Photo: HDclipartall.com

February 15, 2023

- Negative risk sentiment rippling through markets.

- US January Retail Sales surge 3.0% m/m (previous -1.1%).

- US dollar rebounds-GBP underperforms.

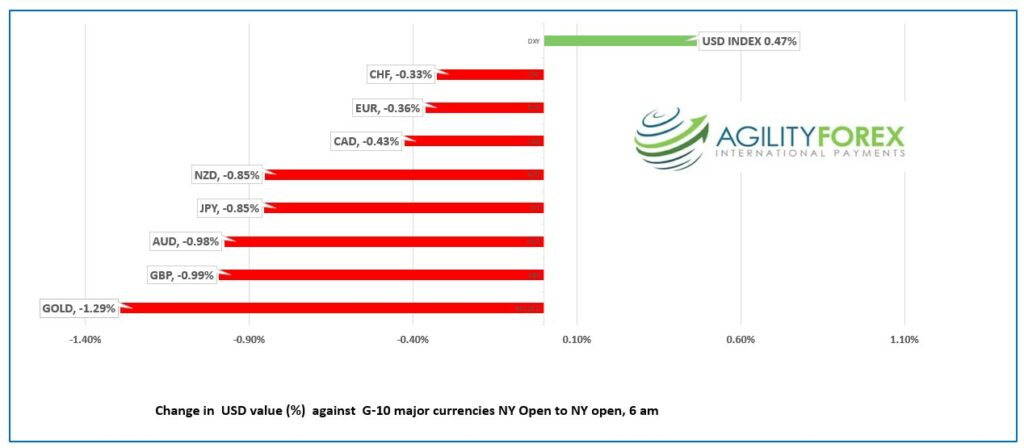

FX at a glance

Source: IFXA Ltd/RP

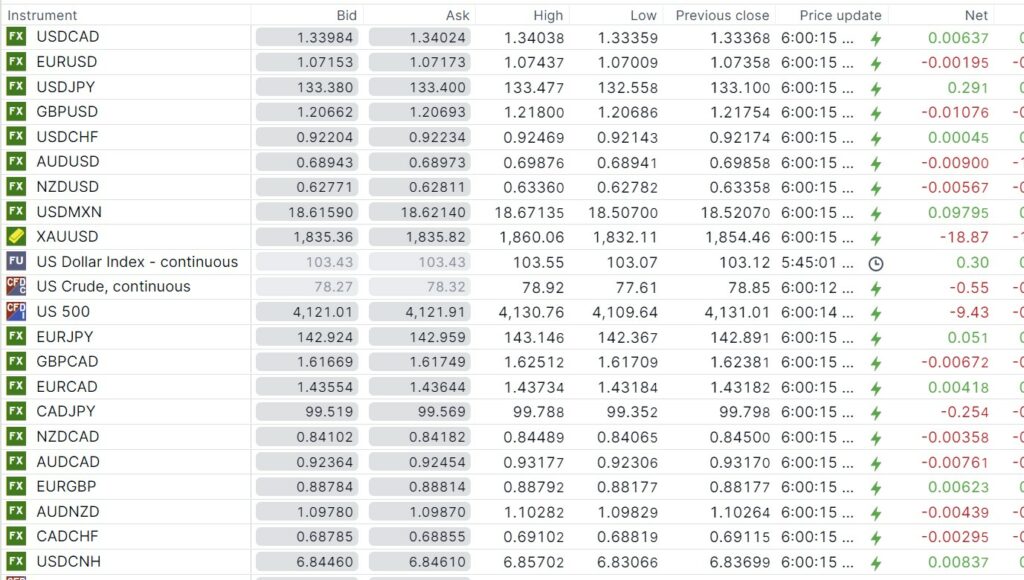

USDCAD Snapshot: open 1.3400-04, overnight range 1.3336-1.3432, close 1.3337

USDCAD had a brief fling with support in the 1.3270-80 area yesterday in the turmoil following the US inflation report. The move was quickly reversed and USDCAD consolidated in a 1.3333-1.3374 for the rest of the day. Prices climbed steadily overnight due to a wave of US dollar demand against the major G-10 currencies.

USDCAD gains extended after US Retail Sales surged 3.0% m/m. The news further reinforces Fed Chair Powell’s view that US rates need to rise higher than expected to tame inflation.

USDCAD garnered additional support from Manufacturing and Wholesale Sales data. Both reports were weak, but an improvement on the November results.

Nevertheless, USDCAD remains rangebound in a 1.3300-1.3500 band.

Oil prices are not providing much support for USDCAD bears. WTI dropped from $79.50/barrel Tuesday to $77.61/b overnight due to both US dollar strength and a sharp build in US crude inventories. API reported that US crude stocks rose 10.5 million barrels in the week ending February 10.

USDCAD Technical Outlook

The intraday USDCAD technicals turned bullish with the move above 1.3340 then 1.3370 yesterday. A mild intraday uptrend is intact above 1.3340 which will act as support today. A move above 1.3420 will extend gains to 1.3470.

The breach of support in the 1.3300-20 is likely a “false break” and suggests that downside support in the 1.3300-20 area is intact.

For today, USDCAD support is at 1.3360 and 1.3320. Resistance is at 1.3460 and 1.3510

Today’s range 1.3360-1.3440

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

Traders are still licking their wounds after yesterday’s US CPI data failed to deliver a convincing argument that inflation had been tamed.

Core CPI rose 0.4% m/m as expected, trimming the annual rate to 5.6% and the results suggest Fed Chair Powell and his colleagues will continue to raise interest rates.

New York Fed President John Williams agrees. He said that the Fed needs to keep raising rates noting “With the strength in the labor market, clearly there are risks that inflation stays higher for longer than expected, or that we might need to raise rates higher” than current forecasts hold.”

Philadelphia Fed President Patrick Harker sounded hawkish when responding to a question about rates saying “It’s going to be above 5% in the Fed funds rate. How much above 5? It’s going to depend a lot on what we’re seeing.”

Bond traders got the message. The 10-year Treasury yield soared from 3.68% to 3.79% before retreating to 3.74% at the close. The US dollar rallied across the board, while equity traders flip-flopped. The S&P 500 index dropped when the CPI data was released and then recouped most of the losses by the end of the day.

Asia equity markets dropped due to the risk of higher US rates for longer. Australia’s ASX 200 index lost 1.06% while the Nikkei gave up 0.37%.

US Retail Sales rose 3.0% m/min December, easily surpassing the forecast of a 1.8% gain. The US dollar rallied, S&P 500 futures fell, and the 10-year Treasury yield climbed to 3.78%, before dipping back to 3.75%.

European bourses opened modestly lower but have since rallied with 0.97% gain in the French CAC 40 index leading indexes higher. The UK FTSE 100 is underperforming and is flat on the day. Oil and gold prices are lower due to the robust greenback.

EURUSD traded in a 1.0701-1.0744 range overnight then dropped to 1.0675 after the US Retail Sales data. The mix of strong US economic reports and soft Euro area data (EU Industrial Production fell 1.1% m/m and 1.7% y/y in December) are weighing on the currency.

GBPUSD fell to 1.2008, post Retail Sales, after trading in a 1.2058-1.2180 range overnight. UK inflation cooled in January (actual 10.1% y/y vs December 10.5% y/y) which raised hopes the Bank of England would not hike rates as high as previously forecast.

USDJPY rallied from 132.56 to 133.48 then accelerated to 134.13 after the US data. The jump in the US 10-year Treasury yield fueled the gains but prices have since retreated along with 10-year yields.

AUDUSD traded in a 0.6876-0.6988 range with the low seen in early NY trading. RBA Governor Philip Lowe reiterated comments that Australia rates need to rise.

Other US data releases include Capacity Utilization, Business Inventories, Industrial Production and NAHB Housing Market Index.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

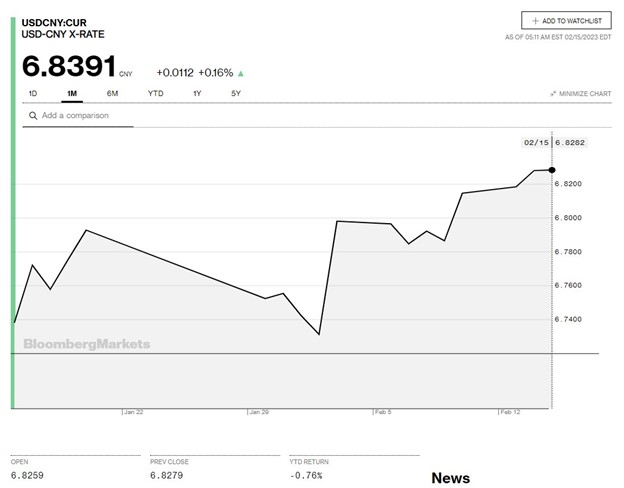

China Snapshot

Bank of China Fix: 6.8196, Previous: 6.8136

Shanghai Shenzhen CSI 300 fell 0.52% to 4123.69.

Chart: USDCNY 1 month

Source: Bloomberg