolidates gains

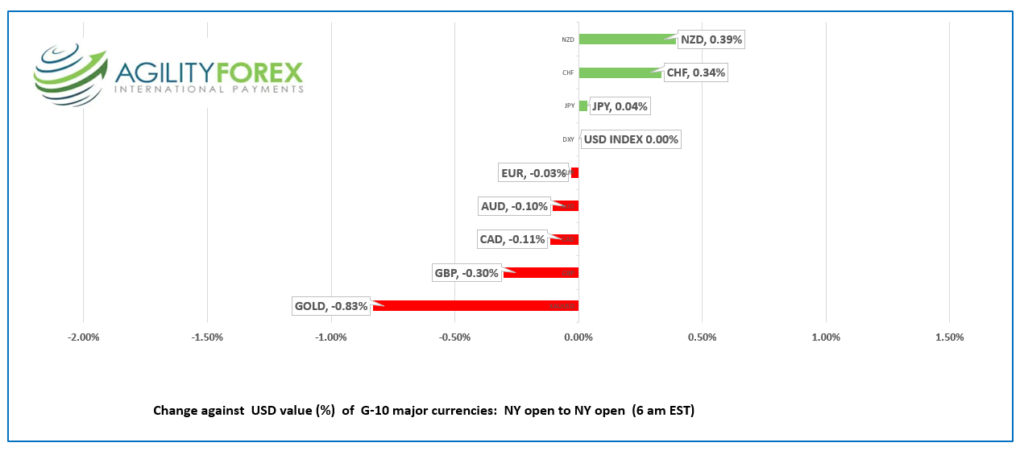

FX at a glance:

Source: IFXA Ltd/RP

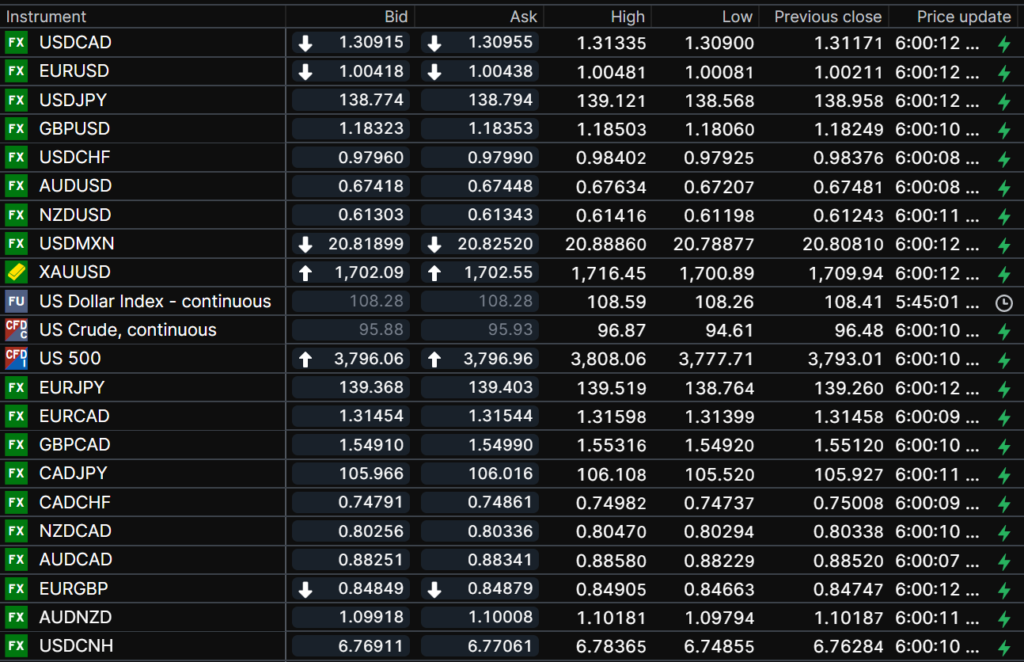

USDCAD Snapshot: open 1.3092-96, overnight range 1.3090-1.3134, close 1.3117

USDCAD had a wild session on Thursday. USDCAD gained 1.95% from its Asia open until the 10:00 am NY option expiry window before retreating and settling into a 1.3087-1.3134 range, which also contained the overnight price action.

It wasn’t alone. AUDUSD and NZDUSD traded in a similar fashion on the back of falling commodity prices. The Thomson Reuters CRB index lost 1.68%.

Recession fears, and concerns about Chinese growth hammered WTI oil prices and snapped the 2021 up trendline, last week. Oil has given back most of its gains following the Russian invasion of Ukraine, but until Russian sanctions are lifted, the downside is limited.

USDCAD retreated from its peak after Fed policymakers pushed back against the notion of a 100 bp rate hike. The CME Fedwatch tool suggests the odds are 50/50 between 0.75 and 100, down from over 60% after the US inflation print and the BoC 1.0% rate hike.

The Canadian economic data is not a factor today.

USDCAD technical outlook

The intraday USDCAD technicals are bullish. The decisive break above 1.3070-80, spike to 1.3224 then retreat to the breakout level suggests a period of consolidation in a 1.3000-1.3220 range, with a break above 1.3220 targeting 1.3400. A move below 1.3070 may extend losses to 1.2970, which is the uptrend line from June.

For today, USDCAD support is at 1.3070 and 1.3020. Resistance is at 1.3140 and 1.3180. Today’s Range 1.3050-1.3150

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

Fed policymakers were a tad annoyed with bond markets telling them rates would rise by 1.00% at the July 27 meeting.

Governor Christopher Waller said, “I support another 75-basis point increase, bringing the target range for the federal funds rate to 2-1/4 to 2-1/2 percent before August.” Then he added, “my base case for July depends on incoming data. We have important data releases on retail sales and housing coming in before the July meeting. If that data comes in materially stronger than expected, it will make me lean towards a larger hike at the July meeting.” So not really a pushback, more of a gentle nudge.

St Louis Fed President is a fan of a 0.75% increase. He said a similar hike in July would be “unprecedented,” which suggests he is not on board with a 100 bp bump.

Those comments were all traders needed to hear. Wall Street clawed back losses but still closed in the red. Asian equity indexes fell due to disappointing Chinese GDP data and weak commodity prices. The Nikkei 225 index was the outlier, rising 0.54%.

US Retail Sales rose 1.0% (forecast 0.8%), ex-autos rose 1.0% (forecast 0.6%). The higher than expected results could make Governor Waller lean toward a “larger hike.”

The post-data, knee-jerk reaction to sell bonds, and equities, and buy US dollar reversed as quickly as it occurred.

European bourses opened in positive territory and added to those gains in a profit-taking rally by the NY open. The German Dax index is the front-runner with a 1.24% gain, a tad s lower than its best level. Meanwhile, S&P 500 and DJIA futures dipped then rallied after the Retail Sales data.

The G20 Finance Ministers meeting from Bali, Indonesia, kicks off today, which may provide some headline risk for markets.

EURUSD smashed through parity yesterday and dropped to 0.9955 before rebounding to 1.0045 and closing at 1.0021. Prices consolidated in a 1.0008-1.0059 range overnight, and extended those gains to 1.0074 in NY.

GBPUSD dropped to 1.1760 yesterday before rallying to 1.1852 overnight. And is trading sideways in a 1.1806-1.1852 band. GBPUSD remains under pressure due to UK recession risks, broad US dollar strength, and the current campaign by Conservative MP’s to select their next ex-leader.

USDJPY consolidated gains in a 138.57-139.12 range. Prices continue to be underpinned by sharply divergent BoJ and Fed monetary policies.

AUDUSD and NZDUSD traded choppily inside recent ranges. Falling commodity prices and weak Chinese data weighed on prices.

Chart of the Day: WTI oil daily

Source: Saxo Bank

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

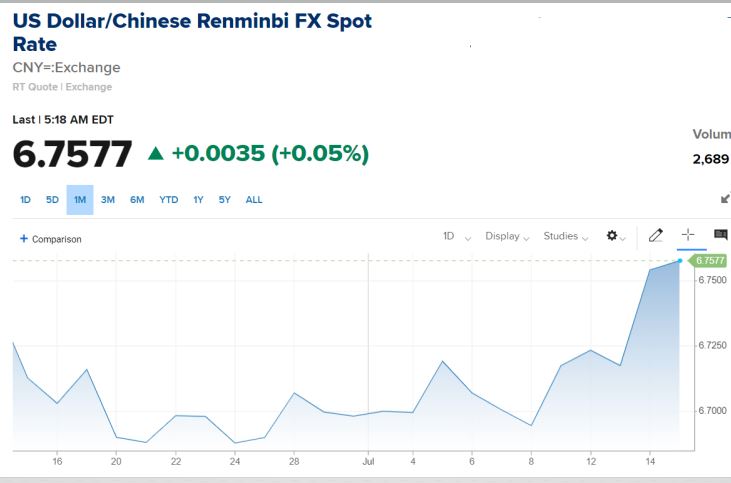

China Snapshot

Today’s Bank of China Fix 6.7503, previous 6.7265

Shanghai Shenzhen CSI 300 fell 1.70% to 4,248.53

Officials forecast retail sales will “maintain an upward trend in H2, per Global Times

June Retail Sales 3.1%y/y (forecast 0, previous -6.7%

Q2 GDP -2.6% q/q (forecast -1.5%, previous 1.4% q/1; Q2 GDP 0.4% y/y (forecast 1.0%, previous 4.8% y/y)

Chart: USDCNY 1 month

Source: CNBC